Advertisement

- Australia

- /

- Professional Services

- /

- ASX:KPG

We Think Kelly Partners Group Holdings (ASX:KPG) Can Stay On Top Of Its Debt

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Kelly Partners Group Holdings Limited (ASX:KPG) does carry debt. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Kelly Partners Group Holdings

How Much Debt Does Kelly Partners Group Holdings Carry?

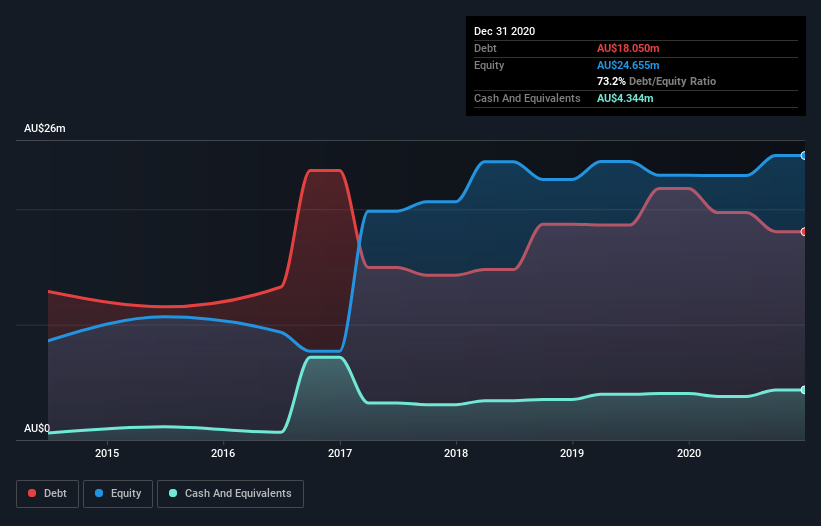

As you can see below, Kelly Partners Group Holdings had AU$18.1m of debt at December 2020, down from AU$21.8m a year prior. However, it does have AU$4.34m in cash offsetting this, leading to net debt of about AU$13.7m.

How Healthy Is Kelly Partners Group Holdings' Balance Sheet?

We can see from the most recent balance sheet that Kelly Partners Group Holdings had liabilities of AU$19.0m falling due within a year, and liabilities of AU$17.5m due beyond that. Offsetting these obligations, it had cash of AU$4.34m as well as receivables valued at AU$9.71m due within 12 months. So it has liabilities totalling AU$22.4m more than its cash and near-term receivables, combined.

While this might seem like a lot, it is not so bad since Kelly Partners Group Holdings has a market capitalization of AU$112.1m, and so it could probably strengthen its balance sheet by raising capital if it needed to. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Kelly Partners Group Holdings has net debt of just 0.91 times EBITDA, indicating that it is certainly not a reckless borrower. And it boasts interest cover of 9.0 times, which is more than adequate. Also good is that Kelly Partners Group Holdings grew its EBIT at 14% over the last year, further increasing its ability to manage debt. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Kelly Partners Group Holdings's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last three years, Kelly Partners Group Holdings recorded free cash flow worth a fulsome 84% of its EBIT, which is stronger than we'd usually expect. That puts it in a very strong position to pay down debt.

Our View

Kelly Partners Group Holdings's conversion of EBIT to free cash flow suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14's goalkeeper. And that's just the beginning of the good news since its interest cover is also very heartening. Looking at the bigger picture, we think Kelly Partners Group Holdings's use of debt seems quite reasonable and we're not concerned about it. After all, sensible leverage can boost returns on equity. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For example - Kelly Partners Group Holdings has 4 warning signs we think you should be aware of.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

When trading Kelly Partners Group Holdings or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Kelly Partners Group Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:KPG

Kelly Partners Group Holdings

Provides chartered accounting and other professional services to private businesses and high net worth individuals in Australia and internationally.

Solid track record low.

Market Insights

Advertisement

Community Narratives

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|5.7% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|32.5% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$384.84|21.9% undervalued

BL

Community Contributor