- Australia

- /

- Metals and Mining

- /

- ASX:EMR

Top ASX Growth Stocks With High Insider Ownership September 2024

Reviewed by Simply Wall St

The Australian market has been buoyant, with the ASX200 closing up a fifth of a percent at 8,209 points, just below its all-time high. Investors are optimistic about the potential impact of a US Fed rate cut on global economic conditions. In this favorable market environment, identifying growth companies with high insider ownership can be particularly rewarding. Such stocks often benefit from strong internal confidence and alignment between management and shareholders' interests.

Top 10 Growth Companies With High Insider Ownership In Australia

| Name | Insider Ownership | Earnings Growth |

| Clinuvel Pharmaceuticals (ASX:CUV) | 10.4% | 27.4% |

| Catalyst Metals (ASX:CYL) | 17% | 54.5% |

| Genmin (ASX:GEN) | 12% | 117.7% |

| AVA Risk Group (ASX:AVA) | 15.7% | 118.8% |

| Pointerra (ASX:3DP) | 18.7% | 126.4% |

| Liontown Resources (ASX:LTR) | 16.4% | 69.4% |

| Hillgrove Resources (ASX:HGO) | 10.4% | 70.9% |

| Acrux (ASX:ACR) | 17.4% | 91.6% |

| Adveritas (ASX:AV1) | 21.1% | 144.2% |

| Plenti Group (ASX:PLT) | 12.8% | 106.4% |

Here we highlight a subset of our preferred stocks from the screener.

Emerald Resources (ASX:EMR)

Simply Wall St Growth Rating: ★★★★★★

Overview: Emerald Resources NL focuses on the exploration and development of mineral reserves in Cambodia and Australia, with a market cap of A$2.57 billion.

Operations: Emerald Resources generates revenue primarily from its mine operations, amounting to A$366.04 million.

