- Australia

- /

- Oil and Gas

- /

- ASX:WDS

Woodside Petroleum Ltd (ASX:WPL) Just Released Its Annual Earnings: Here's What Analysts Think

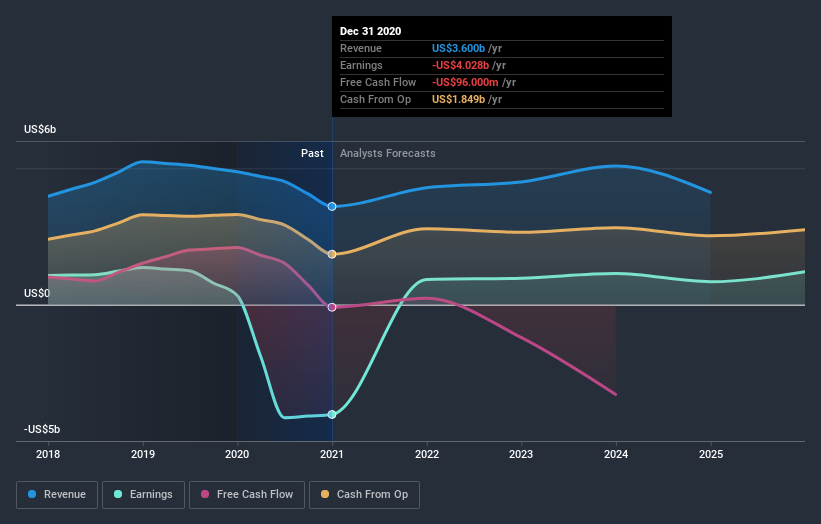

Last week, you might have seen that Woodside Petroleum Ltd (ASX:WPL) released its full-year result to the market. The early response was not positive, with shares down 3.9% to AU$24.00 in the past week. It was a respectable set of results; while revenues of US$3.6b were in line with analyst predictions, statutory losses were 16% smaller than expected, with Woodside Petroleum losing US$4.22 per share. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. We've gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

View our latest analysis for Woodside Petroleum

After the latest results, the twelve analysts covering Woodside Petroleum are now predicting revenues of US$4.28b in 2021. If met, this would reflect a meaningful 19% improvement in sales compared to the last 12 months. Woodside Petroleum is also expected to turn profitable, with statutory earnings of US$0.93 per share. In the lead-up to this report, the analysts had been modelling revenues of US$4.19b and earnings per share (EPS) of US$0.81 in 2021. There's been a pretty noticeable increase in sentiment, with the analysts upgrading revenues and making a nice increase in earnings per share in particular.

Despite these upgrades,the analysts have not made any major changes to their price target of AU$27.84, suggesting that the higher estimates are not likely to have a long term impact on what the stock is worth. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. Currently, the most bullish analyst values Woodside Petroleum at AU$40.00 per share, while the most bearish prices it at AU$21.30. Note the wide gap in analyst price targets? This implies to us that there is a fairly broad range of possible scenarios for the underlying business.

Of course, another way to look at these forecasts is to place them into context against the industry itself. It's clear from the latest estimates that Woodside Petroleum's rate of growth is expected to accelerate meaningfully, with the forecast 19% revenue growth noticeably faster than its historical growth of 0.5%p.a. over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 7.4% next year. Factoring in the forecast acceleration in revenue, it's pretty clear that Woodside Petroleum is expected to grow much faster than its industry.

The Bottom Line

The most important thing here is that the analysts upgraded their earnings per share estimates, suggesting that there has been a clear increase in optimism towards Woodside Petroleum following these results. Happily, they also upgraded their revenue estimates, and are forecasting revenues to grow faster than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

With that in mind, we wouldn't be too quick to come to a conclusion on Woodside Petroleum. Long-term earnings power is much more important than next year's profits. We have estimates - from multiple Woodside Petroleum analysts - going out to 2024, and you can see them free on our platform here.

We don't want to rain on the parade too much, but we did also find 2 warning signs for Woodside Petroleum (1 doesn't sit too well with us!) that you need to be mindful of.

When trading Woodside Petroleum or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Woodside Energy Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:WDS

Woodside Energy Group

Engages in the exploration, evaluation, development, production, marketing, and sale of hydrocarbons in the Asia Pacific, Africa, the Americas, and the Europe.

Undervalued with solid track record.

Similar Companies

Market Insights

Community Narratives