Stock Analysis

Flight Centre Travel Group And 2 More ASX Stocks Estimated Below Intrinsic Value

Reviewed by Simply Wall St

The Australian stock market has experienced a slight downturn over the last week, falling by 1.4%, though it remains up by 6.5% over the past year with earnings expected to grow by 13% annually. In such a fluctuating environment, identifying stocks that are potentially undervalued can offer opportunities for investors looking for value in a growing market.

Top 10 Undervalued Stocks Based On Cash Flows In Australia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| GTN (ASX:GTN) | A$0.445 | A$0.85 | 47.4% |

| MaxiPARTS (ASX:MXI) | A$2.04 | A$3.94 | 48.2% |

| ReadyTech Holdings (ASX:RDY) | A$3.25 | A$6.26 | 48% |

| Australian Clinical Labs (ASX:ACL) | A$2.48 | A$4.73 | 47.5% |

| Strike Energy (ASX:STX) | A$0.225 | A$0.45 | 50.3% |

| IPH (ASX:IPH) | A$6.25 | A$12.00 | 47.9% |

| Regal Partners (ASX:RPL) | A$3.29 | A$6.18 | 46.8% |

| Core Lithium (ASX:CXO) | A$0.085 | A$0.17 | 49.5% |

| Millennium Services Group (ASX:MIL) | A$1.145 | A$2.24 | 48.9% |

| SiteMinder (ASX:SDR) | A$5.20 | A$10.02 | 48.1% |

Let's review some notable picks from our screened stocks

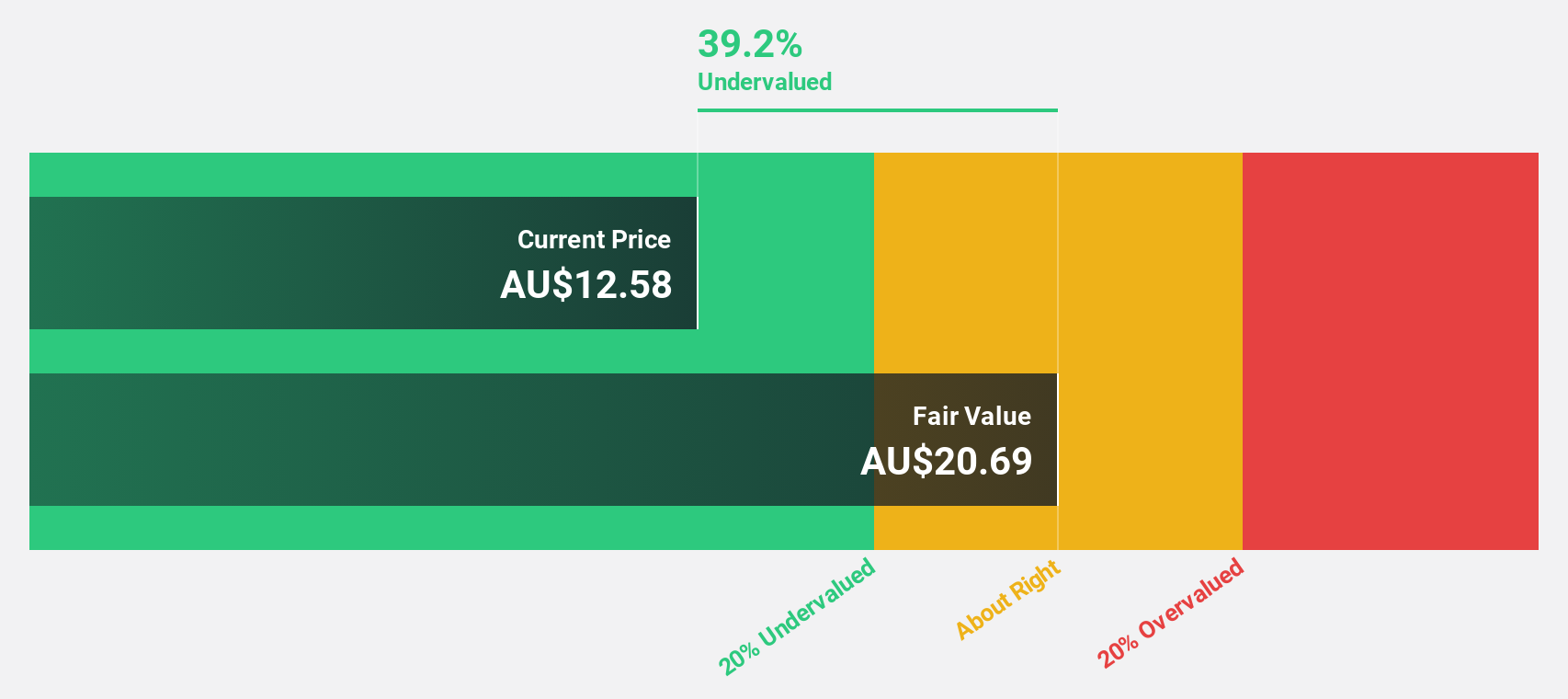

Flight Centre Travel Group (ASX:FLT)

Overview: Flight Centre Travel Group Limited operates as a travel retailer serving both leisure and corporate sectors across regions including Australia, New Zealand, the Americas, Europe, the Middle East, Africa, and Asia with a market capitalization of approximately A$4.54 billion.

Operations: The company's revenue is primarily derived from its leisure and corporate travel services, generating A$1.28 billion and A$1.06 billion respectively.

Estimated Discount To Fair Value: 19.7%

Flight Centre Travel Group (FLT), priced at A$20.63, is trading below our estimated fair value of A$25.62, indicating a potential undervaluation. Recently profitable, FLT's earnings are expected to increase by 18.8% annually, outpacing the Australian market forecast of 13%. Despite this growth, its revenue increase of 9.7% annually exceeds the market's 5.2%, but does not reach high growth thresholds. With a projected high return on equity of 21.8% in three years, FLT combines solid profitability prospects with moderate undervaluation based on cash flows.

- Upon reviewing our latest growth report, Flight Centre Travel Group's projected financial performance appears quite optimistic.

- Click here and access our complete balance sheet health report to understand the dynamics of Flight Centre Travel Group.

