- United States

- /

- Software

- /

- NasdaqGS:ZM

Zoom Communications (NasdaqGS:ZM) Unveils AI-Powered Zoom Virtual Agent 2.0 And Expands Zoom Phone In India

Reviewed by Simply Wall St

Zoom Communications (NasdaqGS:ZM) has recently made strategic moves to strengthen its market position, highlighted by the launch of the Zoom Virtual Agent 2.0 and the expansion of its Zoom Phone service in India. These innovations align with broader trends in customer service automation and telephony enhancements. Despite the company's share price moving 5% over the last quarter, this movement is consistent with broader market trends, which saw the S&P 500 and Nasdaq rise amid optimistic trade negotiations and strong economic data. Zoom's first-quarter earnings showing improved profits and ongoing share buyback program may have added weight to such market increases.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

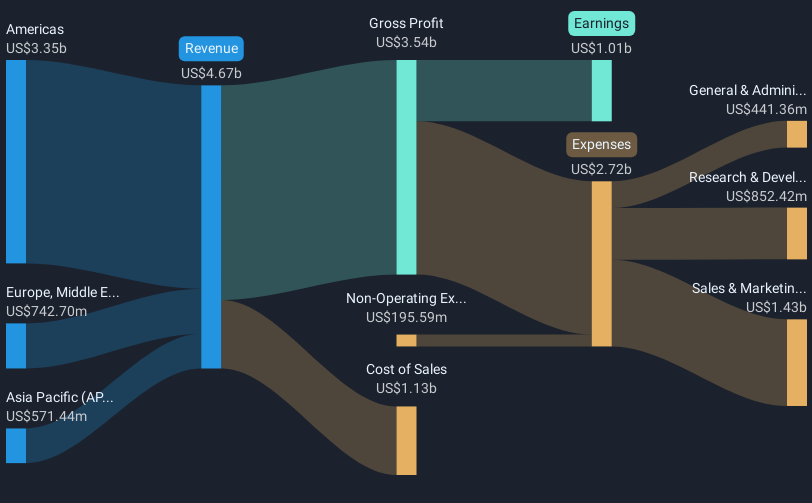

The recent launches by Zoom Communications, such as the Zoom Virtual Agent 2.0 and the expansion of Zoom Phone in India, could potentially enhance its brand value and customer base. These moves are aimed at capitalizing on the trends in customer service automation and telephony advancements, aligning with their AI-first strategy. Over the past year, Zoom’s total return, including share price and dividends, was 34.90%. This impressive return signifies robust performance compared to the US Market's 11.2% return and the 18.5% return of the US Software industry over the same period, reflecting well on Zoom's capacity to innovate and adapt to industry trends.

Zoom’s share price currently stands at US$78.05, presenting an 11.8% potential increase compared to the analyst consensus price target of US$88.48. If Zoom successfully leverages its AI initiatives, we could see a positive impact on revenue and earnings forecasts. However, challenges such as increased competition and macroeconomic conditions still pose risks to achieving these growth targets. Earnings and revenue forecasts reflect a moderate growth trajectory, emphasizing the importance of ongoing customer adoption and execution of strategic partnerships. The company’s forward-thinking initiatives and robust performance can bolster confidence among investors, despite broader challenges in the market.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Zoom Communications might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:ZM

Zoom Communications

Provides an Artificial Intelligence-first work platform for human connection in the Americas, the Asia Pacific, Europe, the Middle East, and Africa.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion