Advertisement

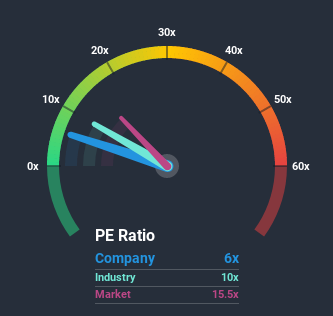

Whitehaven Coal Limited's (ASX:WHC) price-to-earnings (or "P/E") ratio of 6x might make it look like a strong buy right now compared to the market in Australia, where around half of the companies have P/E ratios above 16x and even P/E's above 29x are quite common. However, the P/E might be quite low for a reason and it requires further investigation to determine if it's justified.

Whitehaven Coal hasn't been tracking well recently as its declining earnings compare poorly to other companies, which have seen some growth on average. It seems that many are expecting the dour earnings performance to persist, which has repressed the P/E. If you still like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

Check out our latest analysis for Whitehaven Coal

Does Whitehaven Coal Have A Relatively High Or Low P/E For Its Industry?

It's plausible that Whitehaven Coal's particularly low P/E ratio could be a result of tendencies within its own industry. The image below shows that the Oil and Gas industry as a whole also has a P/E ratio lower than the market. So it appears the company's ratio could be influenced somewhat by these industry numbers currently. In the context of the Oil and Gas industry's current setting, most of its constituents' P/E's would be expected to be toned down. Whilst this can be a heavy component, industry factors are normally secondary to company financials and earnings.

Does Growth Match The Low P/E?

There's an inherent assumption that a company should far underperform the market for P/E ratios like Whitehaven Coal's to be considered reasonable.

Retrospectively, the last year delivered a frustrating 56% decrease to the company's bottom line. Still, the latest three year period has seen an excellent 49% overall rise in EPS, in spite of its unsatisfying short-term performance. Accordingly, while they would have preferred to keep the run going, shareholders would probably welcome the medium-term rates of earnings growth.

Looking ahead now, EPS is anticipated to slump, contracting by 3.5% each year during the coming three years according to the analysts following the company. With the market predicted to deliver 12% growth per annum, that's a disappointing outcome.

With this information, we are not surprised that Whitehaven Coal is trading at a P/E lower than the market. Nonetheless, there's no guarantee the P/E has reached a floor yet with earnings going in reverse. There's potential for the P/E to fall to even lower levels if the company doesn't improve its profitability.

The Key Takeaway

It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As we suspected, our examination of Whitehaven Coal's analyst forecasts revealed that its outlook for shrinking earnings is contributing to its low P/E. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. It's hard to see the share price rising strongly in the near future under these circumstances.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 4 warning signs with Whitehaven Coal, and understanding these should be part of your investment process.

If P/E ratios interest you, you may wish to see this free collection of other companies that have grown earnings strongly and trade on P/E's below 20x.

When trading Whitehaven Coal or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Whitehaven Coal might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About ASX:WHC

Whitehaven Coal

Develops and operates coal mines in New South Wales and Queensland.

Mediocre balance sheet low.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.5% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|18.7% undervalued

TI

Community Contributor