Advertisement

- Australia

- /

- Capital Markets

- /

- ASX:CIN

Australian Undiscovered Gems Carlton Investments And 2 Others With Strong Potential

Simply Wall St

Reviewed by Simply Wall St

As the Australian market takes a breather following a year of record highs, investors are navigating a landscape marked by mixed sector performances and cautious sentiment. In this environment, identifying stocks with strong potential often involves looking beyond immediate market trends to find companies that demonstrate resilience and innovation, such as Carlton Investments and two other promising small-cap contenders.

Top 10 Undiscovered Gems With Strong Fundamentals In Australia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Sugar Terminals | NA | 3.78% | 4.30% | ★★★★★★ |

| Fiducian Group | NA | 10.00% | 9.57% | ★★★★★★ |

| Joyce | NA | 9.93% | 17.54% | ★★★★★★ |

| Spheria Emerging Companies | NA | -1.31% | 0.28% | ★★★★★★ |

| Hearts and Minds Investments | NA | 56.27% | 59.19% | ★★★★★★ |

| Red Hill Minerals | NA | 95.16% | 40.06% | ★★★★★★ |

| Djerriwarrh Investments | 2.39% | 8.18% | 7.91% | ★★★★★★ |

| Zimplats Holdings | 5.44% | -9.79% | -42.03% | ★★★★★☆ |

| Peet | 53.46% | 12.70% | 31.21% | ★★★★☆☆ |

| Australian United Investment | 1.90% | 5.23% | 4.56% | ★★★★☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

