Advertisement

- Australia

- /

- Diversified Financial

- /

- ASX:SOL

Can WHSP Holdings’ Revenue-Profit Gap Reveal New Strategic Priorities for ASX:SOL Investors?

Simply Wall St

Reviewed by Sasha Jovanovic

- Washington H. Soul Pattinson and Company Limited recently reported its full year results for the period ending July 31, 2025, with A$615.4 million in sales, up from A$557.6 million the previous year, but net income dropping to A$364.2 million from A$498.8 million.

- While sales increased, the reduction in net income and earnings per share highlights pressures on profitability despite growth in revenue.

- We'll explore how higher sales but lower net income in the latest results could shape the outlook for WHSP Holdings going forward.

We've found 18 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

WHSP Holdings Investment Narrative Recap

To be a shareholder in Washington H. Soul Pattinson and Company Limited (WHSP), you need to believe in the group's disciplined allocation to private assets and its ability to deliver long-term value through diversified investments, even in the face of market fluctuations. The recent full year results, in which sales grew but net income declined, do not materially change the near-term catalyst for the business: the ongoing performance of its private asset portfolio. However, the most pressing risk remains exposure to volatile sectors like uranium, which could continue to affect earnings if market conditions weaken further.

Among the latest company developments, WHSP’s recent dividend increase (to A$0.59 per share for the second half of 2025) stands out. This announcement is especially relevant given the dip in net income, as it underscores both continued shareholder payouts and the management’s willingness to maintain distributions despite tighter profit margins, a potential signal of confidence in future cash flows and asset performance.

In contrast, investors should also keep a close eye on how WHSP’s uranium exposure might impact future results if commodity prices remain under pressure...

Read the full narrative on WHSP Holdings (it's free!)

WHSP Holdings' narrative projects A$1.3 billion revenue and A$398.8 million earnings by 2028. This requires a 0.8% annual revenue decline and a decrease of A$124.4 million in earnings from A$523.2 million today.

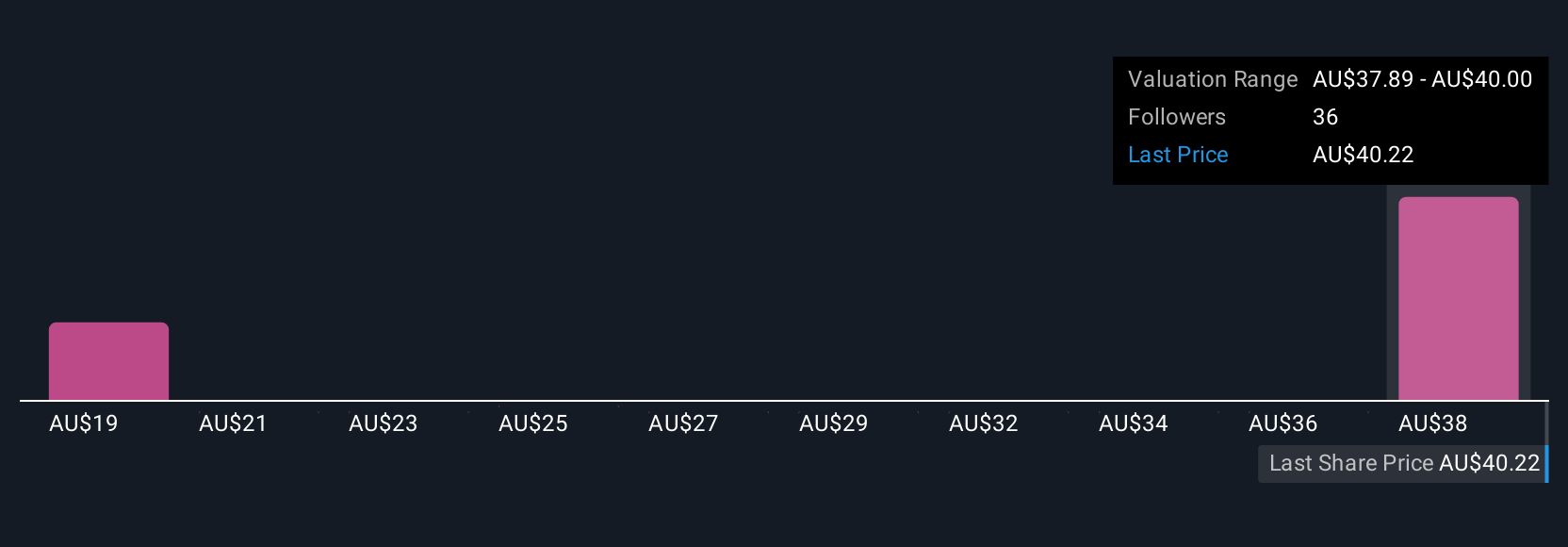

Uncover how WHSP Holdings' forecasts yield a A$39.08 fair value, in line with its current price.

Exploring Other Perspectives

Four Simply Wall St Community fair value estimates for WHSP span from A$17.27 to A$40.00 per share, reflecting wide disparities in outlooks. This diversity sits alongside ongoing questions about whether reliance on private assets and sector exposure will boost, or constrain, future profitability, reminding you to examine several viewpoints before deciding where you stand.

Explore 4 other fair value estimates on WHSP Holdings - why the stock might be worth less than half the current price!

Build Your Own WHSP Holdings Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your WHSP Holdings research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free WHSP Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate WHSP Holdings' overall financial health at a glance.

Curious About Other Options?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Find companies with promising cash flow potential yet trading below their fair value.

- The end of cancer? These 28 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if WHSP Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:SOL

WHSP Holdings

An investment company, engages in investing various industries and asset classes in Australia.

Flawless balance sheet second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

93 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative