Advertisement

- India

- /

- Basic Materials

- /

- NSEI:BVCL

Will Barak Valley Cements (NSE:BVCL) Multiply In Value Going Forward?

If you're looking for a multi-bagger, there's a few things to keep an eye out for. Ideally, a business will show two trends; firstly a growing return on capital employed (ROCE) and secondly, an increasing amount of capital employed. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. Although, when we looked at Barak Valley Cements (NSE:BVCL), it didn't seem to tick all of these boxes.

Return On Capital Employed (ROCE): What is it?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. The formula for this calculation on Barak Valley Cements is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.045 = ₹86m ÷ (₹2.8b - ₹870m) (Based on the trailing twelve months to June 2020).

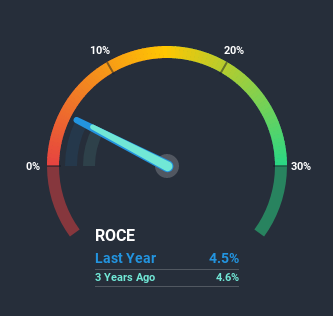

Thus, Barak Valley Cements has an ROCE of 4.5%. In absolute terms, that's a low return and it also under-performs the Basic Materials industry average of 10%.

View our latest analysis for Barak Valley Cements

Historical performance is a great place to start when researching a stock so above you can see the gauge for Barak Valley Cements' ROCE against it's prior returns. If you're interested in investigating Barak Valley Cements' past further, check out this free graph of past earnings, revenue and cash flow.

So How Is Barak Valley Cements' ROCE Trending?

On the surface, the trend of ROCE at Barak Valley Cements doesn't inspire confidence. Over the last five years, returns on capital have decreased to 4.5% from 7.1% five years ago. However it looks like Barak Valley Cements might be reinvesting for long term growth because while capital employed has increased, the company's sales haven't changed much in the last 12 months. It may take some time before the company starts to see any change in earnings from these investments.

On a side note, Barak Valley Cements has done well to pay down its current liabilities to 31% of total assets. So we could link some of this to the decrease in ROCE. What's more, this can reduce some aspects of risk to the business because now the company's suppliers or short-term creditors are funding less of its operations. Since the business is basically funding more of its operations with it's own money, you could argue this has made the business less efficient at generating ROCE.The Bottom Line On Barak Valley Cements' ROCE

In summary, Barak Valley Cements is reinvesting funds back into the business for growth but unfortunately it looks like sales haven't increased much just yet. Since the stock has declined 15% over the last five years, investors may not be too optimistic on this trend improving either. In any case, the stock doesn't have these traits of a multi-bagger discussed above, so if that's what you're looking for, we think you'd have more luck elsewhere.

Barak Valley Cements does have some risks, we noticed 4 warning signs (and 2 which are potentially serious) we think you should know about.

While Barak Valley Cements may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

When trading Barak Valley Cements or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Barak Valley Cements might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NSEI:BVCL

Barak Valley Cements

Manufactures and sells various grades of cement in India.

Flawless balance sheet and slightly overvalued.

Market Insights

Advertisement

Weekly Picks

WE

WealthAP on PayPal Holdings ·

The "Sleeping Giant" Stumbles, Then Wakes Up

Fair Value:US$8227.1% undervalued

28 followersusers have followed this narrative

4 commentsusers have commented on this narrative

23 likesusers have liked this narrative

WO

woodworthfund on Bumble ·

Swiped Left by Wall Street: The BMBL Rebound Trade

Fair Value:US$960.0% undervalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

WE

WealthAP on Duolingo ·

Duolingo (DUOL): Why A 20% Drop Might Be The Entry Point We've Been Waiting For

Fair Value:US$268.6433.4% undervalued

26 followersusers have followed this narrative

4 commentsusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

DE

Deep_Insights on Hims & Hers Health ·

Hims & Hers Health aims for three dimensional revenue expansion

Fair Value:US$173.0279.5% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IN

InvestorNTrader on Endeavour Group ·

Endeavour Group's Future PE Expected to Climb to 15.51%

Fair Value:AU$2.8628.7% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BA

bactrian on Novo Nordisk ·

A Quality Compounder Marked Down on Overblown Fears

Fair Value:US$9540.8% undervalued

97 followersusers have followed this narrative

8 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

AG

Agricola on Excellon Resources ·

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Fair Value:CA$31.898.3% undervalued

69 followersusers have followed this narrative

12 commentsusers have commented on this narrative

21 likesusers have liked this narrative

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25429.4% overvalued

72 followersusers have followed this narrative

1 commentusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0226.0% undervalued

1024 followersusers have followed this narrative

6 commentsusers have commented on this narrative

28 likesusers have liked this narrative