Advertisement

- United States

- /

- Trade Distributors

- /

- NYSE:GWW

There's A Lot To Like About W.W. Grainger, Inc.'s (NYSE:GWW) Upcoming US$1.44 Dividend

It looks like W.W. Grainger, Inc. (NYSE:GWW) is about to go ex-dividend in the next 2 days. Investors can purchase shares before the 8th of May in order to be eligible for this dividend, which will be paid on the 1st of June.

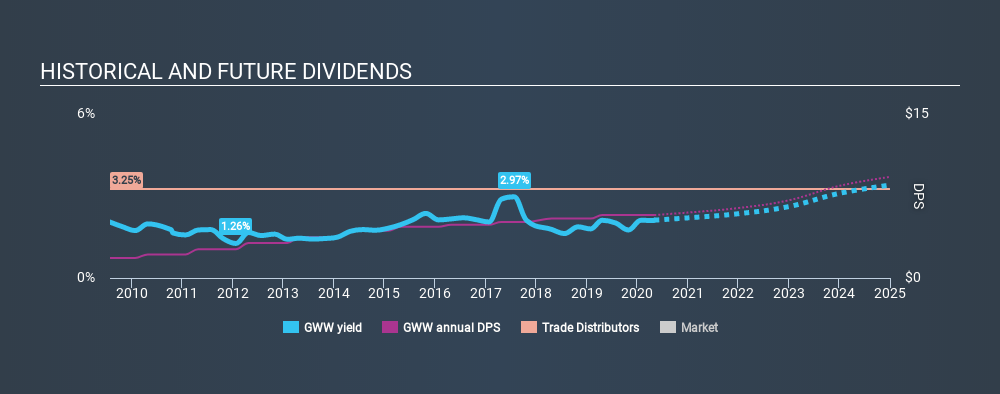

W.W. Grainger's upcoming dividend is US$1.44 a share, following on from the last 12 months, when the company distributed a total of US$5.76 per share to shareholders. Based on the last year's worth of payments, W.W. Grainger stock has a trailing yield of around 2.1% on the current share price of $272.12. Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. That's why we should always check whether the dividend payments appear sustainable, and if the company is growing.

See our latest analysis for W.W. Grainger

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Fortunately W.W. Grainger's payout ratio is modest, at just 41% of profit. That said, even highly profitable companies sometimes might not generate enough cash to pay the dividend, which is why we should always check if the dividend is covered by cash flow. Thankfully its dividend payments took up just 33% of the free cash flow it generated, which is a comfortable payout ratio.

It's positive to see that W.W. Grainger's dividend is covered by both profits and cash flow, since this is generally a sign that the dividend is sustainable, and a lower payout ratio usually suggests a greater margin of safety before the dividend gets cut.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Companies with consistently growing earnings per share generally make the best dividend stocks, as they usually find it easier to grow dividends per share. If business enters a downturn and the dividend is cut, the company could see its value fall precipitously. With that in mind, we're encouraged by the steady growth at W.W. Grainger, with earnings per share up 4.1% on average over the last five years. Recent earnings growth has been limited. However, companies that see their growth slow can often choose to pay out a greater percentage of earnings to shareholders, which could see the dividend continue to rise.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. W.W. Grainger has delivered 12% dividend growth per year on average over the past ten years. We're glad to see dividends rising alongside earnings over a number of years, which may be a sign the company intends to share the growth with shareholders.

Final Takeaway

Is W.W. Grainger worth buying for its dividend? Earnings per share growth has been growing somewhat, and W.W. Grainger is paying out less than half its earnings and cash flow as dividends. This is interesting for a few reasons, as it suggests management may be reinvesting heavily in the business, but it also provides room to increase the dividend in time. We would prefer to see earnings growing faster, but the best dividend stocks over the long term typically combine significant earnings per share growth with a low payout ratio, and W.W. Grainger is halfway there. W.W. Grainger looks solid on this analysis overall, and we'd definitely consider investigating it more closely.

On that note, you'll want to research what risks W.W. Grainger is facing. Our analysis shows 2 warning signs for W.W. Grainger and you should be aware of these before buying any shares.

We wouldn't recommend just buying the first dividend stock you see, though. Here's a list of interesting dividend stocks with a greater than 2% yield and an upcoming dividend.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NYSE:GWW

W.W. Grainger

Distributes maintenance, repair, and operating products and services primarily in North America, Japan, and the United Kingdom.

Solid track record with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor