Advertisement

- United States

- /

- Commercial Services

- /

- NasdaqGS:VSEC

You Have To Love VSE Corporation's (NASDAQ:VSEC) Dividend

Today we'll take a closer look at VSE Corporation (NASDAQ:VSEC) from a dividend investor's perspective. Owning a strong business and reinvesting the dividends is widely seen as an attractive way of growing your wealth. On the other hand, investors have been known to buy a stock because of its yield, and then lose money if the company's dividend doesn't live up to expectations.

A 1.4% yield is nothing to get excited about, but investors probably think the long payment history suggests VSE has some staying power. Some simple analysis can reduce the risk of holding VSE for its dividend, and we'll focus on the most important aspects below.

Explore this interactive chart for our latest analysis on VSE!

Payout ratios

Companies (usually) pay dividends out of their earnings. If a company is paying more than it earns, the dividend might have to be cut. As a result, we should always investigate whether a company can afford its dividend, measured as a percentage of a company's net income after tax. VSE paid out 12% of its profit as dividends, over the trailing twelve month period. We'd say its dividends are thoroughly covered by earnings.

In addition to comparing dividends against profits, we should inspect whether the company generated enough cash to pay its dividend. VSE's cash payout ratio in the last year was 28%, which suggests dividends were well covered by cash generated by the business. It's positive to see that VSE's dividend is covered by both profits and cash flow, since this is generally a sign that the dividend is sustainable, and a lower payout ratio usually suggests a greater margin of safety before the dividend gets cut.

Is VSE's Balance Sheet Risky?

As VSE has a meaningful amount of debt, we need to check its balance sheet to see if the company might have debt risks. A quick check of its financial situation can be done with two ratios: net debt divided by EBITDA (earnings before interest, tax, depreciation and amortisation), and net interest cover. Net debt to EBITDA measures total debt load relative to company earnings (lower = less debt), while net interest cover measures the ability to pay interest on the debt (higher = greater ability to pay interest costs). VSE has net debt of 2.99 times its EBITDA. Using debt can accelerate business growth, but also increases the risks.

We calculated its interest cover by measuring its earnings before interest and tax (EBIT), and dividing this by the company's net interest expense. With EBIT of 4.59 times its interest expense, VSE's interest cover is starting to look a bit thin.

Consider getting our latest analysis on VSE's financial position here.

Dividend Volatility

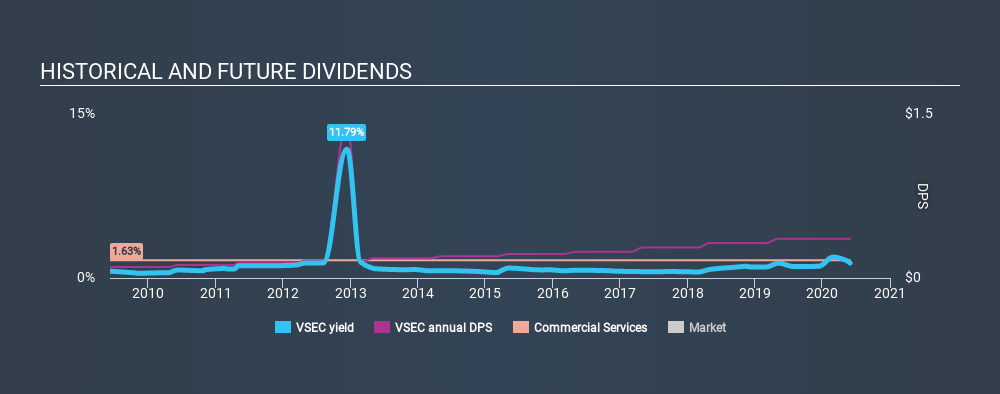

From the perspective of an income investor who wants to earn dividends for many years, there is not much point buying a stock if its dividend is regularly cut or is not reliable. For the purpose of this article, we only scrutinise the last decade of VSE's dividend payments. The dividend has been cut on at least one occasion historically. During the past ten-year period, the first annual payment was US$0.10 in 2010, compared to US$0.36 last year. Dividends per share have grown at approximately 14% per year over this time. The dividends haven't grown at precisely 14% every year, but this is a useful way to average out the historical rate of growth.

VSE has grown distributions at a rapid rate despite cutting the dividend at least once in the past. Companies that cut once often cut again, but it might be worth considering if the business has turned a corner.

Dividend Growth Potential

With a relatively unstable dividend, it's even more important to evaluate if earnings per share (EPS) are growing - it's not worth taking the risk on a dividend getting cut, unless you might be rewarded with larger dividends in future. VSE has grown its earnings per share at 10.0% per annum over the past five years. With a decent amount of growth and a low payout ratio, we think this bodes well for VSE's prospects of growing its dividend payments in the future.

Conclusion

To summarise, shareholders should always check that VSE's dividends are affordable, that its dividend payments are relatively stable, and that it has decent prospects for growing its earnings and dividend. Firstly, we like that VSE has low and conservative payout ratios. We were also glad to see it growing earnings, but it was concerning to see the dividend has been cut at least once in the past. All things considered, VSE looks like a strong prospect. At the right valuation, it could be something special.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. Case in point: We've spotted 2 warning signs for VSE (of which 1 is potentially serious!) you should know about.

We have also put together a list of global stocks with a market capitalisation above $1bn and yielding more 3%.

Love or hate this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Thank you for reading.

About NasdaqGS:VSEC

VSE

Provides aviation aftermarket parts distribution and maintenance, repair, and overhaul services for air transportation assets for commercial and government markets.

Reasonable growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor