- Australia

- /

- Commercial Services

- /

- ASX:MSG

This Is The Reason Why We Think MCS Services Limited's (ASX:MSG) CEO Deserves A Bump Up To Their Compensation

The impressive results at MCS Services Limited (ASX:MSG) recently will be great news for shareholders. At the upcoming AGM on 30 November 2022, they would be interested to hear about the company strategy going forward and get a chance to cast their votes on resolutions such as executive remuneration and other company matters. We think the CEO has done a pretty decent job and probably deserves a well-earned pay rise.

Our analysis indicates that MSG is potentially undervalued!

Comparing MCS Services Limited's CEO Compensation With The Industry

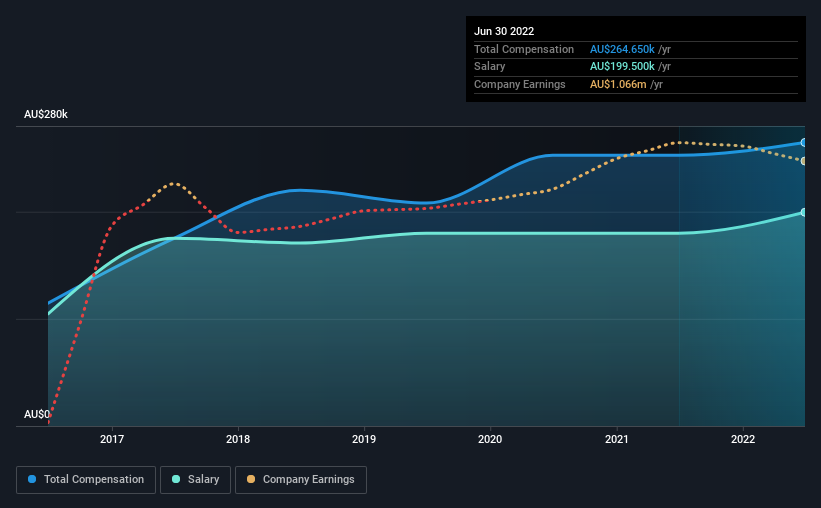

According to our data, MCS Services Limited has a market capitalization of AU$7.9m, and paid its CEO total annual compensation worth AU$265k over the year to June 2022. That's just a smallish increase of 4.8% on last year. Notably, the salary which is AU$199.5k, represents most of the total compensation being paid.

For comparison, other companies in the industry with market capitalizations below AU$302m, reported a median total CEO compensation of AU$443k. Accordingly, MCS Services pays its CEO under the industry median. What's more, Paul Simmons holds AU$1.5m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2022 | 2021 | Proportion (2022) |

| Salary | AU$200k | AU$180k | 75% |

| Other | AU$65k | AU$73k | 25% |

| Total Compensation | AU$265k | AU$253k | 100% |

On an industry level, around 60% of total compensation represents salary and 40% is other remuneration. It's interesting to note that MCS Services pays out a greater portion of remuneration through salary, compared to the industry. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

MCS Services Limited's Growth

MCS Services Limited's earnings per share (EPS) grew 72% per year over the last three years. In the last year, its revenue is up 15%.

This demonstrates that the company has been improving recently and is good news for the shareholders. It's a real positive to see this sort of revenue growth in a single year. That suggests a healthy and growing business. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has MCS Services Limited Been A Good Investment?

We think that the total shareholder return of 135%, over three years, would leave most MCS Services Limited shareholders smiling. So they may not be at all concerned if the CEO were to be paid more than is normal for companies around the same size.

To Conclude...

Seeing that the company has put in a relatively good performance, the CEO remuneration policy may not be the focus at the AGM. However, investors will get the chance to engage on key strategic initiatives and future growth opportunities for the company and set their longer-term expectations.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. That's why we did our research, and identified 3 warning signs for MCS Services (of which 1 shouldn't be ignored!) that you should know about in order to have a holistic understanding of the stock.

Switching gears from MCS Services, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

If you're looking to trade MCS Services, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:MSG

Flawless balance sheet slight.

Market Insights

Community Narratives