Advertisement

- India

- /

- Metals and Mining

- /

- NSEI:MANAKSIA

These 4 Measures Indicate That Manaksia (NSE:MANAKSIA) Is Using Debt Safely

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Manaksia Limited (NSE:MANAKSIA) does use debt in its business. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Manaksia

What Is Manaksia's Debt?

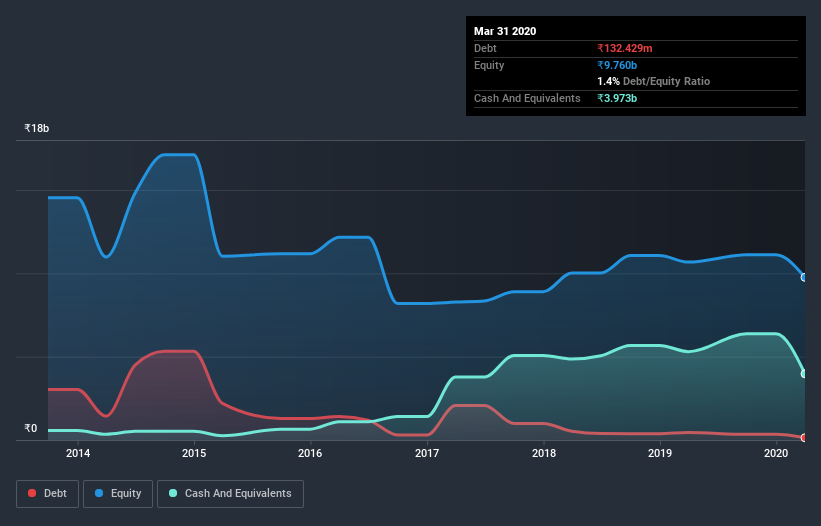

As you can see below, Manaksia had ₹132.4m of debt at March 2020, down from ₹342.9m a year prior. However, it does have ₹3.97b in cash offsetting this, leading to net cash of ₹3.84b.

How Strong Is Manaksia's Balance Sheet?

We can see from the most recent balance sheet that Manaksia had liabilities of ₹1.05b falling due within a year, and liabilities of ₹474.4m due beyond that. Offsetting this, it had ₹3.97b in cash and ₹1.23b in receivables that were due within 12 months. So it actually has ₹3.68b more liquid assets than total liabilities.

This surplus liquidity suggests that Manaksia's balance sheet could take a hit just as well as Homer Simpson's head can take a punch. On this basis we think its balance sheet is strong like a sleek panther or even a proud lion. Succinctly put, Manaksia boasts net cash, so it's fair to say it does not have a heavy debt load!

It is just as well that Manaksia's load is not too heavy, because its EBIT was down 69% over the last year. Falling earnings (if the trend continues) could eventually make even modest debt quite risky. There's no doubt that we learn most about debt from the balance sheet. But it is Manaksia's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. While Manaksia has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Happily for any shareholders, Manaksia actually produced more free cash flow than EBIT over the last three years. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Summing up

While it is always sensible to investigate a company's debt, in this case Manaksia has ₹3.84b in net cash and a strong balance sheet. The cherry on top was that in converted 139% of that EBIT to free cash flow, bringing in -₹399.1m. So is Manaksia's debt a risk? It doesn't seem so to us. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Like risks, for instance. Every company has them, and we've spotted 3 warning signs for Manaksia (of which 1 is concerning!) you should know about.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you’re looking to trade Manaksia, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NSEI:MANAKSIA

Manaksia

Manufactures and sells steel products in India and internationally.

Excellent balance sheet with low risk.

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2540.0% undervalued

77 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

HE

HedgeY on IonQ ·

The Best-Funded Quantum Platform and Still a Stock Priced for Perfection

Fair Value:US$482.3% overvalued

31 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5450.7% undervalued

54 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$825.3% undervalued

27 followersusers have followed this narrative

2 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.917.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DR

DrPotato on TeamViewer ·

TeamViewer Set to Evolve from Stagnation to Enterprise Growth by 2028

Fair Value:€13.3260.9% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

John_Eric on Veeva Systems ·

AI-Powered Veeva Systems Poised for Solid Growth Amid Regulatory Stability

Fair Value:US$32039.8% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75028.1% undervalued

81 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9631.3% undervalued

63 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

NI

niteco on Broadcom ·

A Capital Allocation Favorite with Structural Importance

Fair Value:US$651.0544.6% undervalued

55 followersusers have followed this narrative

0 commentsusers have commented on this narrative

12 likesusers have liked this narrative

Trending Discussion

BU

Buyback_Tiger_ahf5 on Graphic Packaging Holding ·

I was an employee and part of the latest RIF as a result of the leadership change. My take?

0

|0