Advertisement

- Italy

- /

- Aerospace & Defense

- /

- BIT:TPS

These Fundamentals Make Technical Publications Service S.p.A. (BIT:TPS) Truly Worth Looking At

Technical Publications Service S.p.A. (BIT:TPS) is a company with exceptional fundamental characteristics. Upon building up an investment case for a stock, we should look at various aspects. In the case of TPS, it is a financially-robust company with an optimistic future outlook, not yet priced into the stock. Below is a brief commentary on these key aspects. For those interested in digging a bit deeper into my commentary, take a look at the report on Technical Publications Service here.

Undervalued with excellent balance sheet

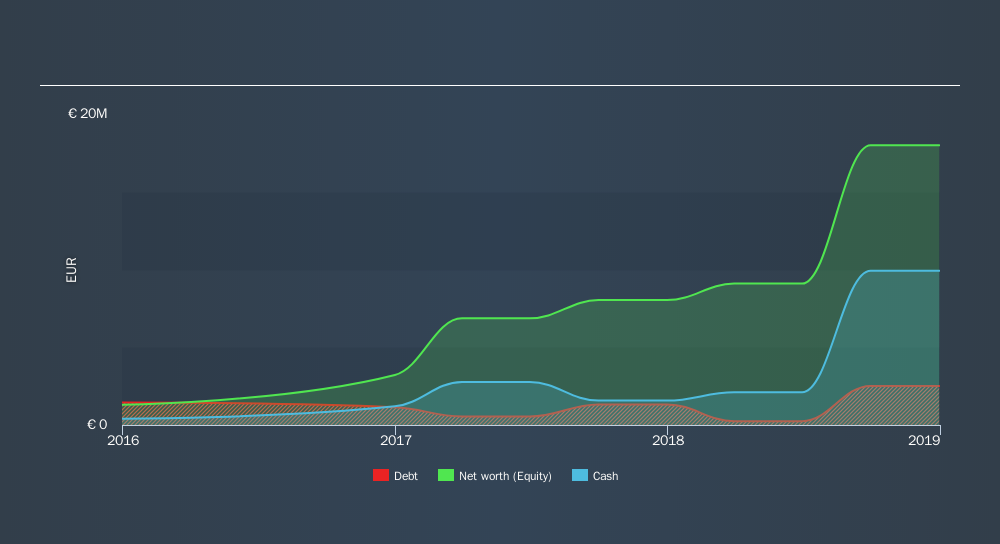

Investors in search for stocks with room to flourish should look no further than TPS, with its expected earnings growth of 20%. The optimistic bottom-line growth is supported by an outstanding revenue growth of 58% over the same time period, which indicates that earnings is driven by top-line activity rather than purely unsustainable cost-reduction initiatives. TPS's shares are now trading at a price below its true value based on its discounted cash flows, indicating a relatively pessimistic market sentiment. Investors have the opportunity to buy into the stock to reap capital gains, if TPS's projected earnings trajectory does follow analyst consensus growth, which determines my intrinsic value of the company. Also, relative to the rest of its peers with similar levels of earnings, TPS's share price is trading below the group's average. This supports the theory that TPS is potentially underpriced.

TPS is financially robust, with ample cash on hand and short-term investments to meet upcoming liabilities. This implies that TPS manages its cash and cost levels well, which is a crucial insight into the health of the company. TPS's has produced operating cash levels of 2.46x total debt over the past year, which implies that TPS's management has put its borrowings into good use by generating enough cash to cover a sufficient portion of borrowings.

Next Steps:

For Technical Publications Service, I've compiled three relevant factors you should further research:

- Historical Performance: What has TPS's returns been like over the past? Go into more detail in the past track record analysis and take a look at the free visual representations of our analysis for more clarity.

- Dividend Income vs Capital Gains: Does TPS return gains to shareholders through reinvesting in itself and growing earnings, or redistribute a decent portion of earnings as dividends? Our historical dividend yield visualization quickly tells you what your can expect from TPS as an investment.

- Other Attractive Alternatives : Are there other well-rounded stocks you could be holding instead of TPS? Explore our interactive list of stocks with large potential to get an idea of what else is out there you may be missing!

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About BIT:TPS

Technical Publications Service

Engages in the provision of engineering and digital services in Italy, EU Countries, and internationally.

Flawless balance sheet and good value.

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7056.5% undervalued

25 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$317.225.0% undervalued

22 followersusers have followed this narrative

7 commentsusers have commented on this narrative

8 likesusers have liked this narrative

NI

niteco on Broadcom ·

A Capital Allocation Favorite with Structural Importance

Fair Value:US$651.0539.8% undervalued

18 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

TO

Tokyo on Okta ·

Good foundation, but now it's all about the next steps

Fair Value:US$15120.6% undervalued

82 followersusers have followed this narrative

7 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Recently Updated Narratives

DA

davidlsander on Ubisoft Entertainment ·

Is Ubisoft the Market’s Biggest Pricing Error? Why Forensic Value Points to €33 Per Share

Fair Value:€33.885.3% undervalued

87 followersusers have followed this narrative

7 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

AntonioS on Retail Food Group ·

Retail Food Group (ASX: RFG) — Deep-Value Thesis

Fair Value:AU$1.250.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BA

Bakullizta on Indofood CBP Sukses Makmur ·

Blindly Bullish on Indofood CBP Sukses Makmur's 5.3% Revenue Growth

Fair Value:Rp9.05k30.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7447.8% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9723.4% undervalued

57 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1932.6% undervalued

48 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

Trending Discussion

SI

Simply Wall St User on Access Holdings ·

It's wonderful. It has greatly helped me take informed decisions.

1

|0