- Australia

- /

- Consumer Services

- /

- ASX:KED

Growth Investors: Industry Analysts Just Upgraded Their Keypath Education International, Inc. (ASX:KED) Revenue Forecasts By 19%

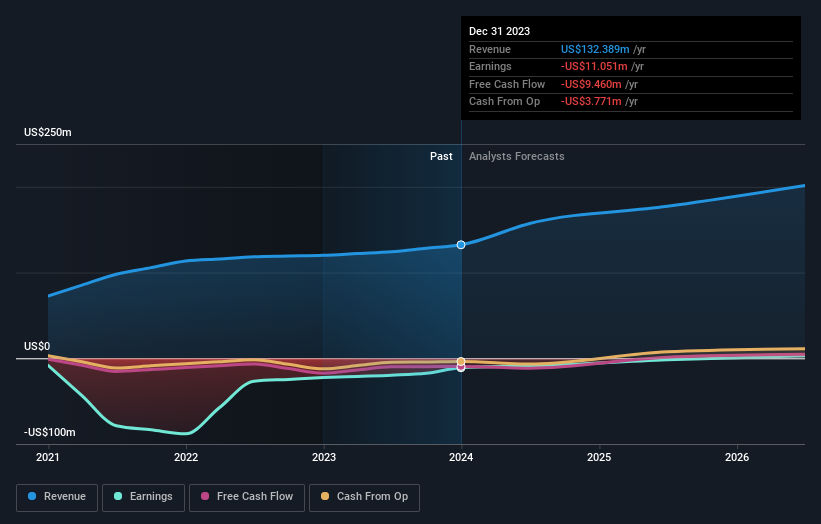

Keypath Education International, Inc. (ASX:KED) shareholders will have a reason to smile today, with the analysts making substantial upgrades to this year's statutory forecasts. The revenue forecast for this year has experienced a facelift, with the analysts now much more optimistic on its sales pipeline. Investors have been pretty optimistic on Keypath Education International too, with the stock up 32% to AU$0.62 over the past week. We'll be curious to see if these new estimates convince the market to lift the stock price higher still.

After the upgrade, the four analysts covering Keypath Education International are now predicting revenues of US$157m in 2024. If met, this would reflect a meaningful 19% improvement in sales compared to the last 12 months. Losses are forecast to narrow 8.6% to US$0.047 per share. Yet before this consensus update, the analysts had been forecasting revenues of US$132m and losses of US$0.051 per share in 2024. We can see there's definitely been a change in sentiment in this update, with the analysts administering a sizeable upgrade to this year's revenue estimates, while at the same time reducing their loss estimates.

See our latest analysis for Keypath Education International

Yet despite these upgrades, the analysts cut their price target 8.4% to US$0.67, implicitly signalling that the ongoing losses are likely to weigh negatively on Keypath Education International's valuation. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. The most optimistic Keypath Education International analyst has a price target of US$1.17 per share, while the most pessimistic values it at US$0.34. So we wouldn't be assigning too much credibility to analyst price targets in this case, because there are clearly some widely differing views on what kind of performance this business can generate. With this in mind, we wouldn't rely too heavily on the consensus price target, as it is just an average and analysts clearly have some deeply divergent views on the business.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. The analysts are definitely expecting Keypath Education International's growth to accelerate, with the forecast 19% annualised growth to the end of 2024 ranking favourably alongside historical growth of 15% per annum over the past three years. Compare this with other companies in the same industry, which are forecast to grow their revenue 9.8% annually. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect Keypath Education International to grow faster than the wider industry.

The Bottom Line

The highlight for us was that the consensus reduced its estimated losses this year, perhaps suggesting Keypath Education International is moving incrementally towards profitability. They also upgraded their revenue estimates for this year, and sales are expected to grow faster than the wider market. The consensus price target fell measurably, with analysts seemingly not reassured by recent business developments, leading to a lower estimate of Keypath Education International's future valuation. Given that analysts appear to be expecting substantial improvement in the sales pipeline, now could be the right time to take another look at Keypath Education International.

Better yet, Keypath Education International is expected to break-even soon - within the next few years - according to analyst forecasts, which would be a momentous event for shareholders. For more information, you can click through to our free platform to learn more about these forecasts.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are upgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

If you're looking to trade Keypath Education International, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Keypath Education International might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:KED

Keypath Education International

Designs, develops, and delivers career-relevant online education solutions in North America, the Asia-Pacific, and internationally.

Flawless balance sheet and good value.

Market Insights

Community Narratives