Advertisement

- Australia

- /

- Consumer Services

- /

- ASX:NDO

Nido Education Limited (ASX:NDO) Analysts Are Cutting Their Estimates: Here's What You Need To Know

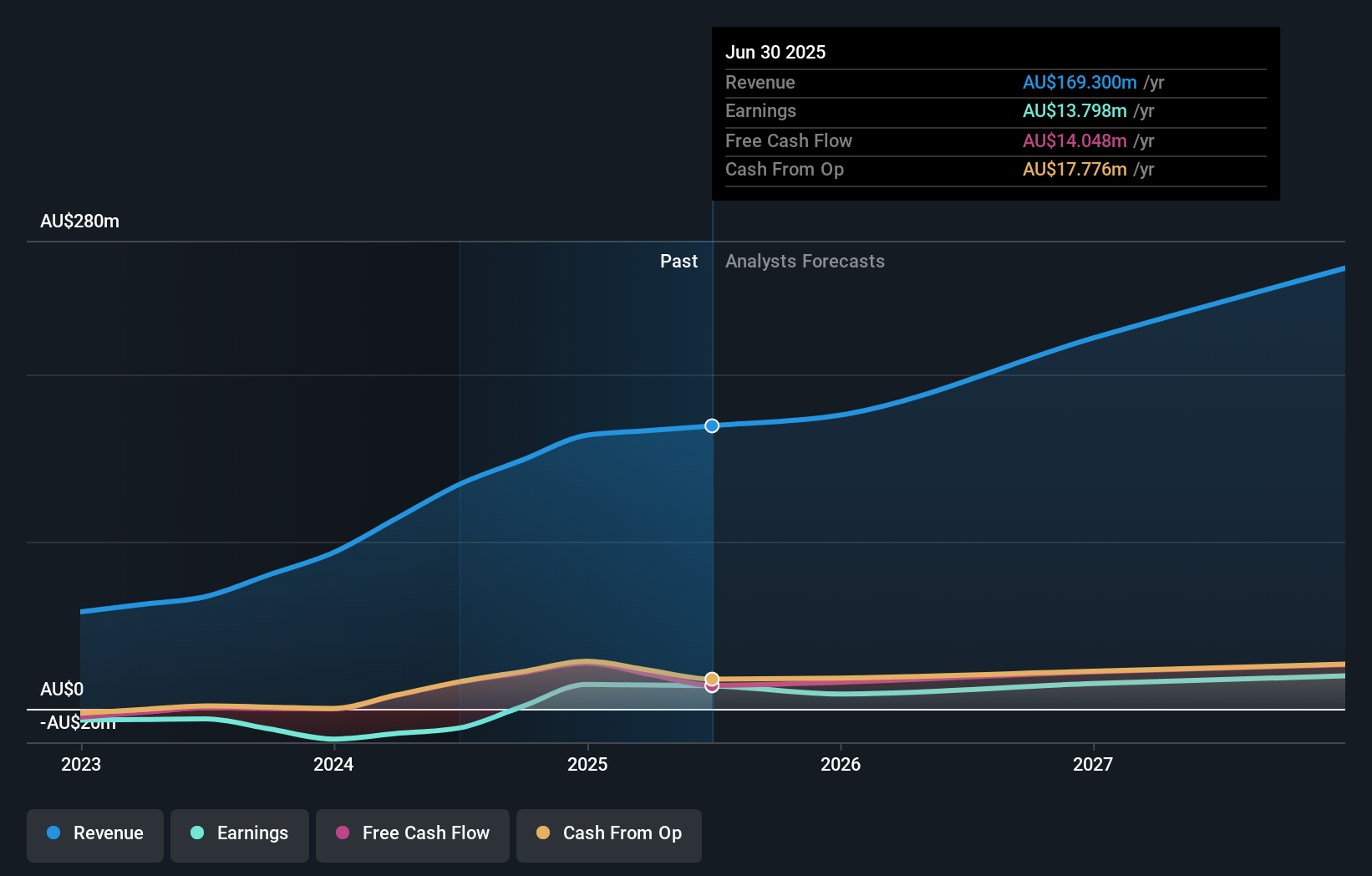

Shareholders might have noticed that Nido Education Limited (ASX:NDO) filed its half-year result this time last week. The early response was not positive, with shares down 5.0% to AU$0.66 in the past week. Results look mixed - while revenue fell marginally short of analyst estimates at AU$81m, statutory earnings were in line with expectations, at AU$0.064 per share. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. We thought readers would find it interesting to see the analysts latest (statutory) post-earnings forecasts for next year.

After the latest results, the four analysts covering Nido Education are now predicting revenues of AU$175.6m in 2025. If met, this would reflect an okay 3.7% improvement in revenue compared to the last 12 months. Statutory earnings per share are expected to nosedive 35% to AU$0.04 in the same period. Yet prior to the latest earnings, the analysts had been anticipated revenues of AU$192.5m and earnings per share (EPS) of AU$0.058 in 2025. The analysts seem less optimistic after the recent results, reducing their revenue forecasts and making a large cut to earnings per share numbers.

Check out our latest analysis for Nido Education

It'll come as no surprise then, to learn that the analysts have cut their price target 7.8% to AU$1.09. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. Currently, the most bullish analyst values Nido Education at AU$1.30 per share, while the most bearish prices it at AU$0.92. There are definitely some different views on the stock, but the range of estimates is not wide enough as to imply that the situation is unforecastable, in our view.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. It's pretty clear that there is an expectation that Nido Education's revenue growth will slow down substantially, with revenues to the end of 2025 expected to display 7.6% growth on an annualised basis. This is compared to a historical growth rate of 26% over the past year. Compare this to the 14 other companies in this industry with analyst coverage, which are forecast to grow their revenue at 7.1% per year. Factoring in the forecast slowdown in growth, it looks like Nido Education is forecast to grow at about the same rate as the wider industry.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for Nido Education. They also downgraded their revenue estimates, although as we saw earlier, forecast growth is only expected to be about the same as the wider industry. The consensus price target fell measurably, with the analysts seemingly not reassured by the latest results, leading to a lower estimate of Nido Education's future valuation.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. At Simply Wall St, we have a full range of analyst estimates for Nido Education going out to 2027, and you can see them free on our platform here..

Don't forget that there may still be risks. For instance, we've identified 1 warning sign for Nido Education that you should be aware of.

Valuation is complex, but we're here to simplify it.

Discover if Nido Education might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:NDO

Nido Education

Owns, operates, and manages long day early childhood education and care centres under the Nido Early School brand in Australia.

Undervalued with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Defense AI: A Robotic Response to America’s Security Gaps

Fair Value US$12.00|49.7% undervalued

MA

Community Contributor

Figma (FIG): The S&P 500’s Design Standard Turning Into an All-in-One Platform

Fair Value US$65.70|7.0% overvalued

TI

Community Contributor

Sleep Cycle's Revenue Set to Rise 10% with Strong Revenue Model

Fair Value SEK 38.04|20.3% undervalued

MA

Community Contributor

Has JB Hi-Fi Lost Its Point of Difference?

Fair Value AU$76.00|54.2% overvalued

RO

Community Contributor