Advertisement

Undervalued Small Caps With Insider Activity On ASX For January 2025

Simply Wall St

Reviewed by Simply Wall St

The Australian market has recently seen the ASX200 reach a record high, buoyed by positive sentiment as concerns over potential tariffs on China ease, with sectors like IT and Materials leading the charge. In this context of shifting investor confidence and sector performance, identifying promising small-cap stocks involves looking at those with strong fundamentals and recent insider activity, which may signal potential opportunities amidst broader market trends.

Top 10 Undervalued Small Caps With Insider Buying In Australia

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Rural Funds Group | 7.6x | 5.6x | 38.60% | ★★★★★★ |

| Collins Foods | 17.6x | 0.6x | 8.62% | ★★★★★☆ |

| SHAPE Australia | 15.3x | 0.3x | 26.25% | ★★★★☆☆ |

| Dicker Data | 19.4x | 0.7x | -62.07% | ★★★★☆☆ |

| Abacus Group | NA | 5.3x | 29.32% | ★★★★☆☆ |

| Healius | NA | 0.6x | 4.96% | ★★★★☆☆ |

| Abacus Storage King | 11.1x | 6.9x | -21.95% | ★★★☆☆☆ |

| Autosports Group | 5.6x | 0.1x | -47.17% | ★★★☆☆☆ |

| Integral Diagnostics | NA | 2.5x | 49.45% | ★★★☆☆☆ |

| Tabcorp Holdings | NA | 0.7x | -10.85% | ★★★☆☆☆ |

Below we spotlight a couple of our favorites from our exclusive screener.

