Advertisement

- Australia

- /

- Capital Markets

- /

- ASX:PL8

Four Days Left To Buy Plato Income Maximiser Limited (ASX:PL8) Before The Ex-Dividend Date

Plato Income Maximiser Limited (ASX:PL8) is about to trade ex-dividend in the next 4 days. If you purchase the stock on or after the 11th of February, you won't be eligible to receive this dividend, when it is paid on the 26th of February.

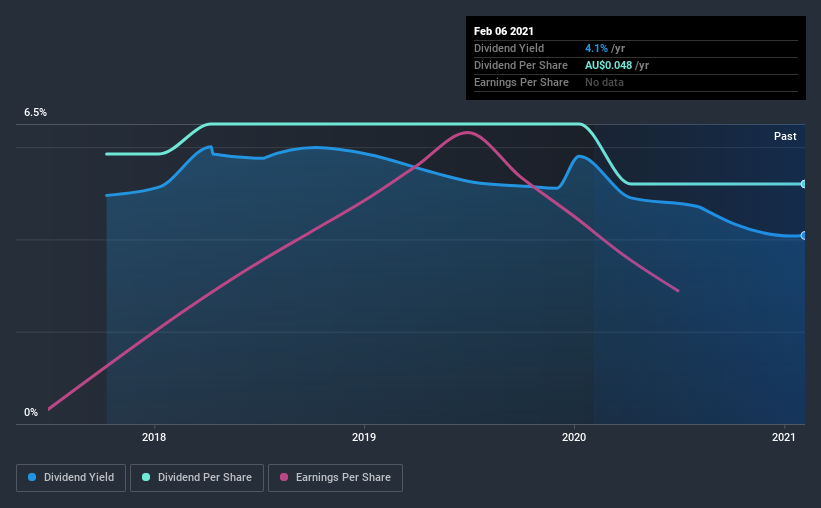

Plato Income Maximiser's next dividend payment will be AU$0.004 per share, and in the last 12 months, the company paid a total of AU$0.048 per share. Based on the last year's worth of payments, Plato Income Maximiser has a trailing yield of 4.1% on the current stock price of A$1.175. Dividends are a major contributor to investment returns for long term holders, but only if the dividend continues to be paid. So we need to check whether the dividend payments are covered, and if earnings are growing.

See our latest analysis for Plato Income Maximiser

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Plato Income Maximiser paid out 107% of its earnings, which is more than we're comfortable with, unless there are mitigating circumstances.

Generally, the higher a company's payout ratio, the more the dividend is at risk of being reduced.

Click here to see how much of its profit Plato Income Maximiser paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Businesses with strong growth prospects usually make the best dividend payers, because it's easier to grow dividends when earnings per share are improving. If earnings fall far enough, the company could be forced to cut its dividend. It's encouraging to see Plato Income Maximiser has grown its earnings rapidly, up 56% a year for the past three years.

Plato Income Maximiser also issued more than 5% of its market cap in new stock during the past year, which we feel is likely to hurt its dividend prospects in the long run. Trying to grow the dividend while issuing large amounts of new shares reminds us of the ancient Greek tale of Sisyphus - perpetually pushing a boulder uphill.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. Plato Income Maximiser's dividend payments per share have declined at 3.9% per year on average over the past three years, which is uninspiring. Plato Income Maximiser is a rare case where dividends have been decreasing at the same time as earnings per share have been improving. It's unusual to see, and could point to unstable conditions in the core business, or more rarely an intensified focus on reinvesting profits.

Final Takeaway

Has Plato Income Maximiser got what it takes to maintain its dividend payments? We're not enthused to see Plato Income Maximiser's dividend was not well covered by earnings over the last year, although it is great to see earnings growing. In sum this is a middling combination, and we find it hard to get excited about the company from a dividend perspective.

With that being said, if dividends aren't your biggest concern with Plato Income Maximiser, you should know about the other risks facing this business. Our analysis shows 2 warning signs for Plato Income Maximiser that we strongly recommend you have a look at before investing in the company.

A common investment mistake is buying the first interesting stock you see. Here you can find a list of promising dividend stocks with a greater than 2% yield and an upcoming dividend.

If you’re looking to trade Plato Income Maximiser, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:PL8

Flawless balance sheet with questionable track record.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor