Advertisement

- Australia

- /

- Industrials

- /

- ASX:SST

Undiscovered Gems in Australia to Explore This January 2025

Simply Wall St

Reviewed by Simply Wall St

As the Australian market experiences positive investor sentiment, with the ASX200 reaching record highs amid easing tariff concerns, certain sectors like IT, Materials, and Real Estate are outperforming while others such as Utilities lag behind. In this dynamic environment, identifying undiscovered gems involves finding stocks that can capitalize on sector strengths and navigate broader economic shifts effectively.

Top 10 Undiscovered Gems With Strong Fundamentals In Australia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Fiducian Group | NA | 9.94% | 6.48% | ★★★★★★ |

| Schaffer | 24.98% | 2.97% | -6.23% | ★★★★★★ |

| Sugar Terminals | NA | 3.14% | 3.53% | ★★★★★★ |

| Bailador Technology Investments | NA | 11.17% | 10.16% | ★★★★★★ |

| Lycopodium | NA | 17.22% | 33.85% | ★★★★★★ |

| Djerriwarrh Investments | 1.14% | 8.17% | 7.54% | ★★★★★★ |

| Red Hill Minerals | NA | 75.05% | 36.74% | ★★★★★★ |

| Steamships Trading | 33.60% | 4.17% | 3.90% | ★★★★★☆ |

| K&S | 16.07% | 0.09% | 33.40% | ★★★★☆☆ |

| Hearts and Minds Investments | 1.00% | 18.81% | 20.95% | ★★★★☆☆ |

Below we spotlight a couple of our favorites from our exclusive screener.

EQT Holdings (ASX:EQT)

Simply Wall St Value Rating: ★★★★★☆

Overview: EQT Holdings Limited, along with its subsidiaries, offers philanthropic, trustee executor, and investment services in Australia and has a market capitalization of approximately A$901 million.

Operations: EQT Holdings generates revenue primarily from its Corporate & Superannuation Trustee Services, which contributed A$71.51 million, and Trustee & Wealth Services (excluding Superannuation Trustee Services), which added A$99.08 million.

EQT Holdings, a smaller player in the financial sector, presents an intriguing profile. Its debt to equity ratio has risen from 4.6% to 18.3% over five years, yet interest payments are comfortably covered with EBIT at 9.6 times interest repayments. Despite earnings growing at a modest 1.2% annually over the past five years, they lag behind industry growth of 17.7%. However, future prospects look brighter with earnings forecasted to grow by 22.7% per year and positive free cash flow supporting its operations without concern for cash runway issues—an encouraging sign for potential investors eyeing this financial entity's trajectory in A$.

- Get an in-depth perspective on EQT Holdings' performance by reading our health report here.

Gain insights into EQT Holdings' historical performance by reviewing our past performance report.

Mader Group (ASX:MAD)

Simply Wall St Value Rating: ★★★★★★

Overview: Mader Group Limited is a contracting company that offers specialist technical services in the mining, energy, and industrial sectors both in Australia and internationally, with a market cap of A$1.25 billion.

Operations: Mader Group generates revenue primarily from its Staffing & Outsourcing Services, amounting to A$774.47 million. The company's market cap is approximately A$1.25 billion.

Mader Group, a nimble player in the Australian market, showcases impressive financial health with high-quality earnings and a net debt to equity ratio of 19.4%, which is satisfactory. Over the past five years, its debt to equity ratio has notably decreased from 70.9% to 38.2%. In terms of growth, Mader's earnings surged by 30.9% last year, outpacing the industry average of 9.1%. The company appears undervalued as it trades at nearly half its estimated fair value and enjoys robust cash flow positivity with EBIT covering interest payments by nearly twenty times.

- Dive into the specifics of Mader Group here with our thorough health report.

Assess Mader Group's past performance with our detailed historical performance reports.