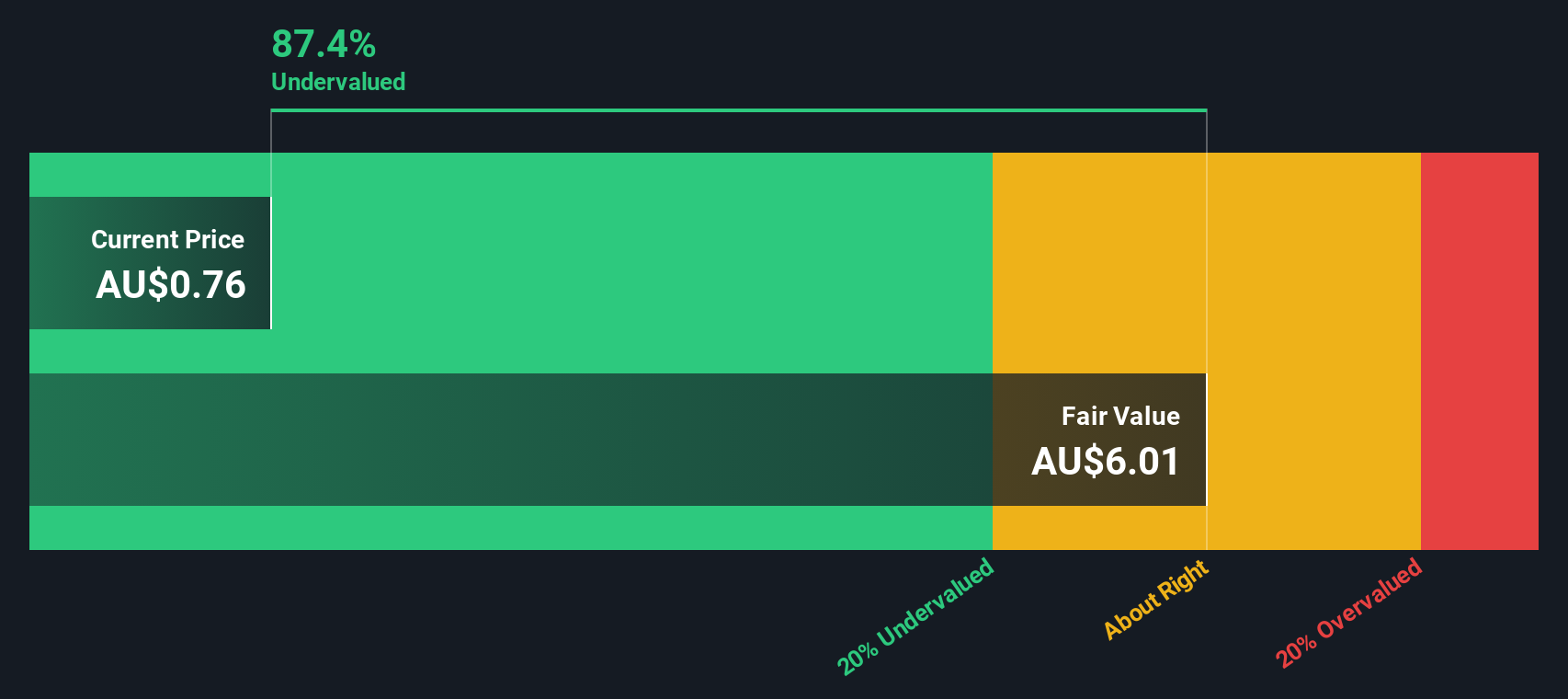

Healius (ASX:HLS)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Healius operates in the healthcare sector, providing pathology and imaging services, with a market capitalization of A$2.34 billion.

Operations: Healius generates revenue primarily from its Pathology and Imaging segments, with Pathology contributing significantly more than Imaging. The company's cost of goods sold (COGS) has been substantial, affecting its gross profit margin, which has shown a declining trend from 46.25% in early 2014 to around 31.00% by mid-2025. Operating expenses have remained a notable part of the financial structure, impacting overall profitability as seen in varying net income margins over the periods analyzed.

PE: -1.6x

Healius, a company known for its healthcare services in Australia, recently appointed Kathy Ostin as an independent Non-Executive Director, enhancing their board's expertise in finance and governance. The company's earnings are forecasted to grow by 96% annually, indicating potential value growth. Despite relying solely on external borrowing for funding—considered higher risk—their strategic leadership changes and shareholder-approved constitutional amendments may position them well for future growth.

- Take a closer look at Healius' potential here in our valuation report.

Understand Healius' track record by examining our Past report.

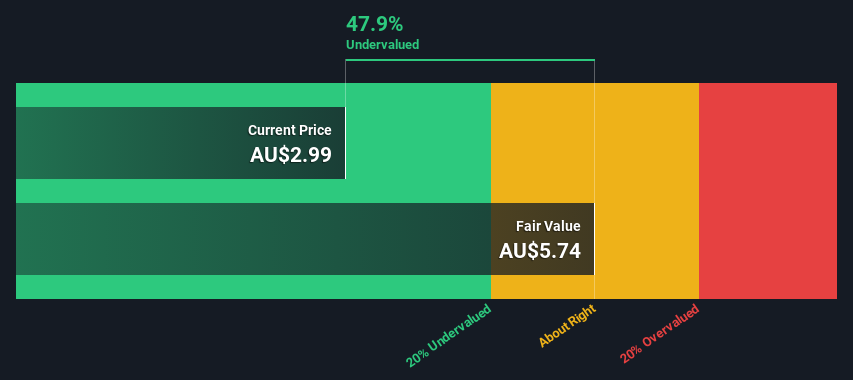

Integral Diagnostics (ASX:IDX)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Integral Diagnostics operates diagnostic imaging facilities, providing medical imaging services with a market cap of A$1.19 billion.

Operations: Integral Diagnostics generates its revenue primarily from operating diagnostic imaging facilities, with a recent revenue figure of A$469.70 million. The company's gross profit margin was 32.34%, while net income has shown a negative trend, with the latest net income margin at -12.92%. Operating expenses and non-operating expenses have been significant cost factors impacting overall profitability.

PE: -19.1x

Integral Diagnostics, with its focus on diagnostic imaging services in Australia, presents an intriguing opportunity within the smaller capitalization space. Despite facing challenges like higher risk funding due to reliance on external borrowing and recent shareholder dilution, the company shows potential for growth with earnings projected to rise by 54% annually. Insider confidence is evident as executives have increased their shareholdings recently. The addition of experienced directors like Laura McBain and Dr Kevin Shaw further strengthens its leadership team.

- Click to explore a detailed breakdown of our findings in Integral Diagnostics' valuation report.

Evaluate Integral Diagnostics' historical performance by accessing our past performance report.

