Advertisement

We Think Live Verdure (ASX:LV1) Needs To Drive Business Growth Carefully

There's no doubt that money can be made by owning shares of unprofitable businesses. Indeed, Live Verdure (ASX:LV1) stock is up 484% in the last year, providing strong gains for shareholders. Nonetheless, only a fool would ignore the risk that a loss making company burns through its cash too quickly.

So notwithstanding the buoyant share price, we think it's well worth asking whether Live Verdure's cash burn is too risky. For the purpose of this article, we'll define cash burn as the amount of cash the company is spending each year to fund its growth (also called its negative free cash flow). The first step is to compare its cash burn with its cash reserves, to give us its 'cash runway'.

Check out our latest analysis for Live Verdure

How Long Is Live Verdure's Cash Runway?

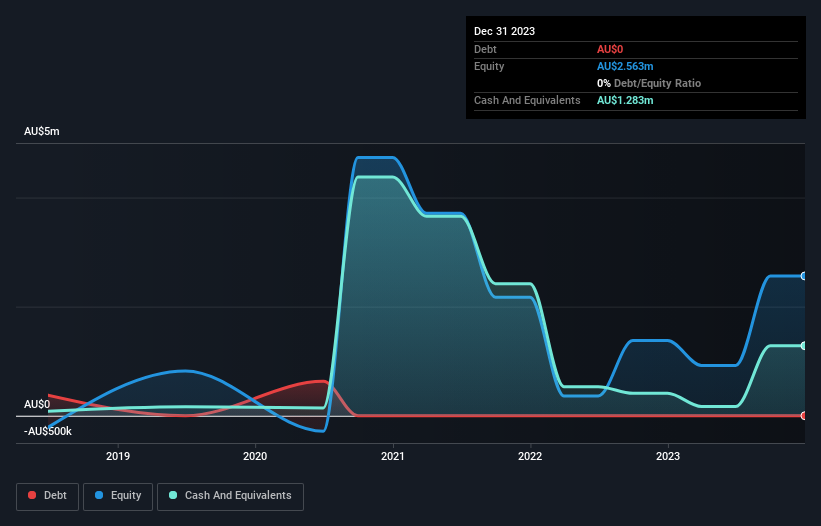

A company's cash runway is calculated by dividing its cash hoard by its cash burn. As at December 2023, Live Verdure had cash of AU$1.3m and no debt. In the last year, its cash burn was AU$2.5m. Therefore, from December 2023 it had roughly 6 months of cash runway. To be frank, this kind of short runway puts us on edge, as it indicates the company must reduce its cash burn significantly, or else raise cash imminently. The image below shows how its cash balance has been changing over the last few years.

How Well Is Live Verdure Growing?

We reckon the fact that Live Verdure managed to shrink its cash burn by 29% over the last year is rather encouraging. Unfortunately, however, operating revenue declined by 2.4% during the period. On balance, we'd say the company is improving over time. In reality, this article only makes a short study of the company's growth data. You can take a look at how Live Verdure has developed its business over time by checking this visualization of its revenue and earnings history.

Can Live Verdure Raise More Cash Easily?

Given Live Verdure's revenue is receding, there's a considerable chance it will eventually need to raise more money to spend on driving growth. Companies can raise capital through either debt or equity. Commonly, a business will sell new shares in itself to raise cash and drive growth. By looking at a company's cash burn relative to its market capitalisation, we gain insight on how much shareholders would be diluted if the company needed to raise enough cash to cover another year's cash burn.

Since it has a market capitalisation of AU$65m, Live Verdure's AU$2.5m in cash burn equates to about 3.8% of its market value. That's a low proportion, so we figure the company would be able to raise more cash to fund growth, with a little dilution, or even to simply borrow some money.

How Risky Is Live Verdure's Cash Burn Situation?

On this analysis of Live Verdure's cash burn, we think its cash burn relative to its market cap was reassuring, while its cash runway has us a bit worried. We don't think its cash burn is particularly problematic, but after considering the range of factors in this article, we do think shareholders should be monitoring how it changes over time. Separately, we looked at different risks affecting the company and spotted 6 warning signs for Live Verdure (of which 2 are concerning!) you should know about.

Of course Live Verdure may not be the best stock to buy. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:DAI

Adequate balance sheet slight.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|36.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|22.0% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|46.4% overvalued

DA

Community Contributor