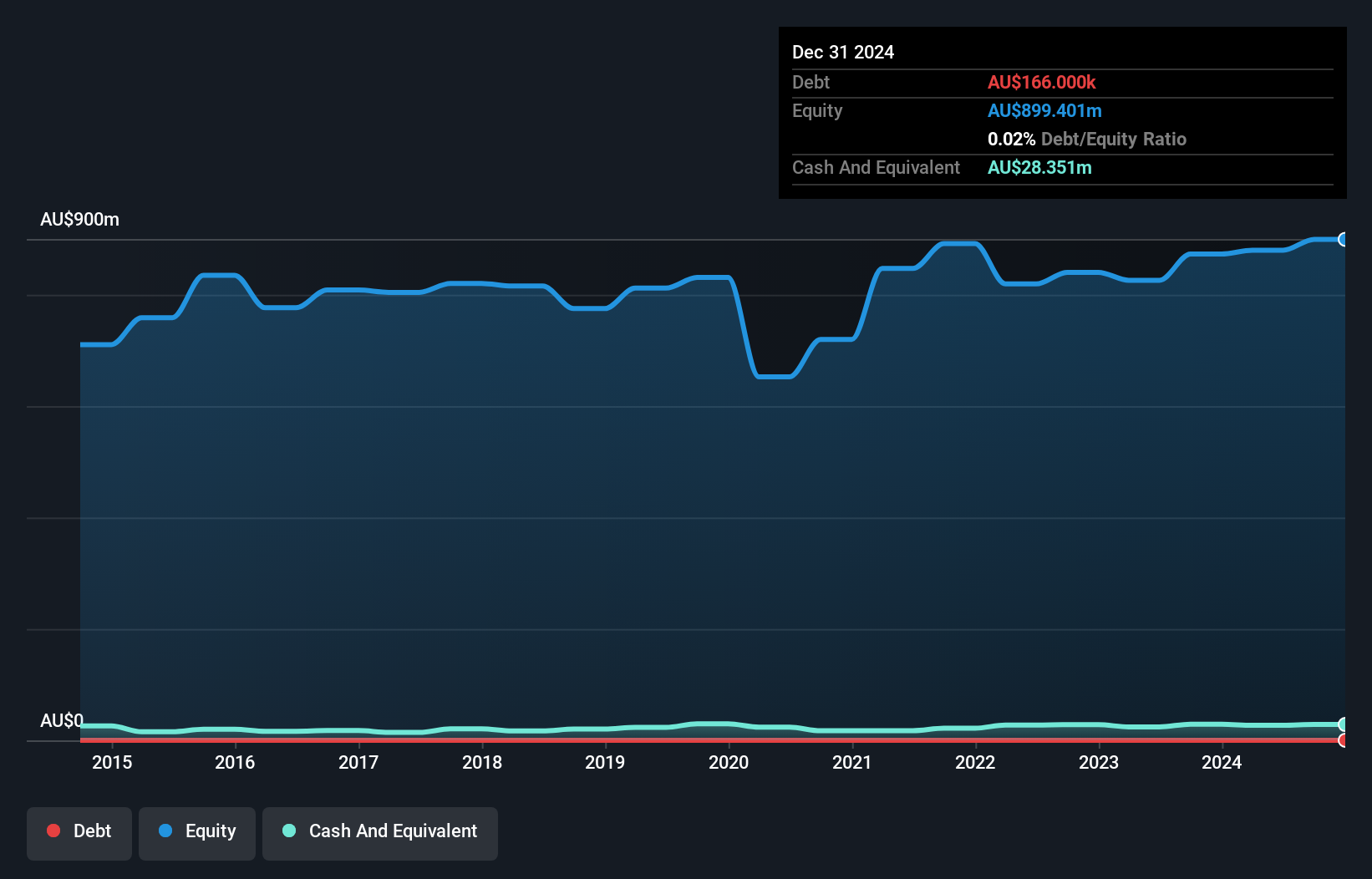

Carlton Investments (ASX:CIN)

Simply Wall St Value Rating: ★★★★★☆

Overview: Carlton Investments Limited is a publicly owned asset management holding company with a market capitalization of A$947.27 million.

Operations: Carlton Investments generates revenue primarily from the acquisition and long-term holding of shares and units, amounting to A$41.60 million. The company's net profit margin is a key financial metric to consider in evaluating its profitability.

Carlton Investments, a smaller player in the Australian market, showcases a solid financial standing with earnings growing at 8.7% annually over the past five years. The company boasts high-quality earnings and minimal debt concerns, as its debt-to-equity ratio has improved from 0.03% to 0.02%. Recent announcements reveal steady revenue of A$41.6 million and net income of A$38.81 million for the year ending June 2025, with basic EPS slightly up at A$1.468 from last year’s A$1.465. Additionally, Carlton's interest payments are well-covered by EBIT at an impressive coverage ratio of 3390x.

- Take a closer look at Carlton Investments' potential here in our health report.

Gain insights into Carlton Investments' past trends and performance with our Past report.

