Whitehaven Coal (ASX:WHC) is making headlines with its strategic positioning in the $3 billion Kestrel coal mine process, following its reaffirmed production guidance for fiscal year 2025. The company has reported a significant increase in quarterly production, reflecting its growth trajectory, despite challenges like low return on equity and operational delays. In the discussion that follows, we explore Whitehaven's market strategies, competitive pressures, and future prospects, including its expansion into Southeast Asia and investment in AI for operational efficiency.

ASX:WHC Earnings and Revenue Growth as at Nov 2024

Advertisement

Key Assets Propelling Whitehaven Coal Forward

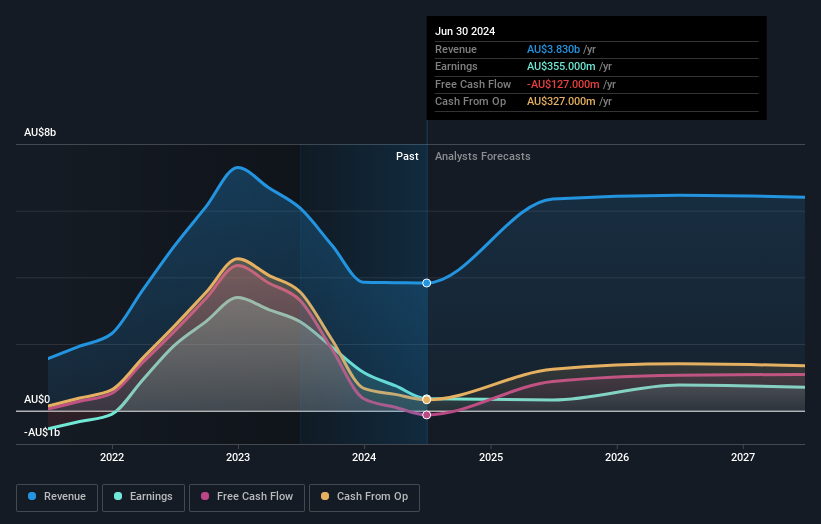

Whitehaven Coal is experiencing growth, with revenue expected to rise by 12.9% annually, outpacing the Australian market average. The company's earnings are projected to grow at 17.9% per year, highlighting its strong market position. CEO Paul Flynn noted that FY '24 has been a standout year for pricing power and demand, reinforcing the company's favorable market conditions. Additionally, WHC's strategic cost management has led to a 15% reduction in operational costs, showcasing operational efficiency. Analysts also predict a significant stock price increase, with targets over 20% higher than the current share price, reflecting investor confidence.

WHC faces challenges, including a low Return on Equity of 6.7%, well below the desired 20%. The company has also grappled with a 7.3% decline in earnings growth over the past year, coupled with a drop in net profit margins from 43.9% to 9.3%. CFO Kevin Ball acknowledged operational delays due to equipment failures, which could impact revenue generation. Furthermore, WHC's valuation, with a Price-To-Earnings Ratio of 15.8x, is favorable compared to peers but remains expensive relative to the industry average.

Future Prospects for Whitehaven Coal in the Market

Opportunities abound for WHC as it explores expansion into Southeast Asia, where coal demand is projected to grow. This move aligns with its strategic focus on capturing emerging markets. The company's investment in AI for predictive maintenance is expected to enhance operational efficiency and reduce costs. Additionally, WHC's involvement in the $3 billion Kestrel coal mine process positions it to capitalize on strategic alliances and expand its asset base.

Competitive Pressures and Market Risks Facing Whitehaven Coal

Economic headwinds remain a concern, with global uncertainty potentially impacting coal demand. Regulatory changes pose another threat, as new policies could impose additional costs. Supply chain disruptions have prompted WHC to reassess its logistics strategies, underscoring the need for adaptability in an evolving market. Competitive pressures from both local and international players also challenge WHC's market share and pricing strategies.

Whitehaven Coal's projected revenue and earnings growth, driven by strategic cost management and favorable market conditions, underscores its strong market position and investor confidence, as reflected in the anticipated stock price increase. However, challenges such as a low Return on Equity and declining profit margins highlight operational inefficiencies and potential revenue impacts from equipment failures. The company's expansion into Southeast Asia and investment in AI for predictive maintenance signal a strategic focus on emerging markets and operational efficiency, which could mitigate some competitive pressures. Despite trading below its estimated fair value with a Price-To-Earnings Ratio of 15.8x, the stock remains expensive relative to the industry average, suggesting that while there is growth potential, investors should weigh these factors against market risks and regulatory challenges.

Summing It All Up

Are you invested in Whitehaven Coal already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Valuation is complex, but we're here to simplify it.

Discover if Whitehaven Coal might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Simply Wall St analyst Simply Wall St and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

About ASX:WHC

Whitehaven Coal

Develops and operates coal mines in New South Wales and Queensland.