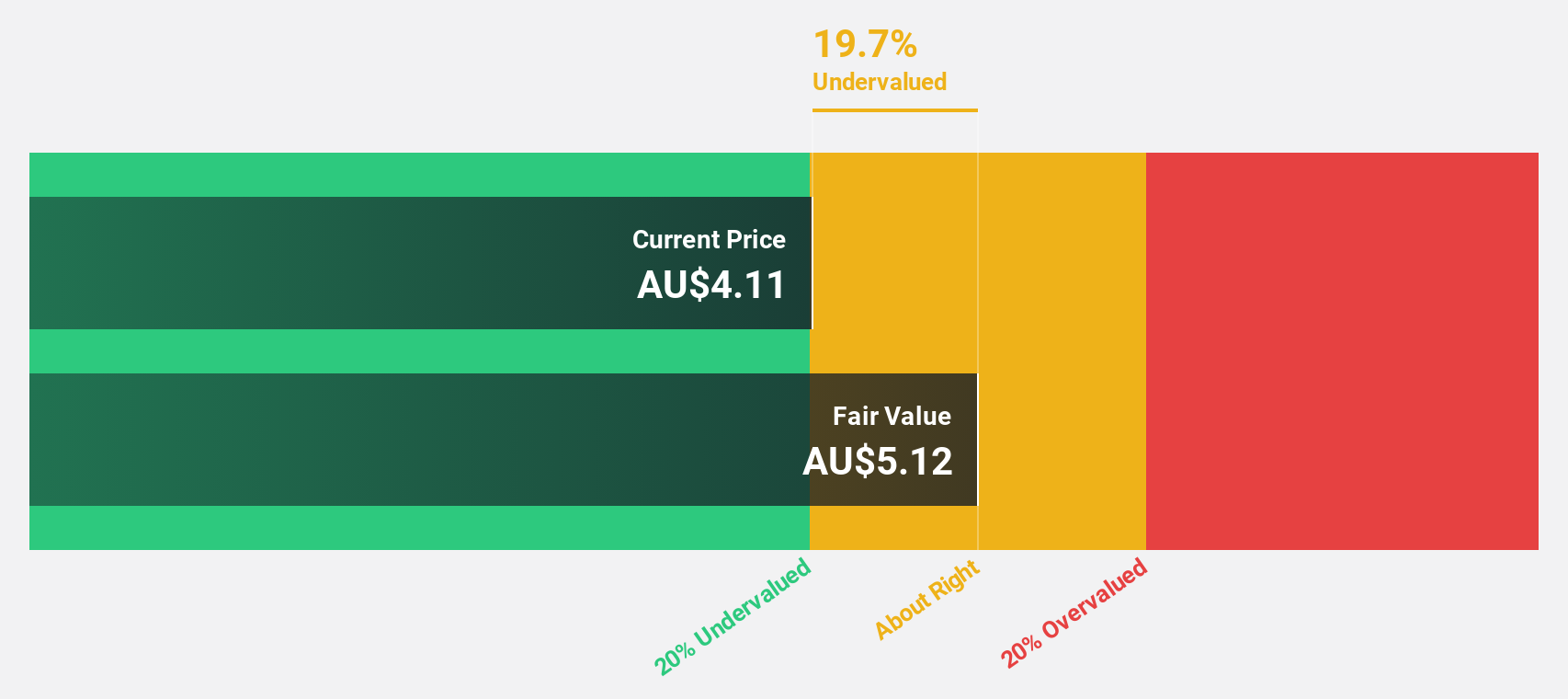

HMC Capital (ASX:HMC)

Overview: HMC Capital Limited, operating in Australia, manages real estate-focused funds with a market capitalization of approximately A$2.63 billion.

Operations: The firm oversees funds concentrated on real estate, generating revenues of approximately A$80.29 million.

Estimated Discount To Fair Value: 43.1%

HMC Capital, with a current price of A$7.14, appears undervalued against a fair value estimate of A$12.55, reflecting a significant discount. The company's revenue growth is robust at 20.1% annually, outperforming the Australian market's 5.2%. Despite recent shareholder dilution from multiple equity offerings totaling A$188.30 million, HMC’s earnings are poised to grow by 16.9% per year, surpassing the market average of 13%. However, its forecasted return on equity in three years is relatively low at 10.5%.

- Our earnings growth report unveils the potential for significant increases in HMC Capital's future results.

- Click here to discover the nuances of HMC Capital with our detailed financial health report.

