As global markets rebound from recent sell-offs and central banks adjust their monetary policies, the S&P 600 and other small-cap indices have shown resilience, reflecting cautious optimism among investors. With core inflation slightly higher than expected but overall economic indicators offering glimmers of hope, it's an opportune time to explore stocks that may be undervalued yet poised for growth. In this dynamic environment, a good stock often combines strong fundamentals with the ability to navigate market volatility effectively. Here are three undiscovered gems that could offer potential as we head into September 2024.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Canal Shipping Agencies | NA | 2.25% | 10.54% | ★★★★★★ |

| Etihad Atheeb Telecommunication | NA | 26.82% | 62.18% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Standard Bank | 0.13% | 27.78% | 30.36% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Central Cooperative Bank AD | 4.88% | 4.12% | 8.95% | ★★★★☆☆ |

| Wilson | 64.79% | 30.09% | 68.29% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Vakif Gayrimenkul Yatirim Ortakligi | 0.74% | 63.98% | 57.67% | ★★★★☆☆ |

We're going to check out a few of the best picks from our screener tool.

Molinos Rio de la Plata (BASE:MOLI)

Simply Wall St Value Rating: ★★★★★★

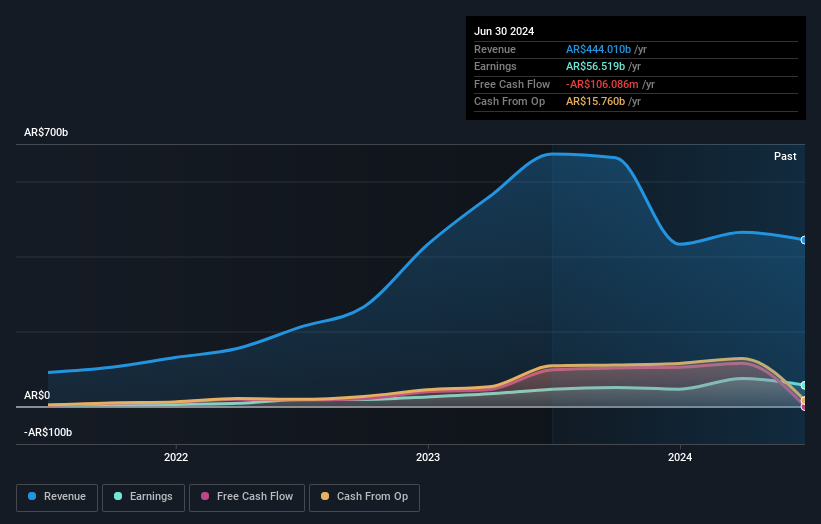

Overview: Molinos Rio de la Plata S.A. is a food company based in Argentina with a market cap of ARS719.96 billion.

Operations: Molinos Rio de la Plata S.A. generates revenue primarily from its Food segment (ARS422.56 billion) and Wineries segment (ARS21.45 billion).

Molinos Rio de la Plata's earnings surged 22.1% last year, outpacing the Food industry’s 4.5%. The net debt to equity ratio stands at a satisfactory 6.8%, down from 101.1% five years ago, reflecting prudent financial management. With a price-to-earnings ratio of 12.7x, it offers good value compared to the AR market average of 20x. Interest payments are well covered by EBIT at five times coverage, underscoring robust operational efficiency despite recent share price volatility.

- Dive into the specifics of Molinos Rio de la Plata here with our thorough health report.

Gain insights into Molinos Rio de la Plata's past trends and performance with our Past report.

Çelebi Hava Servisi (IBSE:CLEBI)

