Advertisement

- Australia

- /

- Consumer Services

- /

- ASX:3PL

Does 3P Learning Limited's (ASX:3PL) CEO Salary Compare Well With Others?

Want to participate in a short research study? Help shape the future of investing tools and receive a $20 prize!

Rebekah O’Flaherty became the CEO of 3P Learning Limited (ASX:3PL) in 2016. This report will, first, examine the CEO compensation levels in comparison to CEO compensation at companies of similar size. Next, we'll consider growth that the business demonstrates. Third, we'll reflect on the total return to shareholders over three years, as a second measure of business performance. This process should give us an idea about how appropriately the CEO is paid.

View our latest analysis for 3P Learning

How Does Rebekah O’Flaherty's Compensation Compare With Similar Sized Companies?

At the time of writing our data says that 3P Learning Limited has a market cap of AU$153m, and is paying total annual CEO compensation of AU$1.0m. (This number is for the twelve months until 2018). We think total compensation is more important but we note that the CEO salary is lower, at AU$585k. We took a group of companies with market capitalizations below AU$279m, and calculated the median CEO compensation to be AU$362k.

It would therefore appear that 3P Learning Limited pays Rebekah O’Flaherty more than the median CEO remuneration at companies of a similar size, in the same market. However, this fact alone doesn't mean the remuneration is too high. We can better assess whether the pay is overly generous by looking into the underlying business performance.

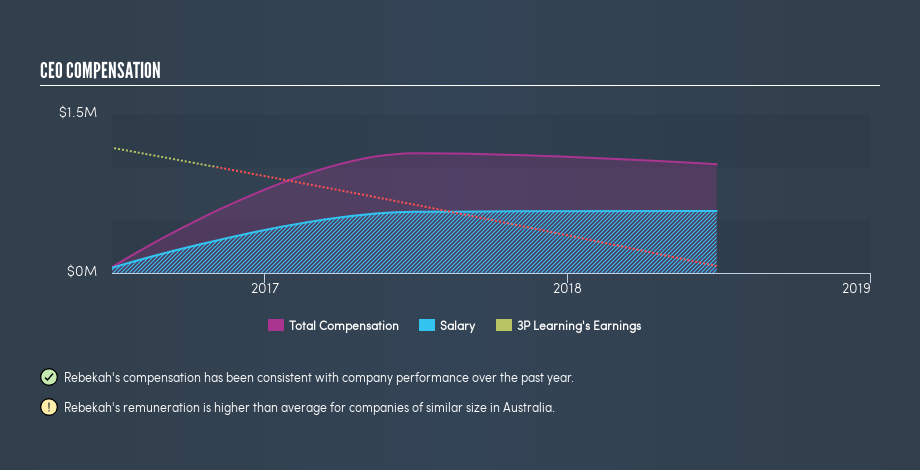

You can see a visual representation of the CEO compensation at 3P Learning, below.

Is 3P Learning Limited Growing?

3P Learning Limited has reduced its earnings per share by an average of 85% a year, over the last three years (measured with a line of best fit). In the last year, its revenue is up 5.6%.

Few shareholders would be pleased to read that earnings per share are lower over three years. The modest increase in revenue in the last year isn't enough to make me overlook the disappointing change in earnings per share. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO. It could be important to check this free visual depiction of what analysts expect for the future.

Has 3P Learning Limited Been A Good Investment?

With a three year total loss of 22%, 3P Learning Limited would certainly have some dissatisfied shareholders. It therefore might be upsetting for shareholders if the CEO were paid generously.

In Summary...

We compared total CEO remuneration at 3P Learning Limited with the amount paid at companies with a similar market capitalization. We found that it pays well over the median amount paid in the benchmark group.

We think many shareholders would be underwhelmed with the business growth over the last three years.Just as bad, share price gains for investors have failed to materialize, over the same period. This analysis suggests to us that the CEO is paid too generously! Whatever your view on compensation, you might want to check if insiders are buying or selling 3P Learning shares (free trial).

Important note: 3P Learning may not be the best stock to buy. You might find something better in this list of interesting companies with high ROE and low debt.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About ASX:3PL

3P Learning

Engages in the development, marketing, and sale of educational software and e-books to schools and parents of school-aged students in the Asia-Pacific, North and South America, Europe, the Middle East, and Africa.

Moderate growth potential and slightly overvalued.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.1% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|20.9% undervalued

TI

Community Contributor