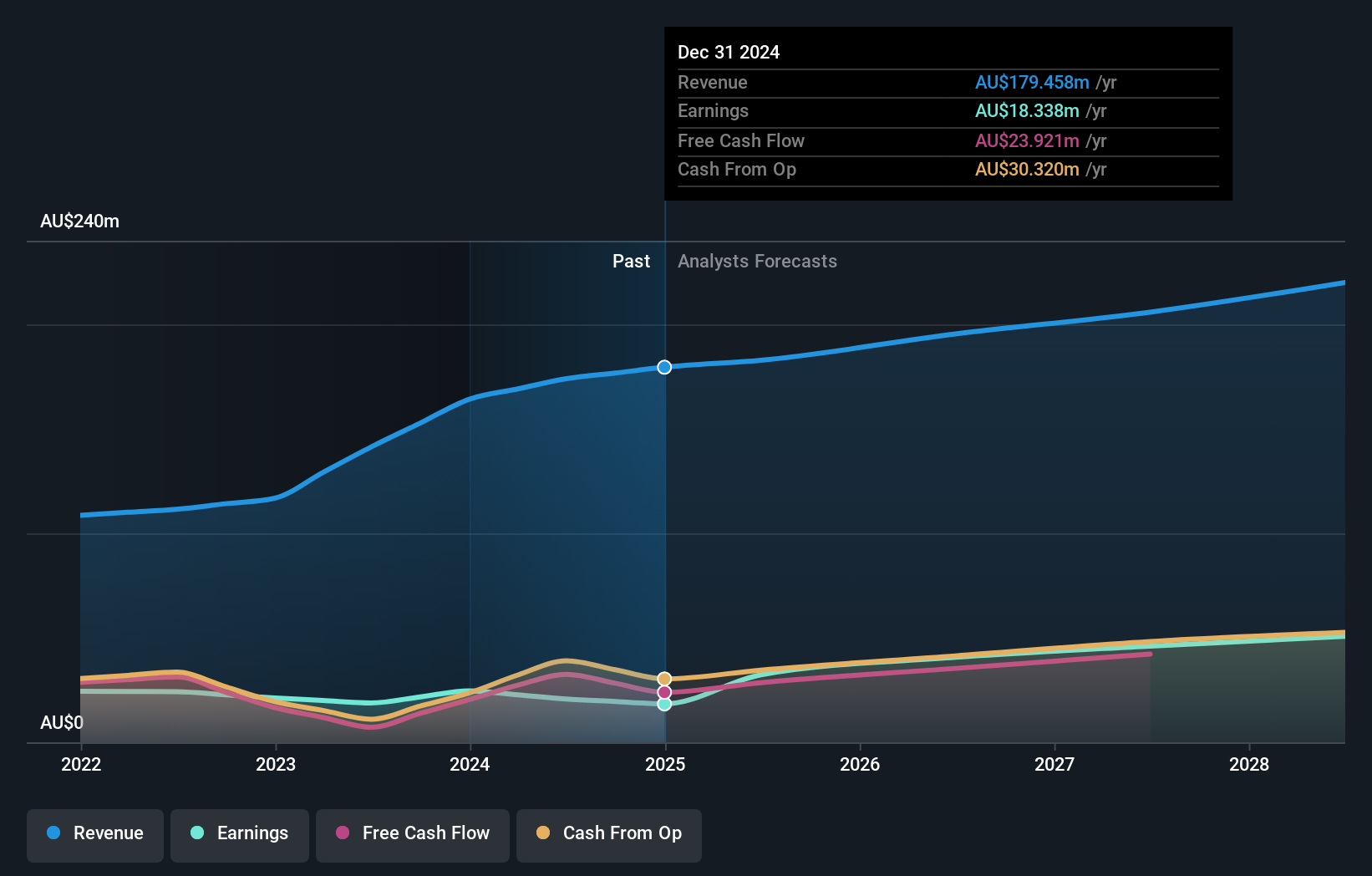

Steamships Trading (ASX:SST)

Simply Wall St Value Rating: ★★★★★☆

Overview: Steamships Trading Company Limited operates in the shipping, transport, property, and hospitality sectors in Papua New Guinea with a market capitalization of A$431.01 million.

Operations: Steamships Trading generates revenue primarily from its Logistics segment, contributing PGK 404.68 million, and its Property and Hospitality segment, which adds PGK 313.16 million. The Finance, Investment and Eliminations segment shows a negative impact of PGK -7.20 million on the overall revenue.

Steamships Trading, a small player in the Industrials sector, has shown impressive earnings growth of 38.2% over the past year, outpacing the industry average of 8.5%. Despite a large one-off gain impacting recent financial results by PGK17.7M, its profitability ensures that cash runway isn't an issue. The company's debt situation has improved with a debt to equity ratio decreasing from 39.8% to 33.6% in five years and interest payments are well-covered at 19.5x EBIT coverage. With a price-to-earnings ratio of 18.1x below the market average, Steamships seems attractively valued for potential investors.

- Take a closer look at Steamships Trading's potential here in our health report.

Examine Steamships Trading's past performance report to understand how it has performed in the past.

Taking Advantage

- Delve into our full catalog of 49 ASX Undiscovered Gems With Strong Fundamentals here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:SST

Steamships Trading

Engages in the shipping, transport, property, and hospitality operation businesses in Papua New Guinea.

Adequate balance sheet low.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.6% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|30.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor