Advertisement

- Canada

- /

- Energy Services

- /

- TSXV:MCR

Will The ROCE Trend At Macro Enterprises (CVE:MCR) Continue?

If we want to find a stock that could multiply over the long term, what are the underlying trends we should look for? Amongst other things, we'll want to see two things; firstly, a growing return on capital employed (ROCE) and secondly, an expansion in the company's amount of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. So on that note, Macro Enterprises (CVE:MCR) looks quite promising in regards to its trends of return on capital.

Return On Capital Employed (ROCE): What is it?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. Analysts use this formula to calculate it for Macro Enterprises:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

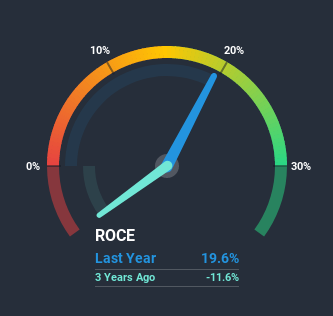

0.20 = CA$29m ÷ (CA$206m - CA$56m) (Based on the trailing twelve months to March 2020).

Therefore, Macro Enterprises has an ROCE of 20%. On its own, that's a standard return, however it's much better than the 14% generated by the Energy Services industry.

View our latest analysis for Macro Enterprises

In the above chart we have a measured Macro Enterprises' prior ROCE against its prior performance, but the future is arguably more important. If you're interested, you can view the analysts predictions in our free report on analyst forecasts for the company.

What Can We Tell From Macro Enterprises' ROCE Trend?

The trends we've noticed at Macro Enterprises are quite reassuring. The numbers show that in the last five years, the returns generated on capital employed have grown considerably to 20%. Basically the business is earning more per dollar of capital invested and in addition to that, 49% more capital is being employed now too. The increasing returns on a growing amount of capital is common amongst multi-baggers and that's why we're impressed.

Our Take On Macro Enterprises' ROCE

A company that is growing its returns on capital and can consistently reinvest in itself is a highly sought after trait, and that's what Macro Enterprises has. Considering the stock has delivered 7.8% to its stockholders over the last five years, it may be fair to think that investors aren't fully aware of the promising trends yet. So exploring more about this stock could uncover a good opportunity, if the valuation and other metrics stack up.

Macro Enterprises does have some risks, we noticed 3 warning signs (and 2 which don't sit too well with us) we think you should know about.

While Macro Enterprises may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

If you’re looking to trade Macro Enterprises, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About TSXV:MCR

Macro Enterprises

Macro Enterprises Inc. provides pipeline and facilities construction and maintenance services to the oil and gas industry in western Canada.

Excellent balance sheet and good value.

Market Insights

Advertisement

Weekly Picks

VA

valuebull on Eva Live ·

Is this the AI replacing marketing professionals?

Fair Value:US$7.4350.9% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

ZA

ZayaanS on Pro Medicus ·

Pro Medicus: The Market Is Confusing a Lumpy Quarter With a Broken Business

Fair Value:AU$196.7838.3% undervalued

27 followersusers have followed this narrative

4 commentsusers have commented on this narrative

18 likesusers have liked this narrative

ST

SteveGruber on Warner Bros. Discovery ·

The Rising Deal Risk That Helped Sink Netflix’s $72 Billion Bid for Warner Bros. Discovery

Fair Value:US$18.1754.1% overvalued

5 followersusers have followed this narrative

1 commentusers have commented on this narrative

3 likesusers have liked this narrative

PD

pdixit1 on Vertiv Holdings Co ·

The Infrastructure AI Cannot Be Built Without

Fair Value:US$408.6438.9% undervalued

32 followersusers have followed this narrative

3 commentsusers have commented on this narrative

13 likesusers have liked this narrative

Recently Updated Narratives

AS

astratov on Santos ·

Santos: Undervalued After Takeover Fallout

Fair Value:AU$8.8917.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

andre_santos on Realty Income ·

Realty Income - A Fundamental and Historical Valuation

Fair Value:US$73.4611.8% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HP

HpN on Microsoft ·

A Structured Counter‑Analysis of "The Leaking Dreadnought"

Fair Value:US$509.8219.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.377.0% undervalued

48 followersusers have followed this narrative

3 commentsusers have commented on this narrative

27 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59631.1% undervalued

1298 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0227.5% undervalued

1101 followersusers have followed this narrative

7 commentsusers have commented on this narrative

33 likesusers have liked this narrative