Advertisement

- Norway

- /

- Marine and Shipping

- /

- OB:WILS

Wilson ASA (OB:WILS): What Does Its Beta Value Mean For Your Portfolio?

Anyone researching Wilson ASA (OB:WILS) might want to consider the historical volatility of the share price. Volatility is considered to be a measure of risk in modern finance theory. Investors may think of volatility as falling into two main categories. First, we have company specific volatility, which is the price gyrations of an individual stock. Holding at least 8 stocks can reduce this kind of risk across a portfolio. The second type is the broader market volatility, which you cannot diversify away, since it arises from macroeconomic factors which directly affects all the stocks on the market.

Some stocks mimic the volatility of the market quite closely, while others demonstrate muted, exagerrated or uncorrelated price movements. Beta is a widely used metric to measure a stock's exposure to market risk (volatility). Before we go on, it's worth noting that Warren Buffett pointed out in his 2014 letter to shareholders that 'volatility is far from synonymous with risk.' Having said that, beta can still be rather useful. The first thing to understand about beta is that the beta of the overall market is one. A stock with a beta greater than one is more sensitive to broader market movements than a stock with a beta of less than one.

See our latest analysis for Wilson

What WILS's beta value tells investors

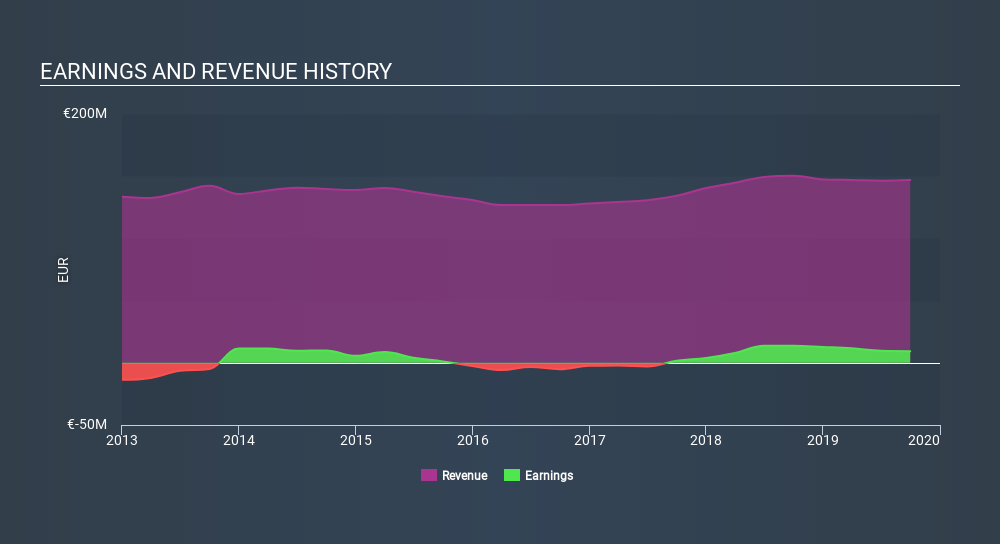

Zooming in on Wilson, we see it has a five year beta of 0.91. This is below 1, so historically its share price has been rather independent from the market. This means that -- if history is a guide -- buying the stock would reduce the impact of overall market volatility in many portfolios (depending on the beta of the portfolio, of course). Many would argue that beta is useful in position sizing, but fundamental metrics such as revenue and earnings are more important overall. You can see Wilson's revenue and earnings in the image below.

Could WILS's size cause it to be more volatile?

Wilson is a rather small company. It has a market capitalisation of kr895m, which means it is probably under the radar of most investors. It is not unusual for very small companies to have a low beta value, especially if only low volumes of shares are traded. Even when they are traded more actively, the share price is often more susceptible to company specific developments than overall market volatility.

What this means for you:

The Wilson doesn't usually show much sensitivity to the broader market. This could be for a variety of reasons. Typically, smaller companies have a low beta if their share price tends to move a lot due to company specific developments. Alternatively, an strong dividend payer might move less than the market because investors are valuing it for its income stream. In order to fully understand whether WILS is a good investment for you, we also need to consider important company-specific fundamentals such as Wilson’s financial health and performance track record. I highly recommend you dive deeper by considering the following:

- Financial Health: Are WILS’s operations financially sustainable? Balance sheets can be hard to analyze, which is why we’ve done it for you. Check out our financial health checks here.

- Past Track Record: Has WILS been consistently performing well irrespective of the ups and downs in the market? Go into more detail in the past performance analysis and take a look at the free visual representations of WILS's historicals for more clarity.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About OB:WILS

Wilson

Wilson ASA operates as a shipping company in Europe.

Solid track record and good value.

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7061.6% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

HE

HedgeY on AST SpaceMobile ·

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Fair Value:US$17036.6% undervalued

31 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

FU

FundamentalFlow on Onto Innovation ·

Onto Innovation: The Advanced Packaging Chokepoint 51.3% undervalued intrinsic discount

Fair Value:US$38026.3% undervalued

20 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7448.8% undervalued

50 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

Recently Updated Narratives

ED

Edward_Sterling on Micron Technology ·

Micron’s AI Crown Sits on a Cycle That Hasn’t Changed

Fair Value:US$1.98k45.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AY

Ayomiposi_X on CWG ·

63% Profit Growth, 6.8× Forward P/E: Inside CWG Plc's FY 2025 Numbers and What They Signal

Fair Value:₦3132.9% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WE

Westimnster on EPAM Systems ·

Expect EPAM's fair value to reach 59.38

Fair Value:US$113.3814.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8589.7% undervalued

124 followersusers have followed this narrative

2 commentsusers have commented on this narrative

36 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9722.1% undervalued

56 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1930.3% undervalued

46 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative