Advertisement

In the midst of recent market volatility and economic uncertainties, small-cap stocks have been particularly impacted, as evidenced by the S&P 600's performance. Despite these challenges, certain undiscovered gems within this category exhibit strong potential due to their robust fundamentals and growth prospects. Identifying promising stocks in such a dynamic environment requires a keen eye for companies with solid financial health, innovative business models, and the ability to adapt to changing market conditions. Here are three small-cap stocks that stand out as potential opportunities amidst today's fluctuating market landscape.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Payton Industries | NA | 8.94% | 12.12% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Polyram Plastic Industries | 34.64% | 9.13% | 13.03% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Societe de Limonaderies et de Boissons Rafraichissantes d'Afrique | 39.37% | 8.04% | -3.72% | ★★★★★☆ |

| Strauss Group | 74.59% | 3.72% | -12.93% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Isracard | 73.43% | 7.99% | -2.01% | ★★★★☆☆ |

| Wilson | 64.79% | 30.09% | 68.29% | ★★★★☆☆ |

Here's a peek at a few of the choices from the screener.

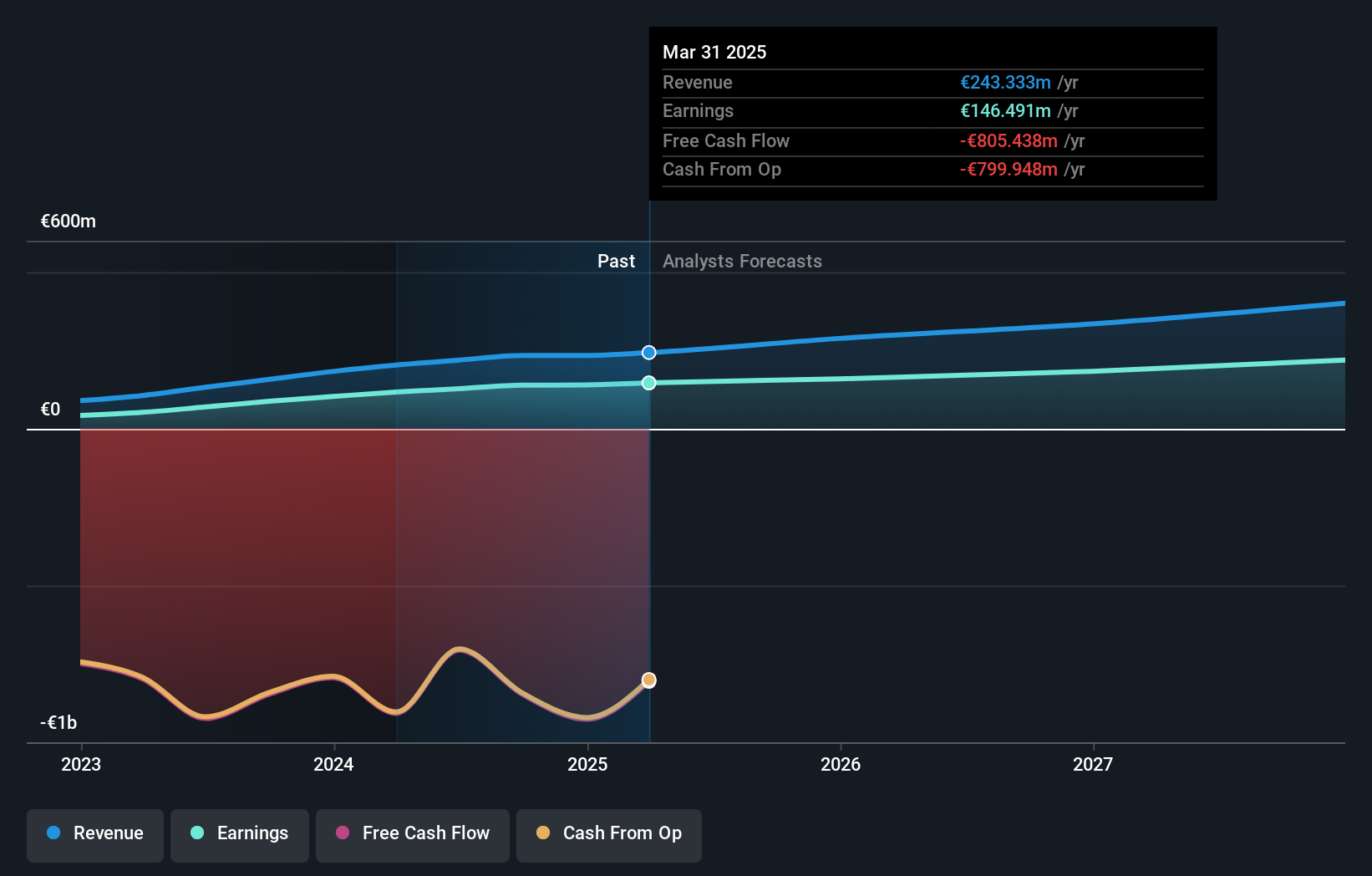

Optima bank (ATSE:OPTIMA)

Simply Wall St Value Rating: ★★★★★☆

Overview: Optima Bank S.A. offers banking, brokerage, and investment banking services in Greece with a market cap of €894.14 million.

Operations: Optima Bank S.A. generates revenue through its banking, brokerage, and investment banking services in Greece. The company has a market cap of €894.14 million.

Optima bank, with total assets of €4.5 billion and equity of €548 million, has seen impressive growth. Total deposits stand at €3.7 billion, while loans amount to €3 billion. The bank's earnings surged by 83% last year, outpacing the industry average of 56%. It trades at 37% below its estimated fair value and boasts a low bad loans allowance at 1%. Recent earnings reports show net income for Q2 was €36 million compared to last year's €26 million.

- Unlock comprehensive insights into our analysis of Optima bank stock in this health report.

Evaluate Optima bank's historical performance by accessing our past performance report.

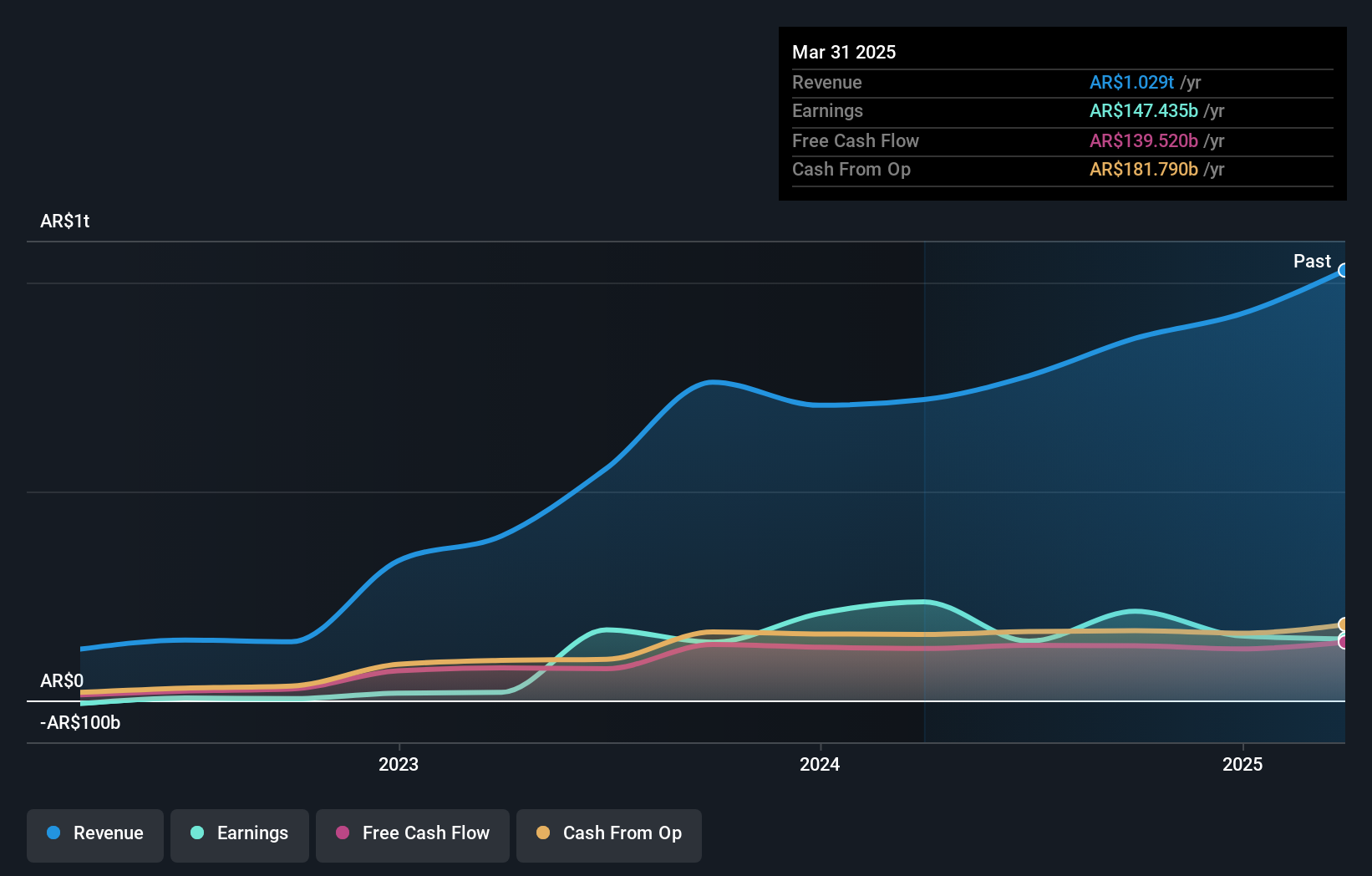

MetroGAS (BASE:METR)

Simply Wall St Value Rating: ★★★★☆☆

Overview: MetroGAS S.A. is a company that focuses on the distribution of natural gas primarily in Argentina with a market cap of ARS542.42 billion.

Operations: MetroGAS generates revenue primarily from its distribution segment, which contributed ARS185.55 billion, and its marketing segment, which added ARS143.44 billion.

MetroGAS, a relatively small player in the gas utilities sector, has shown impressive earnings growth of 489.2% over the past year, far outpacing the industry average of 22.4%. The company’s debt-to-equity ratio improved significantly from 70.1% to 8.9% in five years, indicating better financial health. Despite its high level of non-cash earnings and a low P/E ratio of 5.2x compared to the AR market's 18.8x, MetroGAS's interest payments on its debt are not well covered by EBIT at just 0.1x coverage.

- Take a closer look at MetroGAS' potential here in our health report.

Explore historical data to track MetroGAS' performance over time in our Past section.