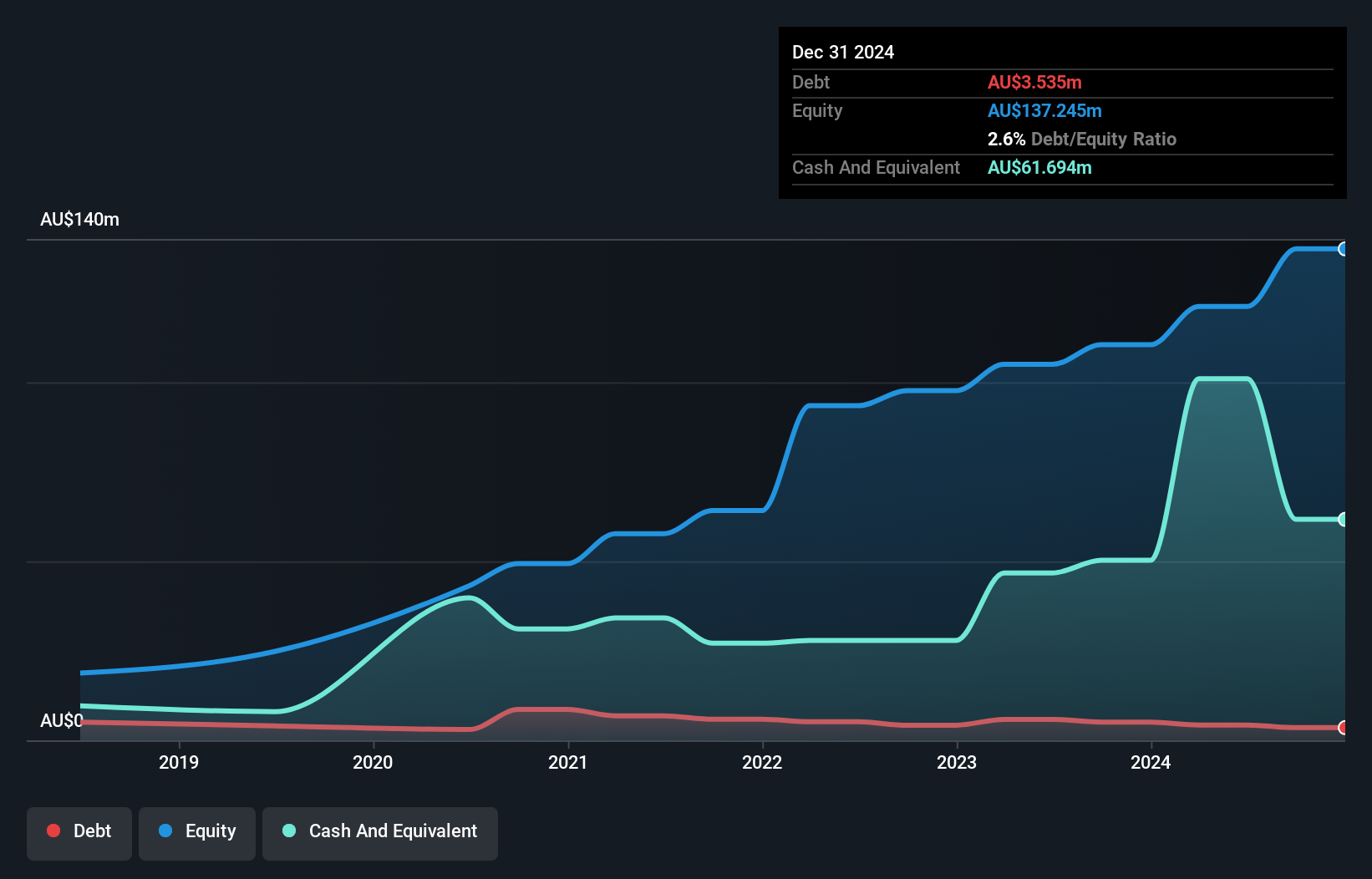

GenusPlus Group (ASX:GNP)

Simply Wall St Value Rating: ★★★★★★

Overview: GenusPlus Group Ltd specializes in the installation, construction, and maintenance of power and communication systems in Australia with a market capitalization of A$918.05 million.

Operations: GenusPlus Group Ltd generates revenue through three primary segments: Services (A$122.11 million), Infrastructure (A$405.10 million), and Energy & Engineering (A$224.06 million). The Infrastructure segment contributes the largest portion to the company's revenue stream.

GenusPlus Group, a dynamic player in Australia's power and communication systems sector, showcases promising growth potential through strategic acquisitions like CommTel. Recent financials reveal sales of A$751.27 million for the year ending June 2025, up from A$551.19 million previously, with net income climbing to A$35.37 million from A$19.26 million last year. Earnings per share improved to A$0.1975 from A$0.1084, indicating robust performance amidst expansion efforts and a focus on high-margin services integration. While challenges such as resource management and acquisition costs loom, analysts forecast continued revenue growth at 20% annually over the next few years.

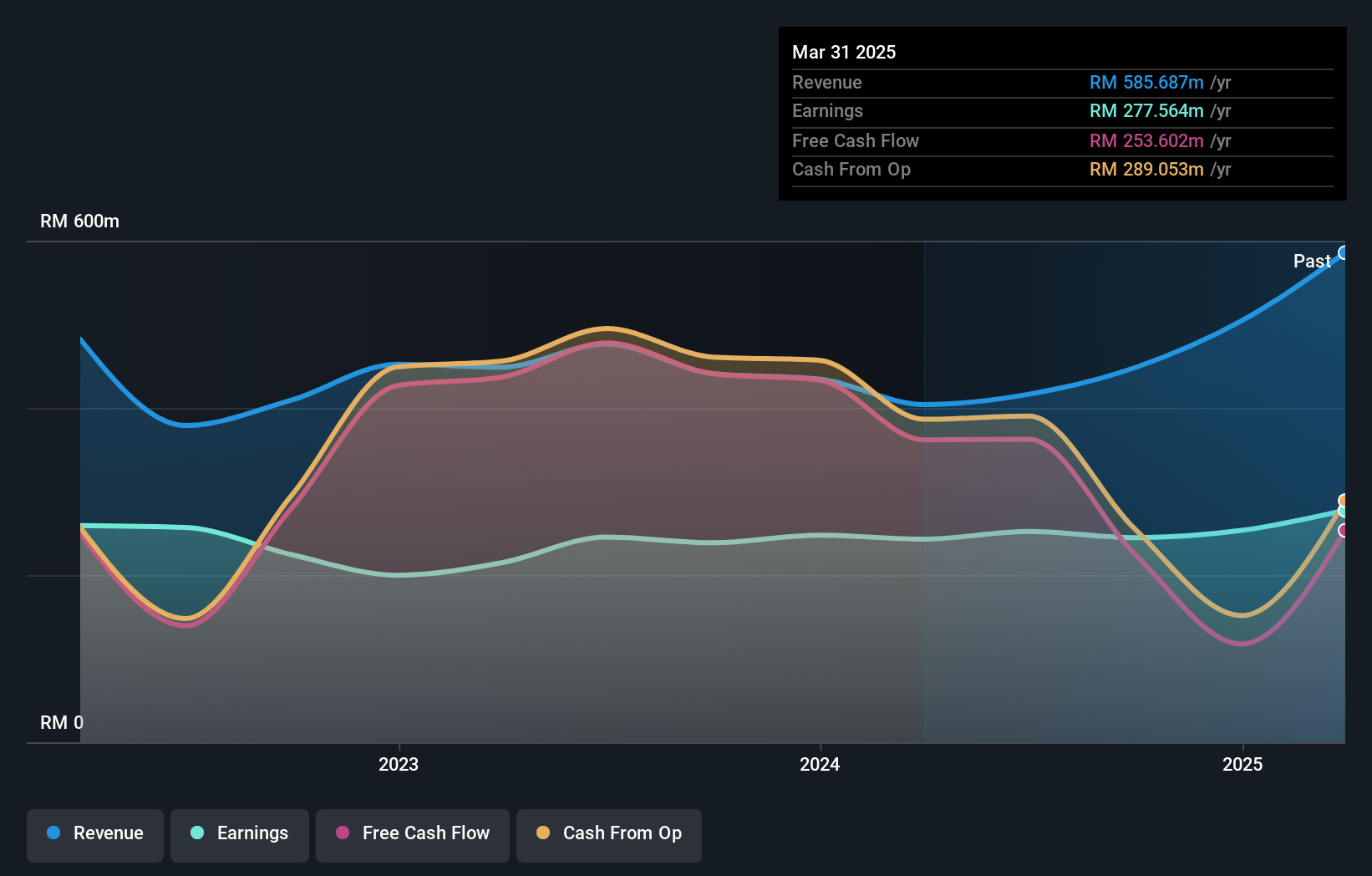

United Overseas Australia (ASX:UOS)

Simply Wall St Value Rating: ★★★★★☆

Overview: United Overseas Australia Ltd, along with its subsidiaries, focuses on the development and resale of land and buildings across Malaysia, Singapore, Vietnam, and Australia with a market capitalization of A$1.07 billion.

Operations: United Overseas Australia's primary revenue stream is derived from land development and resale, generating A$438.18 million, while its investment segment contributes A$257.51 million.

United Overseas Australia, a notable player in the real estate sector, showcases a P/E ratio of 10.5x, which is favorable compared to the broader Australian market's 20x. The company has reported net income of A$44.61 million for the half-year ending June 2025, up from A$33.92 million previously, reflecting solid earnings growth of 1.7% annually over five years. Despite a debt-to-equity increase from 5.5% to 8.8%, UOS maintains more cash than its total debt and continues to generate positive free cash flow at A$99.63 million as of June 2025, indicating robust financial health and potential for future stability amidst industry challenges.

Seize The Opportunity

- Investigate our full lineup of 53 ASX Undiscovered Gems With Strong Fundamentals right here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:CIN

Carlton Investments

Carlton Investments Limited is a publicly owned asset management holding company.

Excellent balance sheet average dividend payer.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor