Advertisement

- Canada

- /

- Metals and Mining

- /

- CNSX:SPRK

We're Not Very Worried About Maxtech Ventures's (CSE:MVT) Cash Burn Rate

We can readily understand why investors are attracted to unprofitable companies. For example, although Amazon.com made losses for many years after listing, if you had bought and held the shares since 1999, you would have made a fortune. But the harsh reality is that very many loss making companies burn through all their cash and go bankrupt.

So, the natural question for Maxtech Ventures (CSE:MVT) shareholders is whether they should be concerned by its rate of cash burn. For the purpose of this article, we'll define cash burn as the amount of cash the company is spending each year to fund its growth (also called its negative free cash flow). Let's start with an examination of the business's cash, relative to its cash burn.

Check out our latest analysis for Maxtech Ventures

When Might Maxtech Ventures Run Out Of Money?

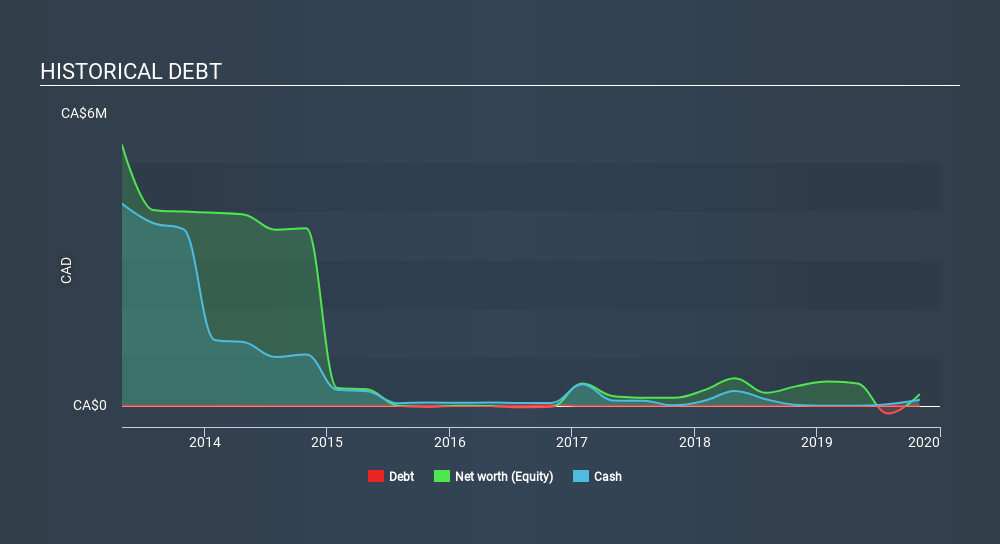

A company's cash runway is the amount of time it would take to burn through its cash reserves at its current cash burn rate. As at October 2019, Maxtech Ventures had cash of CA$121k and no debt. Looking at the last year, the company burnt through CA$124k. That means it had a cash runway of around 12 months as of October 2019. To be frank, this kind of short runway puts us on edge, as it indicates the company must reduce its cash burn significantly, or else raise cash imminently. You can see how its cash balance has changed over time in the image below.

How Is Maxtech Ventures's Cash Burn Changing Over Time?

Because Maxtech Ventures isn't currently generating revenue, we consider it an early-stage business. So while we can't look to sales to understand growth, we can look at how the cash burn is changing to understand how expenditure is trending over time. The good news, from a balance sheet perspective, is that it actually reduced its cash burn by 91% in the last twelve months. That might not be promising when it comes to business development, but it's good for the companies cash preservation. Maxtech Ventures makes us a little nervous due to its lack of substantial operating revenue. So we'd generally prefer stocks from this list of stocks that have analysts forecasting growth.

Can Maxtech Ventures Raise More Cash Easily?

There's no doubt Maxtech Ventures's rapidly reducing cash burn brings comfort, but even if it's only hypothetical, it's always worth asking how easily it could raise more money to fund further growth. Companies can raise capital through either debt or equity. Commonly, a business will sell new shares in itself to raise cash to drive growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

Since it has a market capitalisation of CA$5.9m, Maxtech Ventures's CA$124k in cash burn equates to about 2.1% of its market value. That means it could easily issue a few shares to fund more growth, and might well be in a position to borrow cheaply.

Is Maxtech Ventures's Cash Burn A Worry?

On this analysis of Maxtech Ventures's cash burn, we think its cash burn reduction was reassuring, while its cash runway has us a bit worried. Based on the factors mentioned in this article, we think its cash burn situation warrants some attention from shareholders, but we don't think they should be worried. While it's important to consider hard data like the metrics discussed above, many investors would also be interested to note that Maxtech Ventures insiders have been trading shares in the company. Click here to find out if they have been buying or selling.

If you would prefer to check out another company with better fundamentals, then do not miss this free list of interesting companies, that have HIGH return on equity and low debt or this list of stocks which are all forecast to grow.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About CNSX:SPRK

Spark Energy Minerals

Engages in the acquisition, exploration, and evaluation of mineral properties in Canada.

Excellent balance sheet moderate.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor