With A 36% Price Drop For Top Shelf International Holdings Ltd (ASX:TSI) You'll Still Get What You Pay For

To the annoyance of some shareholders, Top Shelf International Holdings Ltd (ASX:TSI) shares are down a considerable 36% in the last month, which continues a horrid run for the company. For any long-term shareholders, the last month ends a year to forget by locking in a 64% share price decline.

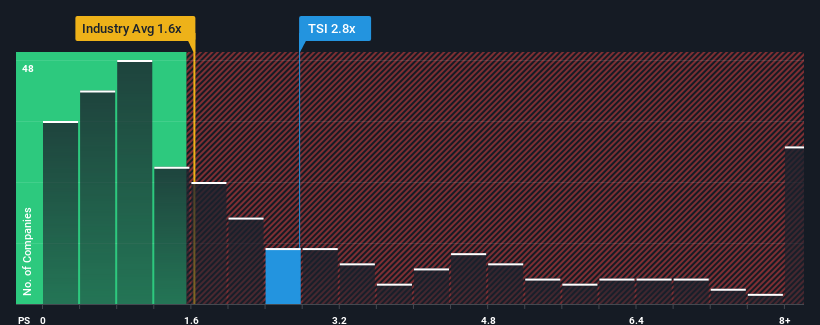

Even after such a large drop in price, given close to half the companies operating in Australia's Beverage industry have price-to-sales ratios (or "P/S") below 1.7x, you may still consider Top Shelf International Holdings as a stock to potentially avoid with its 2.8x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/S.

See our latest analysis for Top Shelf International Holdings

What Does Top Shelf International Holdings' Recent Performance Look Like?

Top Shelf International Holdings certainly has been doing a good job lately as its revenue growth has been positive while most other companies have been seeing their revenue go backwards. It seems that many are expecting the company to continue defying the broader industry adversity, which has increased investors’ willingness to pay up for the stock. However, if this isn't the case, investors might get caught out paying to much for the stock.

Want the full picture on analyst estimates for the company? Then our free report on Top Shelf International Holdings will help you uncover what's on the horizon.How Is Top Shelf International Holdings' Revenue Growth Trending?

There's an inherent assumption that a company should outperform the industry for P/S ratios like Top Shelf International Holdings' to be considered reasonable.

Retrospectively, the last year delivered an exceptional 22% gain to the company's top line. The strong recent performance means it was also able to grow revenue by 227% in total over the last three years. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Turning to the outlook, the next three years should generate growth of 89% per year as estimated by the four analysts watching the company. With the industry only predicted to deliver 9.2% each year, the company is positioned for a stronger revenue result.

With this in mind, it's not hard to understand why Top Shelf International Holdings' P/S is high relative to its industry peers. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

What We Can Learn From Top Shelf International Holdings' P/S?

There's still some elevation in Top Shelf International Holdings' P/S, even if the same can't be said for its share price recently. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

As we suspected, our examination of Top Shelf International Holdings' analyst forecasts revealed that its superior revenue outlook is contributing to its high P/S. It appears that shareholders are confident in the company's future revenues, which is propping up the P/S. It's hard to see the share price falling strongly in the near future under these circumstances.

Having said that, be aware Top Shelf International Holdings is showing 5 warning signs in our investment analysis, and 1 of those is significant.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if Top Shelf International Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:TSI

Top Shelf International Holdings

Engages in the production, marketing, and selling of NED Australian Whisky and Grainshaker Hand Made Vodka spirit products in Australia.

Moderate and slightly overvalued.

Market Insights

Community Narratives