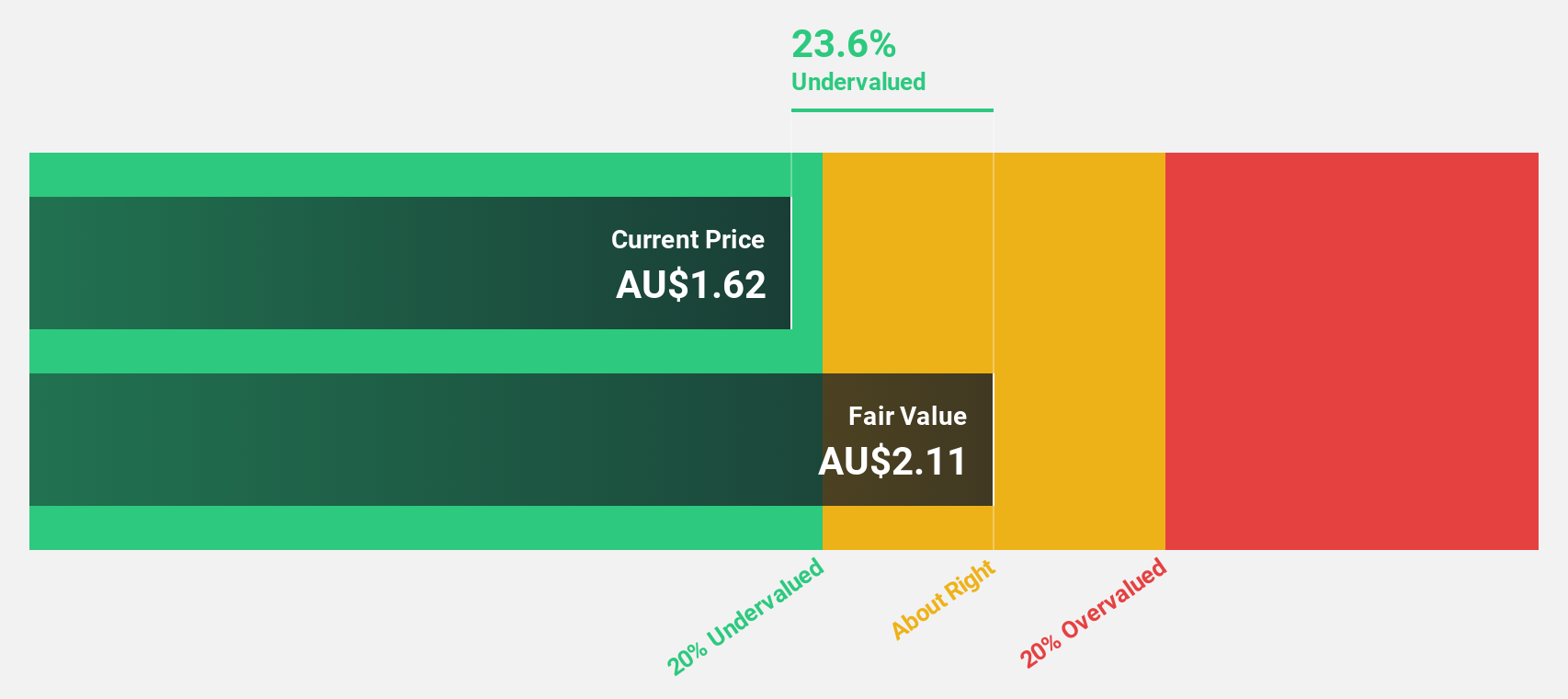

Judo Capital Holdings (ASX:JDO)

Overview: Judo Capital Holdings Limited, operating in Australia, offers a range of banking products and services tailored to small and medium-sized businesses, with a market capitalization of approximately A$1.38 billion.

Operations: The company generates revenue primarily through its banking segment, totaling A$328.70 million.

Estimated Discount To Fair Value: 10.3%

Judo Capital Holdings, priced at A$1.24, trades below its calculated fair value of A$1.38. While its revenue growth is projected at 16.6% annually, outpacing the Australian market's average of 5.2%, its earnings are expected to increase by 26.32% per year, also above the national trend of 13%. Recently added to the S&P/ASX 200 Index, Judo shows potential despite a modest forecasted return on equity of 10.1% in three years and a valuation that is not significantly undervalued based on discounted cash flows.

- Our comprehensive growth report raises the possibility that Judo Capital Holdings is poised for substantial financial growth.

- Unlock comprehensive insights into our analysis of Judo Capital Holdings stock in this financial health report.

Taking Advantage

- Reveal the 49 hidden gems among our Undervalued ASX Stocks Based On Cash Flows screener with a single click here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're helping make it simple.

Find out whether Judo Capital Holdings is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:JDO

Judo Capital Holdings

Provides various banking products and services for small and medium businesses in Australia.

Solid track record with excellent balance sheet.