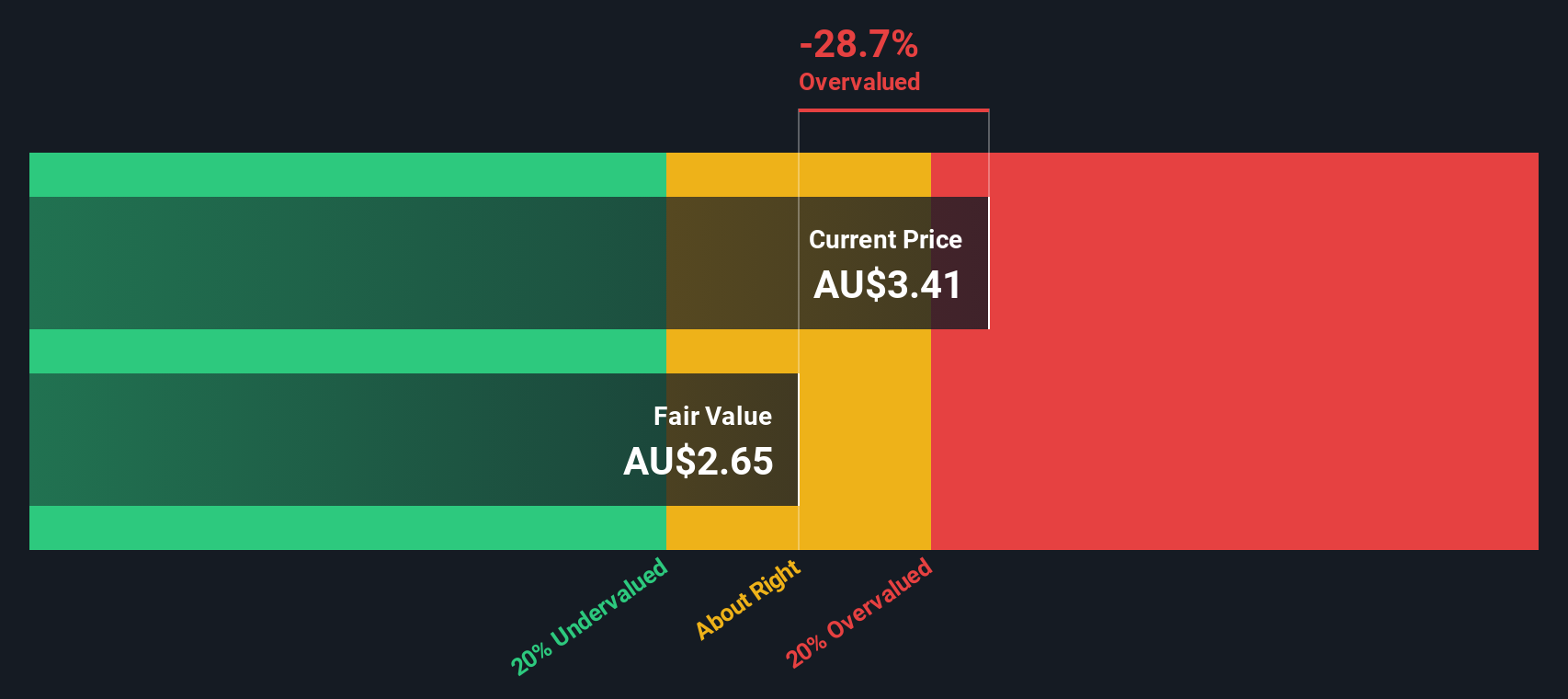

K&S (ASX:KSC)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: K&S is a logistics and transportation company operating primarily in Australia and New Zealand, with a market cap of A$ 0.35 billion, focusing on fuel distribution and transport services across these regions.

Operations: K&S generates revenue primarily from Australian Transport and Fuel, with a smaller contribution from New Zealand Transport. The company's gross profit margin has shown fluctuations, peaking at 44.83% before declining to 12.57%, and then rising again to 15.64%. Operating expenses are a significant cost component, including depreciation and amortization expenses that have varied over time but remain substantial in the overall expense structure.

PE: 16.0x

K&S, an Australian company known for its transport and logistics services, is catching attention in the market due to its perceived undervaluation. Despite having 100% of its liabilities from external borrowing, which presents higher risk compared to customer deposits, insider confidence has been evident with recent share purchases throughout 2024. This insider activity suggests a belief in potential growth or resilience within the industry. As K&S navigates these financial dynamics, investors may find opportunities amidst the challenges.

- Click here and access our complete valuation analysis report to understand the dynamics of K&S.

Examine K&S' past performance report to understand how it has performed in the past.

Seize The Opportunity

- Click here to access our complete index of 21 Undervalued ASX Small Caps With Insider Buying.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if K&S might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:KSC

K&S

Engages in the transportation and logistics, warehousing, and fuel distribution businesses in Australia and New Zealand.

Excellent balance sheet second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

138 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

931 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative