Advertisement

- Canada

- /

- Gas Utilities

- /

- TSX:SPB

What Does Superior Plus Corp.'s (TSE:SPB) Share Price Indicate?

Superior Plus Corp. (TSE:SPB), which is in the gas utilities business, and is based in Canada, saw a significant share price rise of over 20% in the past couple of months on the TSX. With many analysts covering the stock, we may expect any price-sensitive announcements have already been factored into the stock’s share price. But what if there is still an opportunity to buy? Let’s examine Superior Plus’s valuation and outlook in more detail to determine if there’s still a bargain opportunity.

View our latest analysis for Superior Plus

Is Superior Plus still cheap?

The share price seems sensible at the moment according to my price multiple model, where I compare the company's price-to-earnings ratio to the industry average. In this instance, I’ve used the price-to-earnings (PE) ratio given that there is not enough information to reliably forecast the stock’s cash flows. I find that Superior Plus’s ratio of 10.83x is trading slightly below its industry peers’ ratio of 11.08x, which means if you buy Superior Plus today, you’d be paying a reasonable price for it. And if you believe Superior Plus should be trading in this range, then there isn’t much room for the share price to grow beyond the levels of other industry peers over the long-term. Although, there may be an opportunity to buy in the future. This is because Superior Plus’s beta (a measure of share price volatility) is high, meaning its price movements will be exaggerated relative to the rest of the market. If the market is bearish, the company’s shares will likely fall by more than the rest of the market, providing a prime buying opportunity.

What does the future of Superior Plus look like?

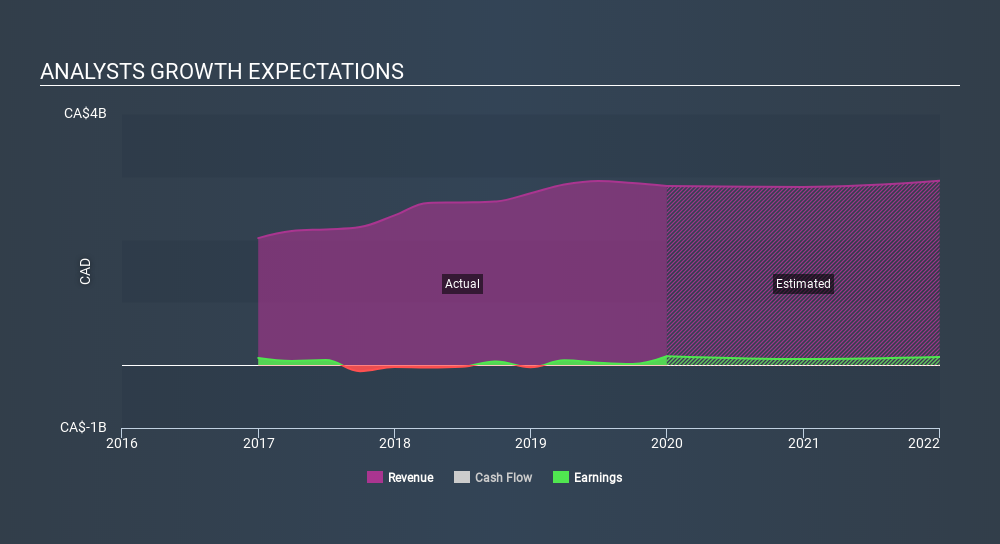

Investors looking for growth in their portfolio may want to consider the prospects of a company before buying its shares. Buying a great company with a robust outlook at a cheap price is always a good investment, so let’s also take a look at the company's future expectations. However, with a negative profit growth of -8.5% expected over the next couple of years, near-term growth certainly doesn’t appear to be a driver for a buy decision for Superior Plus. This certainty tips the risk-return scale towards higher risk.

What this means for you:

Are you a shareholder? Currently, SPB appears to be trading around industry price multiples, but given the uncertainty from negative returns in the future, this could be the right time to reduce the risk in your portfolio. Is your current exposure to the stock beneficial for your total portfolio? And is the opportunity cost of holding a negative-outlook stock too high? Before you make a decision on SPB, take a look at whether its fundamentals have changed.

Are you a potential investor? If you’ve been keeping an eye on SPB for a while, now may not be the most advantageous time to buy, given it is trading around industry price multiples. This means there’s less benefit from mispricing. Furthermore, the negative growth outlook increases the risk of holding the stock. However, there are also other important factors we haven’t considered today, which can help gel your views on SPB should the price fluctuate below the industry PE ratio.

Price is just the tip of the iceberg. Dig deeper into what truly matters – the fundamentals – before you make a decision on Superior Plus. You can find everything you need to know about Superior Plus in the latest infographic research report. If you are no longer interested in Superior Plus, you can use our free platform to see my list of over 50 other stocks with a high growth potential.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About TSX:SPB

Superior Plus

Distributes propane, compressed natural gas, renewable energy, and related products and services to approximately 936,500 customers in the United States and Canada.

Fair value with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Unicycive Therapeutics ·

Looking to be second time lucky with a game-changing new product

Fair Value:US$21.5370.8% undervalued

61 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

HE

HegelBayeBagel on PlaySide Studios ·

PlaySide Studios: Market Is Sleeping on a Potential 10M+ Unit Breakout Year, FY26 Could Be the Rerate of the Decade

Fair Value:AU$0.8460.7% undervalued

12 followersusers have followed this narrative

2 commentsusers have commented on this narrative

7 likesusers have liked this narrative

AN

AnimalDoctorKwon on Inotiv ·

Inotiv NAMs Test Center

Fair Value:US$1.278.3% undervalued

20 followersusers have followed this narrative

2 commentsusers have commented on this narrative

6 likesusers have liked this narrative

TH

TheValueDetector on Cognyte Software ·

This isn’t speculation — this is confirmation.A Schedule 13G was filed, not a 13D, meaning this is passive institutional capital, not acti

Fair Value:US$95.6792.9% undervalued

41 followersusers have followed this narrative

2 commentsusers have commented on this narrative

7 likesusers have liked this narrative

Recently Updated Narratives

TA

Tacenda on Palantir Technologies ·

Valuation Analysis of Palantir Technologies: Growth Assumptions and Market Expectations

Fair Value:US$242.0144.1% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JA

Jades on Coca-Cola ·

Coca-Cola’s Enduring Moat in a Health-Conscious World: Steady Compounder Poised for 5-10% Annual Returns Through Emerging Market Dominance

Fair Value:US$66.220.6% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BR

Bradleywang on Marriott International ·

Asset-Light but Valuation-Heavy: A Fundamental Breakdown of Marriott ($MAR)

Fair Value:US$313.9410.8% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

DA

davidlsander on Ubisoft Entertainment ·

Is Ubisoft the Market’s Biggest Pricing Error? Why Forensic Value Points to €33 Per Share

Fair Value:€33.887.9% undervalued

61 followersusers have followed this narrative

5 commentsusers have commented on this narrative

27 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59633.4% undervalued

1297 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

TA

Talos on Tesla ·

The "Physical AI" Monopoly – A New Industrial Revolution

Fair Value:US$665.3638.1% undervalued

48 followersusers have followed this narrative

19 commentsusers have commented on this narrative

22 likesusers have liked this narrative