Advertisement

- Australia

- /

- Commercial Services

- /

- ASX:MSG

This Is Why Shareholders May Want To Hold Back On A Pay Rise For MCS Services Limited's (ASX:MSG) CEO

Key Insights

- MCS Services will host its Annual General Meeting on 30th of November

- CEO Paul Simmons' total compensation includes salary of AU$196.4k

- Total compensation is 43% below industry average

- MCS Services' EPS declined by 71% over the past three years while total shareholder loss over the past three years was 38%

Performance at MCS Services Limited (ASX:MSG) has not been particularly rosy recently and shareholders will likely be holding CEO Paul Simmons and the board accountable for this. The next AGM coming up on 30th of November will be a chance for shareholders to have their concerns addressed by the board, challenge management on company strategy and vote on resolutions such as executive remuneration, which may help change the company's future prospects. From our analysis below, we think CEO compensation looks appropriate for now.

View our latest analysis for MCS Services

How Does Total Compensation For Paul Simmons Compare With Other Companies In The Industry?

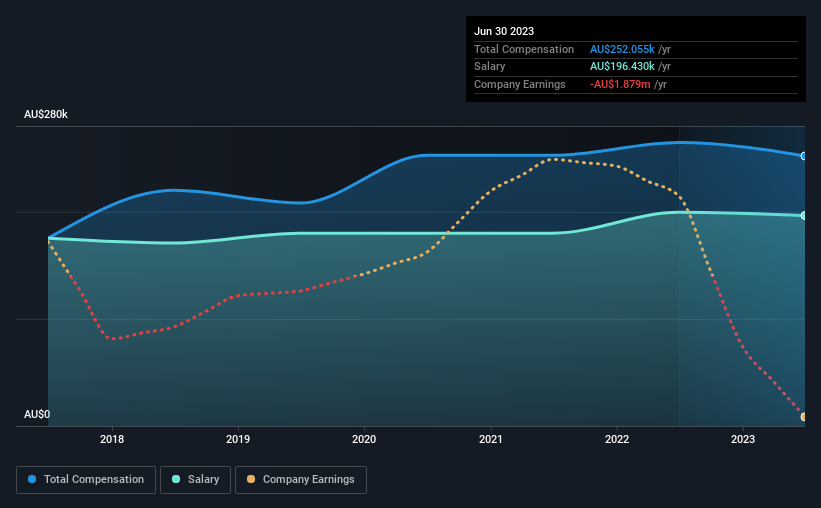

According to our data, MCS Services Limited has a market capitalization of AU$4.0m, and paid its CEO total annual compensation worth AU$252k over the year to June 2023. That's slightly lower by 4.8% over the previous year. Notably, the salary which is AU$196.4k, represents most of the total compensation being paid.

On comparing similar-sized companies in the Australian Commercial Services industry with market capitalizations below AU$305m, we found that the median total CEO compensation was AU$442k. That is to say, Paul Simmons is paid under the industry median. Moreover, Paul Simmons also holds AU$761k worth of MCS Services stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | AU$196k | AU$200k | 78% |

| Other | AU$56k | AU$65k | 22% |

| Total Compensation | AU$252k | AU$265k | 100% |

Speaking on an industry level, nearly 70% of total compensation represents salary, while the remainder of 30% is other remuneration. MCS Services pays out 78% of remuneration in the form of a salary, significantly higher than the industry average. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

A Look at MCS Services Limited's Growth Numbers

MCS Services Limited has reduced its earnings per share by 71% a year over the last three years. In the last year, its revenue is down 12%.

The decline in EPS is a bit concerning. This is compounded by the fact revenue is actually down on last year. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has MCS Services Limited Been A Good Investment?

The return of -38% over three years would not have pleased MCS Services Limited shareholders. Therefore, it might be upsetting for shareholders if the CEO were paid generously.

In Summary...

Given that shareholders haven't seen any positive returns on their investment, not to mention the lack of earnings growth, this may suggest that few of them would be willing to award the CEO with a pay rise. At the upcoming AGM, the board will get the chance to explain the steps it plans to take to improve business performance.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. We did our research and spotted 2 warning signs for MCS Services that investors should look into moving forward.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:MSG

Flawless balance sheet slight.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.6% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.4% undervalued

TO

Community Contributor