Simply Wall St Value Rating: ★★★★★★

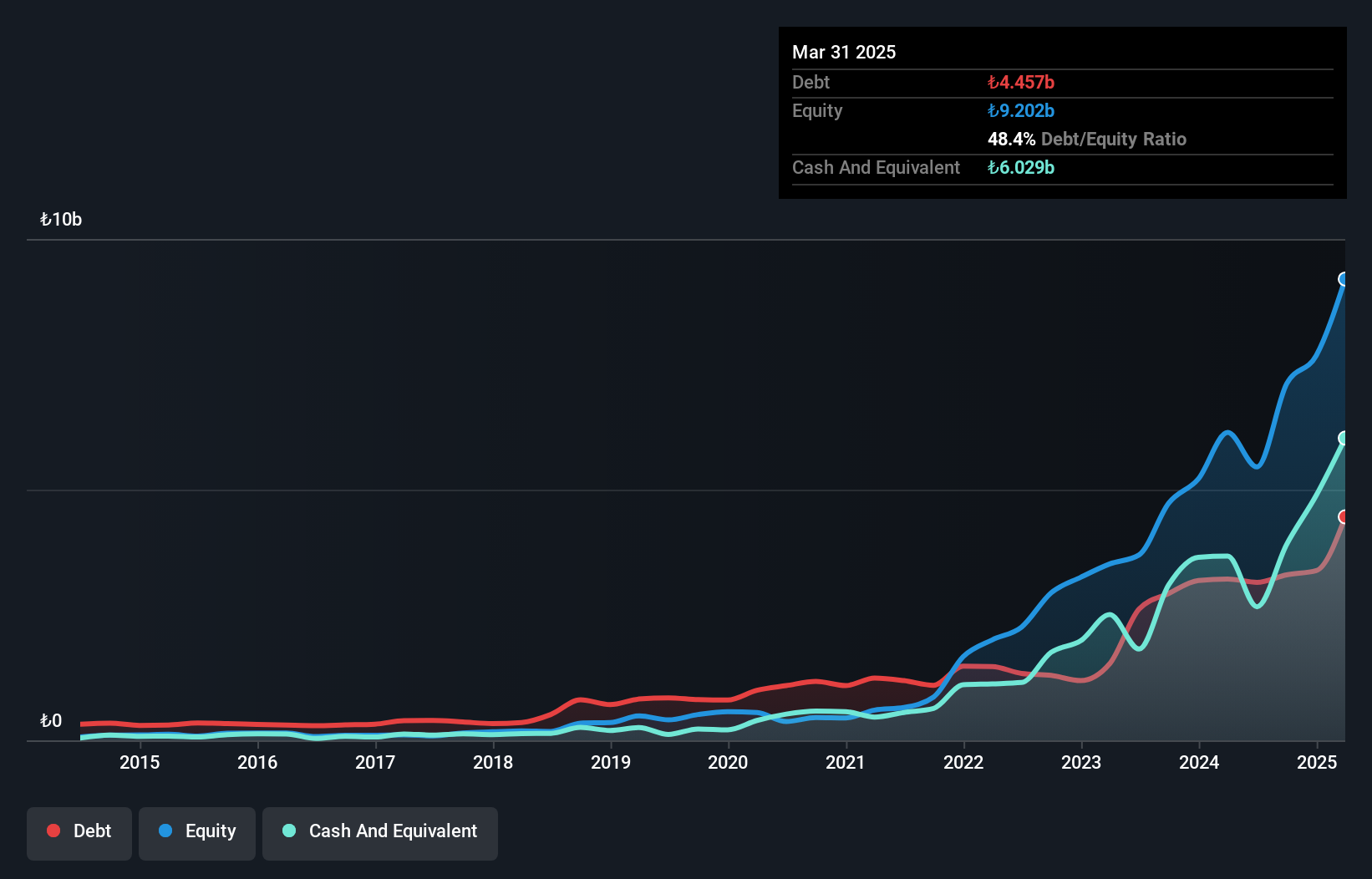

Overview: Çelebi Hava Servisi A.S. provides ground handling, cargo, and warehouse services to domestic and foreign airlines, and private air cargo companies primarily in Turkey with a market cap of TRY46.27 billion.

Operations: The company's primary revenue streams include Airport Ground Services, generating TRY9.82 billion, and Cargo and Warehouse Services, contributing TRY5.18 billion.

Çelebi Hava Servisi has shown impressive financial performance, with net income for the second quarter of 2024 reaching TRY 609.42 million, up from TRY 474.91 million a year ago. The company's net debt to equity ratio stands at a satisfactory 8.9%, and its earnings growth over the past year (70.5%) significantly outpaces the industry average of 9.8%. Additionally, Çelebi's interest payments are well covered by EBIT at a robust 27.8x coverage ratio, reflecting strong financial health and operational efficiency.

Sariguna Primatirta (IDX:CLEO)

Simply Wall St Value Rating: ★★★★★☆

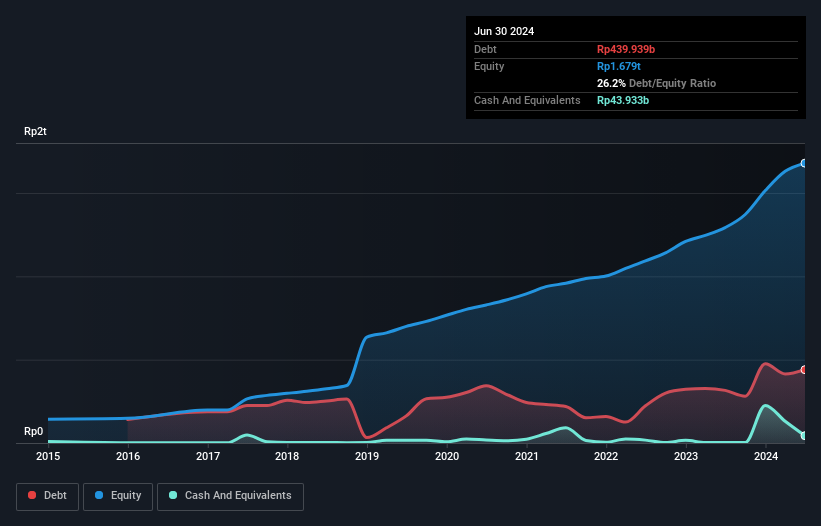

Overview: PT Sariguna Primatirta Tbk operates in the bottled drinking water industry in Indonesia, with a market cap of IDR15.13 billion.

Operations: PT Sariguna Primatirta Tbk generates revenue primarily from bottled drinking water, contributing IDR1.30 trillion, and non-bottle segments, adding IDR1.07 trillion.

Sariguna Primatirta reported impressive half-year sales of IDR 1.30 trillion, up from IDR 975.68 billion last year, with net income rising to IDR 220.23 million from IDR 128.81 million. EBIT covers interest payments by a robust 25.7 times, indicating solid financial health. The company's debt to equity ratio increased slightly over five years from 23% to 26%. Trading at a discount of around 5%, it shows potential for value investors looking for growth in the beverage sector.

Summing It All Up

- Delve into our full catalog of 4852 Undiscovered Gems With Strong Fundamentals here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About IDX:CLEO

Sariguna Primatirta

Engages in the bottled drinking water business in Indonesia.

Exceptional growth potential with solid track record.