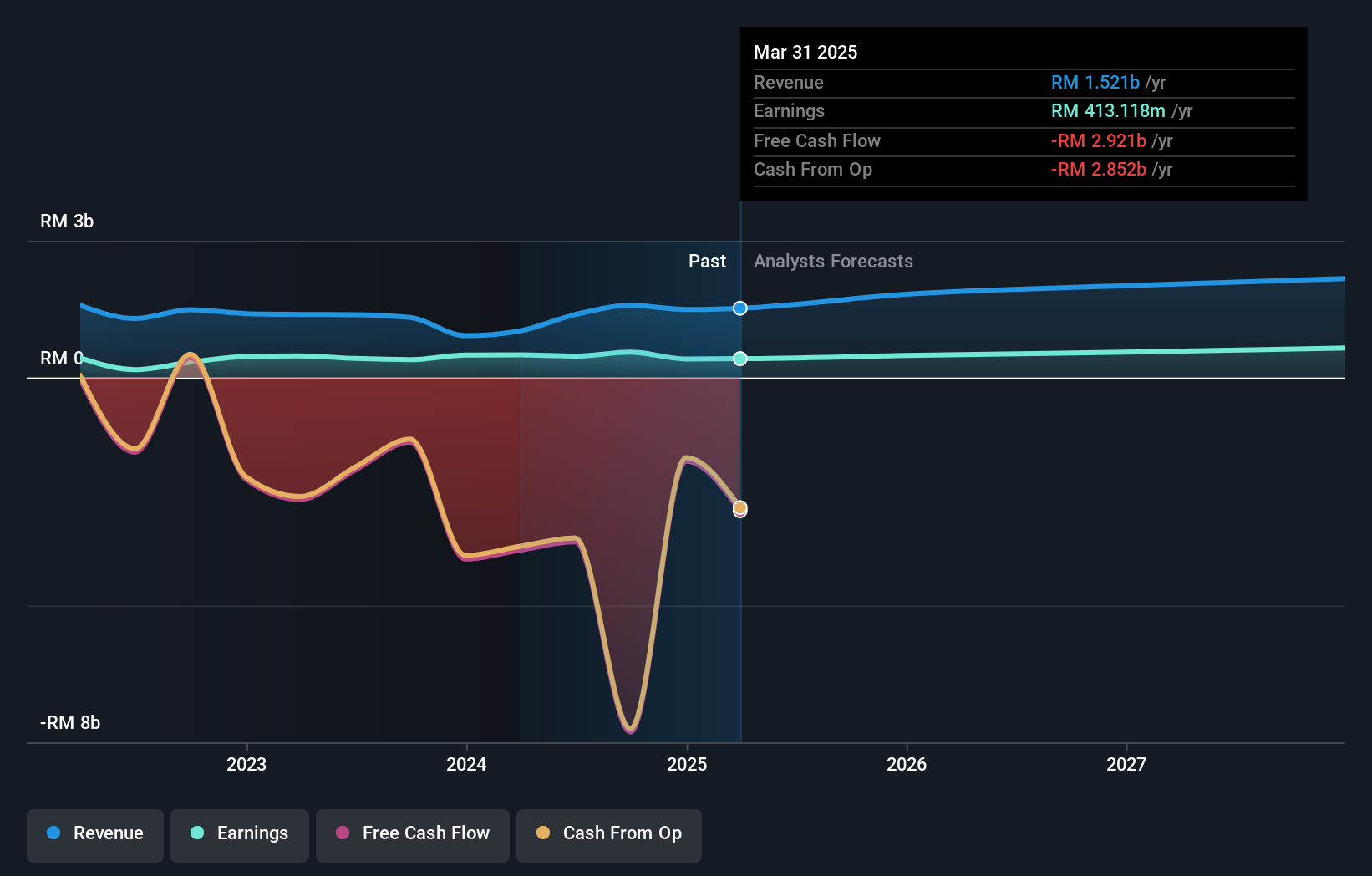

MBSB Berhad (KLSE:MBSB)

Simply Wall St Value Rating: ★★★★☆☆

Overview: MBSB Berhad, an investment holding company with a market cap of MYR6.50 billion, provides banking services in Malaysia.

Operations: MBSB Berhad generates revenue primarily from Consumer Banking (MYR963.55 million) and Corporate Banking (MYR515.97 million). The company also has a Segment Adjustment of MYR152.27 million.

MBSB Berhad, with MYR65.6B in total assets and MYR9.9B in equity, has a solid foundation supported by MYR47.9B in deposits and MYR41.4B in loans. The company’s liabilities are primarily funded by customer deposits (86%), which is less risky than external borrowing. Despite a high level of bad loans at 7.1%, MBSB has kept its allowance for bad loans low at 52%. Recently, the company announced a name change effective June 11, 2024, reflecting its evolving identity and strategic direction.

- Click here and access our complete health analysis report to understand the dynamics of MBSB Berhad.

Review our historical performance report to gain insights into MBSB Berhad's's past performance.

Taking Advantage

- Click this link to deep-dive into the 4834 companies within our Undiscovered Gems With Strong Fundamentals screener.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KLSE:MBSB

MBSB Berhad

An investment holding company, provides banking services in Malaysia.

Adequate balance sheet with moderate growth potential.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor