Advertisement

- India

- /

- Professional Services

- /

- NSEI:RPSGVENT

Will The ROCE Trend At CESC Ventures (NSE:CESCVENT) Continue?

If we want to find a stock that could multiply over the long term, what are the underlying trends we should look for? Ideally, a business will show two trends; firstly a growing return on capital employed (ROCE) and secondly, an increasing amount of capital employed. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. Speaking of which, we noticed some great changes in CESC Ventures' (NSE:CESCVENT) returns on capital, so let's have a look.

Return On Capital Employed (ROCE): What is it?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. The formula for this calculation on CESC Ventures is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.053 = ₹2.5b ÷ (₹62b - ₹15b) (Based on the trailing twelve months to March 2020).

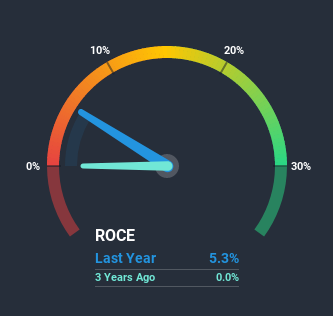

Thus, CESC Ventures has an ROCE of 5.3%. In absolute terms, that's a low return and it also under-performs the IT industry average of 14%.

See our latest analysis for CESC Ventures

Historical performance is a great place to start when researching a stock so above you can see the gauge for CESC Ventures' ROCE against it's prior returns. If you'd like to look at how CESC Ventures has performed in the past in other metrics, you can view this free graph of past earnings, revenue and cash flow.

What Can We Tell From CESC Ventures' ROCE Trend?

We're glad to see that ROCE is heading in the right direction, even if it is still low at the moment. The data shows that returns on capital have increased substantially over the last two years to 5.3%. The company is effectively making more money per dollar of capital used, and it's worth noting that the amount of capital has increased too, by 27%. The increasing returns on a growing amount of capital is common amongst multi-baggers and that's why we're impressed.

In Conclusion...

All in all, it's terrific to see that CESC Ventures is reaping the rewards from prior investments and is growing its capital base. And since the stock has fallen 61% over the last year, there might be an opportunity here. So researching this company further and determining whether or not these trends will continue seems justified.

One more thing to note, we've identified 2 warning signs with CESC Ventures and understanding them should be part of your investment process.

While CESC Ventures isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

If you decide to trade CESC Ventures, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account.Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NSEI:RPSGVENT

RPSG Ventures

Owns, operates, invests, and promotes business in the fields of information technology, business process outsourcing, property, entertainment, fast moving consumer goods, and sports activities in India.

Good value with imperfect balance sheet.

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0775.1% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

JA

Jades on Coca-Cola ·

Coca-Cola’s Enduring Moat in a Health-Conscious World: Steady Compounder Poised for 5-10% Annual Returns Through Emerging Market Dominance

Fair Value:US$66.221.2% overvalued

18 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

ET

Ethan_cpa on Xero ·

Xero: Growth Was Priced In — Execution Is Not

Fair Value:AU$101.5621.3% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

5 likesusers have liked this narrative

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.376.4% undervalued

47 followersusers have followed this narrative

3 commentsusers have commented on this narrative

27 likesusers have liked this narrative

Recently Updated Narratives

JG

JGabriels on SoFi Technologies ·

SOFI-licious Dip

Fair Value:US$18.832.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FI

FIMJ on NVIDIA ·

The NVIDIA Phenomenon

Fair Value:US$313.7541.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AA

Aadi_S on Take-Two Interactive Software ·

Take Two Interactive Software TTWO Valuation Analysis

Fair Value:US$2073.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

DA

davidlsander on Ubisoft Entertainment ·

Is Ubisoft the Market’s Biggest Pricing Error? Why Forensic Value Points to €33 Per Share

Fair Value:€33.888.0% undervalued

65 followersusers have followed this narrative

5 commentsusers have commented on this narrative

28 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59633.1% undervalued

1300 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.376.4% undervalued

47 followersusers have followed this narrative

3 commentsusers have commented on this narrative

27 likesusers have liked this narrative

Trending Discussion

US

User on Caesars Entertainment ·

I can't take seriously any analysis of Caesars Entertainment when there is not present (at least onc...

0

|0