Advertisement

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

Could CSR Limited (ASX:CSR) be an attractive dividend share to own for the long haul? Investors are often drawn to strong companies with the idea of reinvesting the dividends. If you are hoping to live on your dividends, it's important to be more stringent with your investments than the average punter. Regular readers know we like to apply the same approach to each dividend stock, and we hope you'll find our analysis useful.

A high yield and a long history of paying dividends is an appealing combination for CSR. It would not be a surprise to discover that many investors buy it for the dividends. The company also bought back stock equivalent to around 0.5% of market capitalisation this year. Some simple analysis can reduce the risk of holding CSR for its dividend, and we'll focus on the most important aspects below.

Click the interactive chart for our full dividend analysis

Payout ratios

Companies (usually) pay dividends out of their earnings. If a company is paying more than it earns, the dividend might have to be cut. Comparing dividend payments to a company's net profit after tax is a simple way of reality-checking whether a dividend is sustainable. Looking at the data, we can see that 94% of CSR's profits were paid out as dividends in the last 12 months. This is quite a high payout ratio that suggests the dividend is not well covered by earnings.

In addition to comparing dividends against profits, we should inspect whether the company generated enough cash to pay its dividend. CSR paid out 306% of its free cash flow last year, suggesting the dividend is poorly covered by cash flow. Paying out more than 100% of your free cash flow in dividends is generally not a long-term, sustainable state of affairs, so we think shareholders should watch this metric closely. Cash is slightly more important than profit from a dividend perspective, but given CSR's payouts were not well covered by either earnings or cash flow, we would definitely be concerned about the sustainability of this dividend.

Dividend Volatility

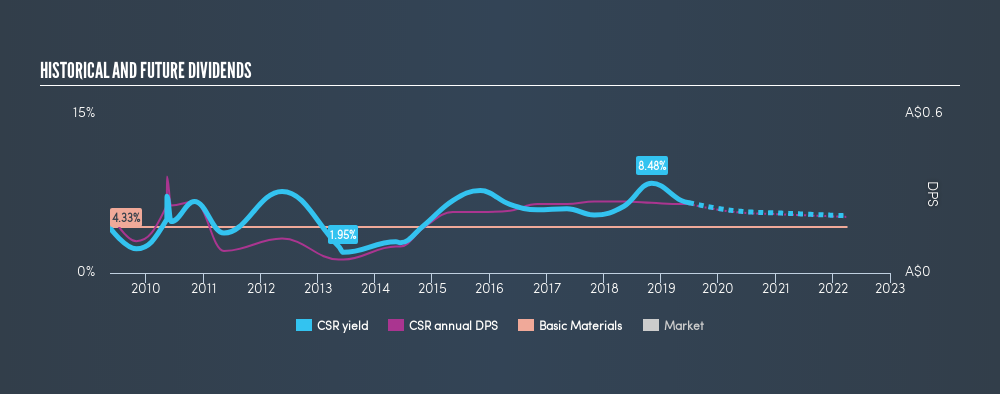

From the perspective of an income investor who wants to earn dividends for many years, there is not much point buying a stock if its dividend is regularly cut or is not reliable. CSR has been paying dividends for a long time, but for the purpose of this analysis, we only examine the past 10 years of payments. The dividend has been cut by more than 20% on at least one occasion historically. During the past ten-year period, the first annual payment was AU$0.23 in 2009, compared to AU$0.26 last year. Dividends per share have grown at approximately 1.5% per year over this time. CSR's dividend payments have fluctuated, so it hasn't grown 1.5% every year, but the CAGR is a useful rule of thumb for approximating the historical growth.

We're glad to see the dividend has risen, but with a limited rate of growth and fluctuations in the payments, we don't think this is an attractive combination.

Dividend Growth Potential

With a relatively unstable dividend, it's even more important to evaluate if earnings per share (EPS) are growing - it's not worth taking the risk on a dividend getting cut, unless you might be rewarded with larger dividends in future. CSR has grown its earnings per share at 9.6% per annum over the past five years. Although per-share earnings are growing at a credible rate, virtually all of the income is being paid out as dividends to shareholders. This is okay, but may limit growth in the company's future dividend payments.

Conclusion

When we look at a dividend stock, we need to form a judgement on whether the dividend will grow, if the company is able to maintain it in a wide range of economic circumstances, and if the dividend payout is sustainable. We're a bit uncomfortable with CSR paying out a high percentage of both its cashflow and earnings. Next, earnings growth has been good, but unfortunately the dividend has been cut at least once in the past. Overall, CSR falls short in several key areas here. Unless the investor has strong grounds for an alternative conclusion, we find it hard to get interested in a dividend stock with these characteristics.

Earnings growth generally bodes well for the future value of company dividend payments. See if the 11 CSR analysts we track are forecasting continued growth with our free report on analyst estimates for the company.

If you are a dividend investor, you might also want to look at our curated list of dividend stocks yielding above 3%.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About ASX:CSR

CSR

Engages in the manufacture and supply of building products for residential and commercial constructions in Australia and New Zealand.

Flawless balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.5% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.9% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|21.3% undervalued

TI

Community Contributor