Advertisement

- Australia

- /

- Metals and Mining

- /

- ASX:MSV

These 4 Measures Indicate That Mitchell Services (ASX:MSV) Is Using Debt Reasonably Well

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Mitchell Services Limited (ASX:MSV) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Mitchell Services

What Is Mitchell Services's Debt?

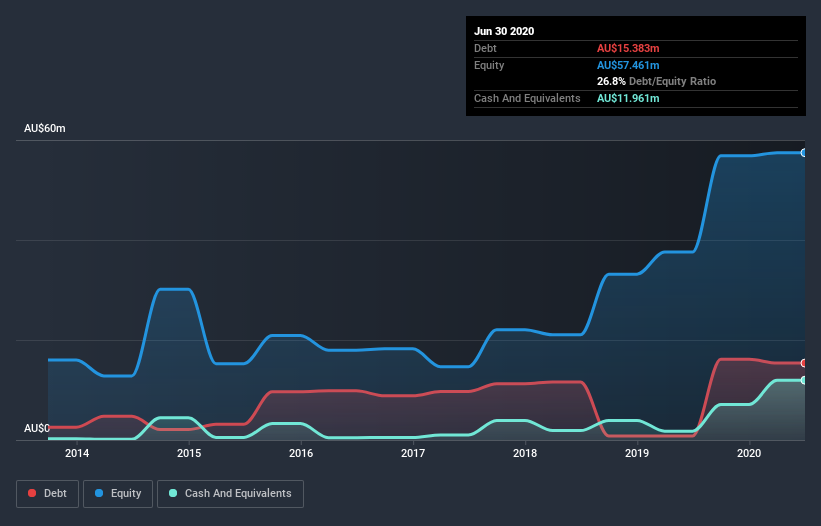

As you can see below, at the end of June 2020, Mitchell Services had AU$15.4m of debt, up from AU$816.3k a year ago. Click the image for more detail. However, because it has a cash reserve of AU$12.0m, its net debt is less, at about AU$3.42m.

How Healthy Is Mitchell Services's Balance Sheet?

The latest balance sheet data shows that Mitchell Services had liabilities of AU$49.5m due within a year, and liabilities of AU$35.1m falling due after that. Offsetting this, it had AU$12.0m in cash and AU$33.0m in receivables that were due within 12 months. So it has liabilities totalling AU$39.6m more than its cash and near-term receivables, combined.

While this might seem like a lot, it is not so bad since Mitchell Services has a market capitalization of AU$109.6m, and so it could probably strengthen its balance sheet by raising capital if it needed to. However, it is still worthwhile taking a close look at its ability to pay off debt.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

While Mitchell Services's low debt to EBITDA ratio of 0.11 suggests only modest use of debt, the fact that EBIT only covered the interest expense by 4.0 times last year does give us pause. So we'd recommend keeping a close eye on the impact financing costs are having on the business. Shareholders should be aware that Mitchell Services's EBIT was down 37% last year. If that decline continues then paying off debt will be harder than selling foie gras at a vegan convention. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Mitchell Services's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it's worth checking how much of that EBIT is backed by free cash flow. Happily for any shareholders, Mitchell Services actually produced more free cash flow than EBIT over the last two years. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Our View

Based on what we've seen Mitchell Services is not finding it easy, given its EBIT growth rate, but the other factors we considered give us cause to be optimistic. There's no doubt that its ability to to convert EBIT to free cash flow is pretty flash. When we consider all the factors mentioned above, we do feel a bit cautious about Mitchell Services's use of debt. While we appreciate debt can enhance returns on equity, we'd suggest that shareholders keep close watch on its debt levels, lest they increase. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For instance, we've identified 5 warning signs for Mitchell Services that you should be aware of.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

If you decide to trade Mitchell Services, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About ASX:MSV

Mitchell Services

Provides exploration, and mine site and geotechnical drilling services to the exploration, mining, and energy industries in Australia.

Flawless balance sheet and good value.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|8.8% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.3% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$384.84|18.1% undervalued

BL

Community Contributor