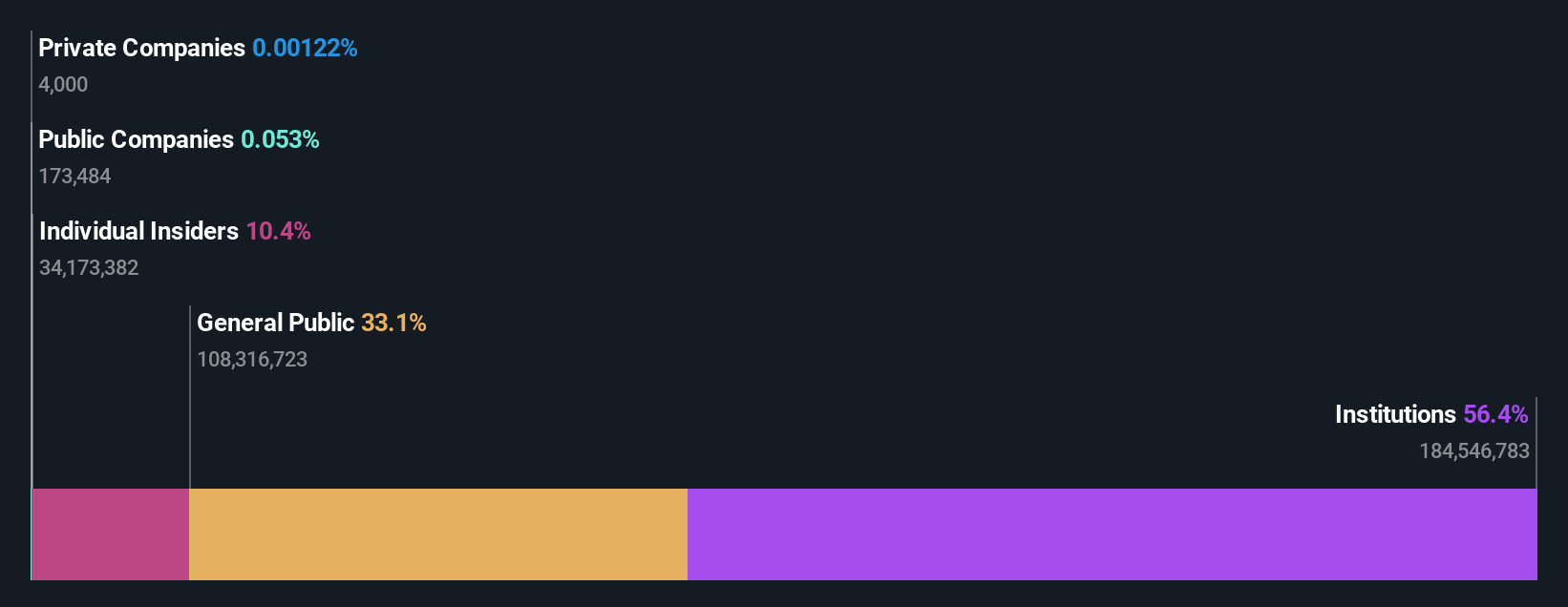

Insider Ownership: 18%

Earnings Growth Forecast: 30.1% p.a.

Emerald Resources has demonstrated robust growth, with earnings rising from A$59.36 million to A$84.27 million year-over-year and revenue increasing to A$371.07 million. The company’s earnings are forecasted to grow at 30.1% annually, significantly outpacing the Australian market's 12.3%. Trading at 59% below its estimated fair value, Emerald Resources presents a compelling case for growth investors, bolstered by high insider ownership and strong financial performance indicators like a projected 20% return on equity in three years.

- Delve into the full analysis future growth report here for a deeper understanding of Emerald Resources.

- Our expertly prepared valuation report Emerald Resources implies its share price may be too high.

Flight Centre Travel Group (ASX:FLT)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Flight Centre Travel Group Limited (ASX:FLT) offers travel retailing services for both leisure and corporate clients across various regions including Australia, New Zealand, the Americas, Europe, the Middle East, Africa and Asia with a market cap of A$4.83 billion.

Operations: The company's revenue segments include A$1.35 billion from leisure travel and A$1.11 billion from corporate travel services.

Insider Ownership: 13.5%

Earnings Growth Forecast: 19.7% p.a.

Flight Centre Travel Group has shown strong growth, with earnings rising from A$47 million to A$139 million year-over-year and revenue increasing to A$2.71 billion. The company's earnings are forecasted to grow at 19.7% annually, outpacing the Australian market's 12.3%. Recent initiatives include seeking acquisitions and doubling Cruise & Touring sales, supported by a solid cash position. Despite an unstable dividend track record, it trades at 14.4% below estimated fair value.

- Take a closer look at Flight Centre Travel Group's potential here in our earnings growth report.

- The analysis detailed in our Flight Centre Travel Group valuation report hints at an inflated share price compared to its estimated value.

Technology One (ASX:TNE)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Technology One Limited develops, markets, sells, implements, and supports integrated enterprise business software solutions in Australia and internationally with a market cap of A$7.80 billion.

Operations: The company's revenue segments are comprised of Software (A$317.24 million), Corporate (A$83.83 million), and Consulting (A$68.13 million).

Insider Ownership: 12.3%

Earnings Growth Forecast: 14.8% p.a.

Technology One demonstrates robust growth potential, with earnings forecasted to grow 14.79% annually, outpacing the Australian market's 12.3%. The company's revenue is expected to rise by 11.5% per year, faster than the market's 5.4%. Recent developments include appointing Paul Robson as an independent Non-Executive Director, bringing significant SaaS and strategic transformation expertise from his tenure at Adobe. This leadership addition aims to bolster Technology One's global SaaS platform expansion efforts.

- Navigate through the intricacies of Technology One with our comprehensive analyst estimates report here.

- According our valuation report, there's an indication that Technology One's share price might be on the expensive side.

Key Takeaways

- Click this link to deep-dive into the 100 companies within our Fast Growing ASX Companies With High Insider Ownership screener.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Emerald Resources might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:EMR

Emerald Resources

Engages in the exploration and development of mineral reserves in Cambodia and Australia.

Exceptional growth potential with excellent balance sheet.