- United States

- /

- Commercial Services

- /

- NYSE:DLX

Why You Should Leave Deluxe Corporation (NYSE:DLX)'s Upcoming Dividend On The Shelf

Regular readers will know that we love our dividends at Simply Wall St, which is why it's exciting to see Deluxe Corporation (NYSE:DLX) is about to trade ex-dividend in the next 4 days. Investors can purchase shares before the 15th of November in order to be eligible for this dividend, which will be paid on the 2nd of December.

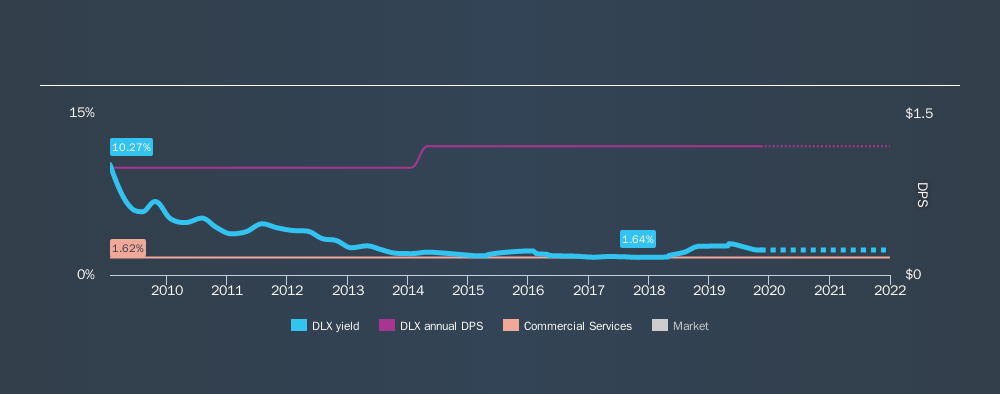

Deluxe's next dividend payment will be US$0.3 per share, and in the last 12 months, the company paid a total of US$1.2 per share. Based on the last year's worth of payments, Deluxe stock has a trailing yield of around 2.3% on the current share price of $51.27. We love seeing companies pay a dividend, but it's also important to be sure that laying the golden eggs isn't going to kill our golden goose! So we need to check whether the dividend payments are covered, and if earnings are growing.

View our latest analysis for Deluxe

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Deluxe reported a loss last year, so it's not great to see that it has continued paying a dividend. With the recent loss, it's important to check if the business generated enough cash to pay its dividend. If Deluxe didn't generate enough cash to pay the dividend, then it must have either paid from cash in the bank or by borrowing money, neither of which is sustainable in the long term. The good news is it paid out just 20% of its free cash flow in the last year.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Companies with falling earnings are riskier for dividend shareholders. If earnings fall far enough, the company could be forced to cut its dividend. Deluxe was unprofitable last year and, unfortunately, the general trend suggests its earnings have been in decline over the last five years, making us wonder if the dividend is sustainable at all.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. Deluxe has delivered an average of 1.8% per year annual increase in its dividend, based on the past ten years of dividend payments.

Remember, you can always get a snapshot of Deluxe's financial health, by checking our visualisation of its financial health, here.

The Bottom Line

Is Deluxe an attractive dividend stock, or better left on the shelf? We're a bit uncomfortable with it paying a dividend while being loss-making. However, we note that the dividend was covered by cash flow. Overall it doesn't look like the most suitable dividend stock for a long-term buy and hold investor.

Wondering what the future holds for Deluxe? See what the three analysts we track are forecasting, with this visualisation of its historical and future estimated earnings and cash flow

We wouldn't recommend just buying the first dividend stock you see, though. Here's a list of interesting dividend stocks with a greater than 2% yield and an upcoming dividend.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NYSE:DLX

Deluxe

Provides technology-enabled solutions to small and medium-sized businesses, and financial institutions in the United States and Canada.

Very undervalued with solid track record and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Automotive Electronics Manufacturer Consistent and Stable

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion