Advertisement

The Trend Of High Returns At Embelton (ASX:EMB) Has Us Very Interested

If you're not sure where to start when looking for the next multi-bagger, there are a few key trends you should keep an eye out for. Typically, we'll want to notice a trend of growing return on capital employed (ROCE) and alongside that, an expanding base of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. So when we looked at the ROCE trend of Embelton (ASX:EMB) we really liked what we saw.

Understanding Return On Capital Employed (ROCE)

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. The formula for this calculation on Embelton is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.20 = AU$3.9m ÷ (AU$36m - AU$17m) (Based on the trailing twelve months to June 2020).

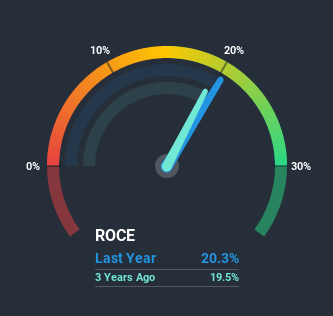

Thus, Embelton has an ROCE of 20%. That's a fantastic return and not only that, it outpaces the average of 9.6% earned by companies in a similar industry.

See our latest analysis for Embelton

Historical performance is a great place to start when researching a stock so above you can see the gauge for Embelton's ROCE against it's prior returns. If you're interested in investigating Embelton's past further, check out this free graph of past earnings, revenue and cash flow.

What The Trend Of ROCE Can Tell Us

We like the trends that we're seeing from Embelton. Over the last five years, returns on capital employed have risen substantially to 20%. Basically the business is earning more per dollar of capital invested and in addition to that, 48% more capital is being employed now too. So we're very much inspired by what we're seeing at Embelton thanks to its ability to profitably reinvest capital.

For the record though, there was a noticeable increase in the company's current liabilities over the period, so we would attribute some of the ROCE growth to that. The current liabilities has increased to 47% of total assets, so the business is now more funded by the likes of its suppliers or short-term creditors. And with current liabilities at those levels, that's pretty high.The Bottom Line On Embelton's ROCE

All in all, it's terrific to see that Embelton is reaping the rewards from prior investments and is growing its capital base. And with a respectable 87% awarded to those who held the stock over the last five years, you could argue that these developments are starting to get the attention they deserve. So given the stock has proven it has promising trends, it's worth researching the company further to see if these trends are likely to persist.

Embelton does come with some risks though, we found 3 warning signs in our investment analysis, and 1 of those is significant...

If you'd like to see other companies earning high returns, check out our free list of companies earning high returns with solid balance sheets here.

If you decide to trade Embelton, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Embelton might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About ASX:EMB

Embelton

Engages in the manufacture, distribution, and installation of flooring products and services in Australia, Singapore, China, the United Kingdom, and internationally.

Flawless balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|8.8% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.3% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$384.84|18.1% undervalued

BL

Community Contributor