Advertisement

- Australia

- /

- Professional Services

- /

- ASX:KPG

Kelly Partners Group Holdings' (ASX:KPG) Dividend Will Be AU$0.0036

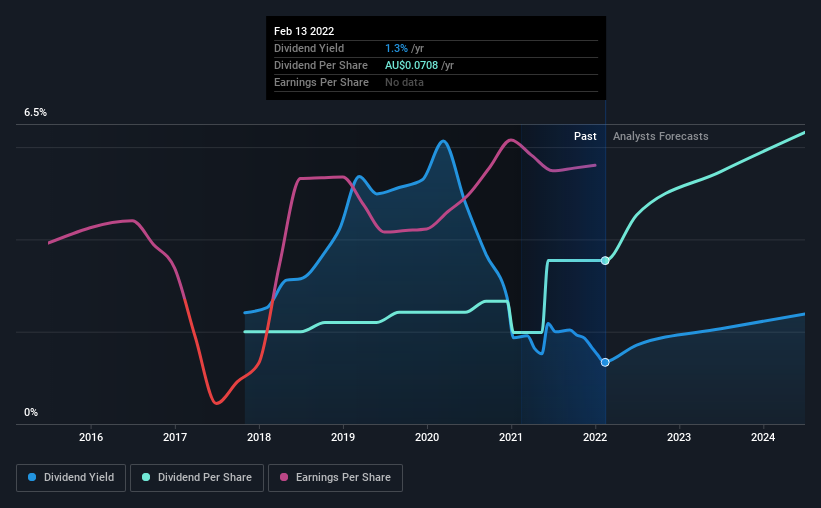

The board of Kelly Partners Group Holdings Limited (ASX:KPG) has announced that it will pay a dividend on the 28th of February, with investors receiving AU$0.0036 per share. Including this payment, the dividend yield on the stock will be 1.3%, which is a modest boost for shareholders' returns.

While the dividend yield is important for income investors, it is also important to consider any large share price moves, as this will generally outweigh any gains from distributions. Investors will be pleased to see that Kelly Partners Group Holdings' stock price has increased by 36% in the last 3 months, which is good for shareholders and can also explain a decrease in the dividend yield.

See our latest analysis for Kelly Partners Group Holdings

Kelly Partners Group Holdings' Earnings Easily Cover the Distributions

It would be nice for the yield to be higher, but we should also check if higher levels of dividend payment would be sustainable. The last dividend was quite easily covered by Kelly Partners Group Holdings' earnings. This indicates that a lot of the earnings are being reinvested into the business, with the aim of fueling growth.

Over the next year, EPS is forecast to fall by 35.1%. If recent patterns in the dividend continue, we could see the payout ratio reaching 86% in the next 12 months, which is on the higher end of the range we would say is sustainable.

Kelly Partners Group Holdings Doesn't Have A Long Payment History

The company has maintained a consistent dividend for a few years now, but we would like to see a longer track record before relying on it. The first annual payment during the last 4 years was AU$0.04 in 2018, and the most recent fiscal year payment was AU$0.071. This means that it has been growing its distributions at 15% per annum over that time. Kelly Partners Group Holdings has been growing its dividend quite rapidly, which is exciting. However, the short payment history makes us question whether this performance will persist across a full market cycle.

The Dividend Looks Likely To Grow

Investors could be attracted to the stock based on the quality of its payment history. It's encouraging to see Kelly Partners Group Holdings has been growing its earnings per share at 34% a year over the past five years. The company doesn't have any problems growing, despite returning a lot of capital to shareholders, which is a very nice combination for a dividend stock to have.

We Really Like Kelly Partners Group Holdings' Dividend

Overall, we like to see the dividend staying consistent, and we think Kelly Partners Group Holdings might even raise payments in the future. The earnings easily cover the company's distributions, and the company is generating plenty of cash. We should point out that the earnings are expected to fall over the next 12 months, which won't be a problem if this doesn't become a trend, but could cause some turbulence in the next year. Taking this all into consideration, this looks like it could be a good dividend opportunity.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. However, there are other things to consider for investors when analysing stock performance. For instance, we've picked out 2 warning signs for Kelly Partners Group Holdings that investors should take into consideration. If you are a dividend investor, you might also want to look at our curated list of high performing dividend stock.

Valuation is complex, but we're here to simplify it.

Discover if Kelly Partners Group Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:KPG

Kelly Partners Group Holdings

Provides chartered accounting and other professional services to private businesses and high net worth individuals in Australia and internationally.

Slightly overvalued with questionable track record.

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor