Advertisement

- Australia

- /

- Oil and Gas

- /

- ASX:PEN

Analysts' Revenue Estimates For Peninsula Energy Limited (ASX:PEN) Are Surging Higher

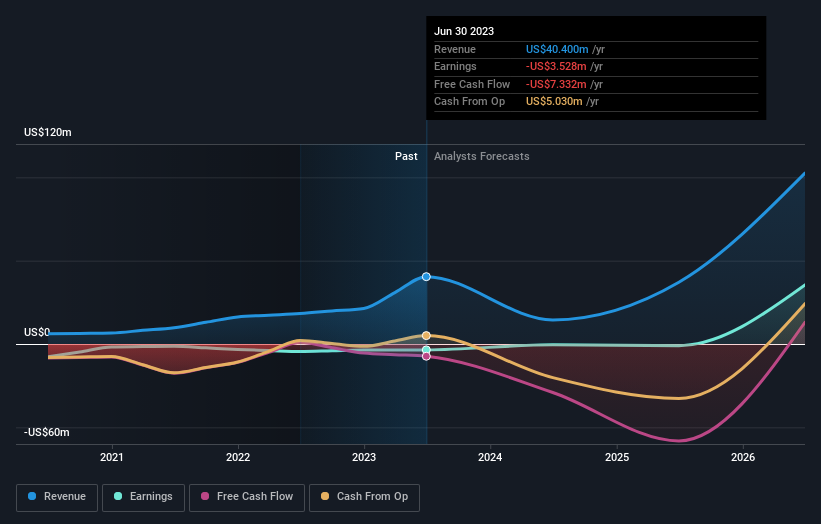

Peninsula Energy Limited (ASX:PEN) shareholders will have a reason to smile today, with the analysts making substantial upgrades to this year's forecasts. The revenue forecast for this year has experienced a facelift, with analysts now much more optimistic on its sales pipeline. Investors have been pretty optimistic on Peninsula Energy too, with the stock up 12% to AU$0.10 over the past week. We'll be curious to see if these new estimates convince the market to lift the stock price higher still.

Following the latest upgrade, the current consensus, from the three analysts covering Peninsula Energy, is for revenues of US$14m in 2024, which would reflect a sizeable 64% reduction in Peninsula Energy's sales over the past 12 months. However, before this estimates update, the consensus had been expecting revenues of US$13m and US$0.0013 per share in losses. So we can see there's been a pretty clear increase in analyst sentiment in recent times, with both revenues and earnings per share receiving a decent lift in the latest estimates.

Check out our latest analysis for Peninsula Energy

There was no particular change to the consensus price target of AU$0.26, with Peninsula Energy's latest outlook seemingly not enough to result in a change of valuation.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. These estimates imply that sales are expected to slow, with a forecast annualised revenue decline of 64% by the end of 2024. This indicates a significant reduction from annual growth of 32% over the last five years. Yet aggregate analyst estimates for other companies in the industry suggest that industry revenues are forecast to decline 2.5% per year. The forecasts do look bearish for Peninsula Energy, since they're expecting it to shrink faster than the industry.

The Bottom Line

The most important thing to take away from this upgrade is that the consensus now expects Peninsula Energy to become profitable this year. They also upgraded their revenue estimates, with sales apparently performing well even though revenue growth expected to decline against the wider market this year. Seeing the dramatic upgrade to this year's forecasts, it might be time to take another look at Peninsula Energy.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have estimates - from multiple Peninsula Energy analysts - going out to 2026, and you can see them free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:PEN

Peninsula Energy

Operates as a uranium exploration company in the United States.

Exceptional growth potential and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor