Advertisement

- Spain

- /

- Specialty Stores

- /

- BME:ITX

We Think Industria de Diseño Textil (BME:ITX) Can Stay On Top Of Its Debt

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Industria de Diseño Textil, S.A. (BME:ITX) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Industria de Diseño Textil

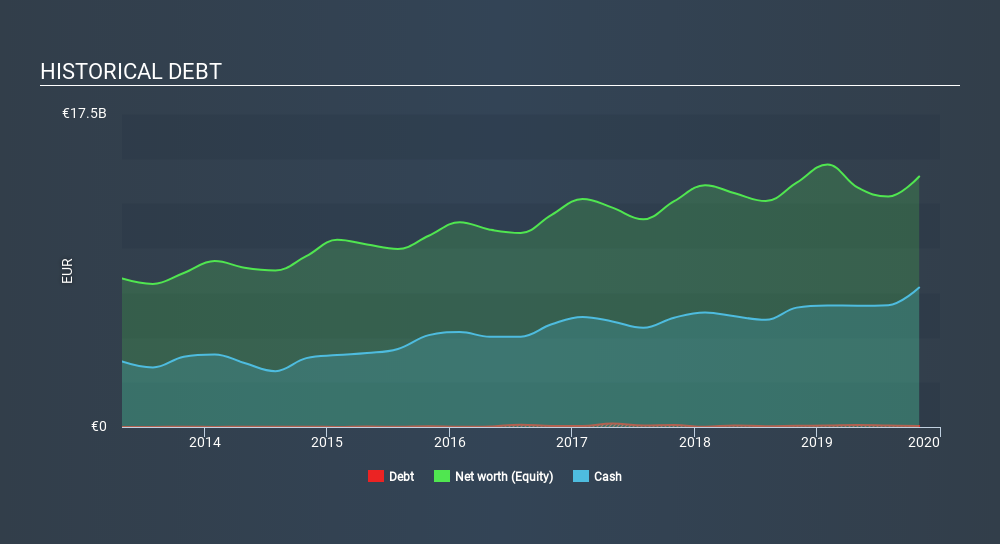

How Much Debt Does Industria de Diseño Textil Carry?

You can click the graphic below for the historical numbers, but it shows that Industria de Diseño Textil had €57.0m of debt in October 2019, down from €68.0m, one year before. But on the other hand it also has €7.80b in cash, leading to a €7.74b net cash position.

How Healthy Is Industria de Diseño Textil's Balance Sheet?

According to the last reported balance sheet, Industria de Diseño Textil had liabilities of €9.26b due within 12 months, and liabilities of €5.98b due beyond 12 months. On the other hand, it had cash of €7.80b and €843.0m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by €6.61b.

Of course, Industria de Diseño Textil has a titanic market capitalization of €87.5b, so these liabilities are probably manageable. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. While it does have liabilities worth noting, Industria de Diseño Textil also has more cash than debt, so we're pretty confident it can manage its debt safely.

Fortunately, Industria de Diseño Textil grew its EBIT by 7.3% in the last year, making that debt load look even more manageable. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Industria de Diseño Textil's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. While Industria de Diseño Textil has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the most recent three years, Industria de Diseño Textil recorded free cash flow worth 65% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Summing up

We could understand if investors are concerned about Industria de Diseño Textil's liabilities, but we can be reassured by the fact it has has net cash of €7.74b. So we don't think Industria de Diseño Textil's use of debt is risky. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should be aware of the 1 warning sign we've spotted with Industria de Diseño Textil .

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About BME:ITX

Industria de Diseño Textil

Engages in the retail and online distribution of clothing, footwear, accessories, and household products in Spain, rest of Europe, the Americas, Asia, and internationally.

Flawless balance sheet with solid track record and pays a dividend.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor