- Australia

- /

- Consumer Services

- /

- ASX:SHJ

Here's Why We Think Shine Justice Ltd's (ASX:SHJ) CEO Compensation Looks Fair for the time being

Under the guidance of CEO Simon Morrison, Shine Justice Ltd (ASX:SHJ) has performed reasonably well recently. This is something shareholders will keep in mind as they cast their votes on company resolutions such as executive remuneration in the upcoming AGM on 20 October 2021. Here is our take on why we think the CEO compensation looks appropriate.

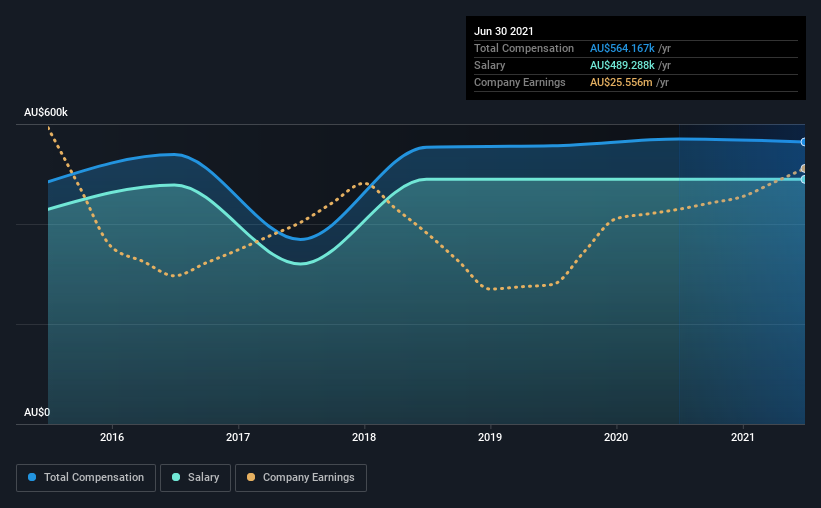

View our latest analysis for Shine Justice

Comparing Shine Justice Ltd's CEO Compensation With the industry

According to our data, Shine Justice Ltd has a market capitalization of AU$226m, and paid its CEO total annual compensation worth AU$564k over the year to June 2021. That's mostly flat as compared to the prior year's compensation. We note that the salary portion, which stands at AU$489.3k constitutes the majority of total compensation received by the CEO.

On comparing similar companies from the same industry with market caps ranging from AU$136m to AU$543m, we found that the median CEO total compensation was AU$519k. From this we gather that Simon Morrison is paid around the median for CEOs in the industry. Furthermore, Simon Morrison directly owns AU$55m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2021 | 2020 | Proportion (2021) |

| Salary | AU$489k | AU$489k | 87% |

| Other | AU$75k | AU$81k | 13% |

| Total Compensation | AU$564k | AU$570k | 100% |

On an industry level, roughly 62% of total compensation represents salary and 38% is other remuneration. According to our research, Shine Justice has allocated a higher percentage of pay to salary in comparison to the wider industry. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

A Look at Shine Justice Ltd's Growth Numbers

Over the past three years, Shine Justice Ltd has seen its earnings per share (EPS) grow by 9.9% per year. It achieved revenue growth of 5.9% over the last year.

We would argue that the improvement in revenue is good, but isn't particularly impressive, but we're happy with the modest EPS growth. It's clear the performance has been quite decent, but it it falls short of outstanding,based on this information. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has Shine Justice Ltd Been A Good Investment?

Most shareholders would probably be pleased with Shine Justice Ltd for providing a total return of 73% over three years. As a result, some may believe the CEO should be paid more than is normal for companies of similar size.

To Conclude...

Seeing that the company has put up a decent performance, only a few shareholders, if any at all, might have questions about the CEO pay in the upcoming AGM. In saying that, any proposed increase to CEO compensation will still be assessed on how reasonable it is based on performance and industry benchmarks.

CEO compensation is a crucial aspect to keep your eyes on but investors also need to keep their eyes open for other issues related to business performance. That's why we did some digging and identified 1 warning sign for Shine Justice that investors should think about before committing capital to this stock.

Switching gears from Shine Justice, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:SHJ

Shine Justice

Through its subsidiaries, provides damages-based plaintiff litigation legal services in Australia and New Zealand.

Adequate balance sheet with moderate growth potential.

Market Insights

Community Narratives