Advertisement

- United States

- /

- Food and Staples Retail

- /

- NYSE:SYY

Sysco Corporation Earnings Missed Analyst Estimates: Here's What Analysts Are Forecasting Now

Sysco Corporation (NYSE:SYY) last week reported its latest quarterly results, which makes it a good time for investors to dive in and see if the business is performing in line with expectations. It looks like the results were a bit of a negative overall. While revenues of US$15b were in line with analyst predictions, earnings were less than expected, missing estimates by 9.0% to hit US$0.87 per share. Analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. So we collected the latest post-earnings consensus estimates to see what could be in store for next year.

View our latest analysis for Sysco

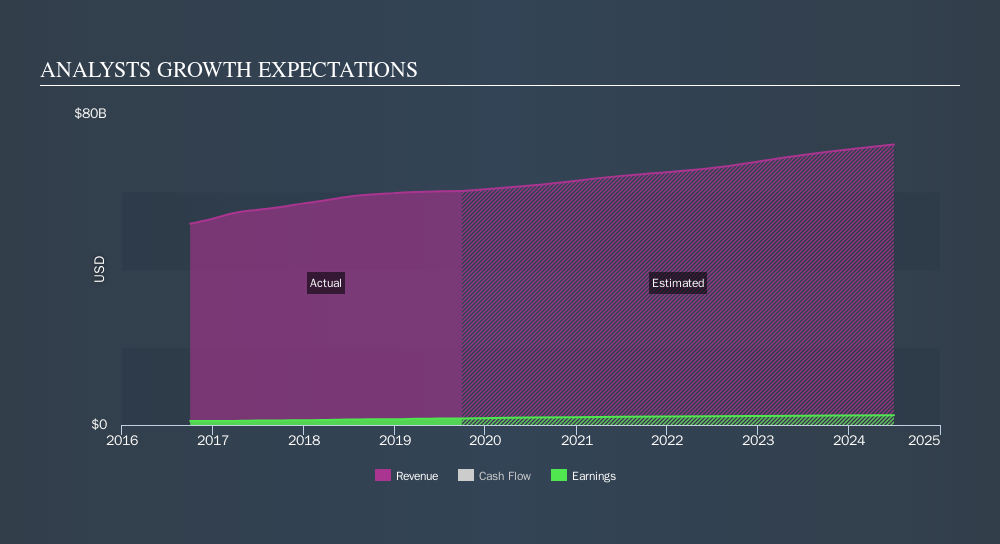

Following the latest results, Sysco's ten analysts are now forecasting revenues of US$62b in 2020. This would be an okay 2.3% improvement in sales compared to the last 12 months. Earnings per share are expected to climb 11% to US$3.66. Yet prior to the latest earnings, analysts had been forecasting revenues of US$62b and earnings per share (EPS) of US$3.76 in 2020. Analysts seem to have become a little more negative on the business after the latest results, given the small dip in their earnings per share forecasts for next year.

Despite cutting their earnings forecasts, analysts have lifted their price target 5.6% to US$81.08, suggesting that these impacts are not expected to weigh on the stock's value in the long term. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. Currently, the most bullish analyst values Sysco at US$94.00 per share, while the most bearish prices it at US$61.00. Analysts definitely have varying views on the business, but the spread of estimates is not wide enough in our view to suggest that extreme outcomes could await Sysco shareholders.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how analyst forecasts compare, both to the Sysco's past performance and to peers in the same market. It's pretty clear that analysts expect Sysco's revenue growth will slow down substantially, with revenues next year expected to grow 2.3%, compared to a historical growth rate of 5.6% over the past five years. Compare this against other companies (with analyst forecasts) in the market, which are in aggregate expected to see revenue growth of 3.8% next year. So it's pretty clear that, while revenue growth is expected to slow down, analysts also expect the wider market to grow faster than Sysco.

The Bottom Line

The most important thing to take away is that analysts downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. On the plus side, there were no major changes to revenue estimates; although analyst forecasts do imply revenues expected to perform worse than the wider market. There was also a nice increase in the price target, with analysts feeling that the intrinsic value of the business is improving.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have estimates - from multiple Sysco analysts - going out to 2024, and you can see them free on our platform here.

You can also view our analysis of Sysco's balance sheet, and whether we think Sysco is carrying too much debt, for free on our platform here.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NYSE:SYY

Sysco

Through its subsidiaries, engages in the marketing and distribution of various food and related products to the foodservice or food-away-from-home industry in the United States, Canada, the United Kingdom, France, and internationally.

Established dividend payer and good value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Nevgold ·

The U.S. Government Is Desperate for This Metal. This Tiny Miner Has It -- Its Closest Peer Is Already Worth Double.

Fair Value:US$2.1946.6% undervalued

38 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6513.0% undervalued

62 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

JD

JD009 on Celsius Holdings ·

From $5M to $2B: Why the 2024 Crash Was the Best Buying Opportunity in Consumer Stocks

Fair Value:US$55.4347.7% undervalued

22 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

WA

Wavefarer on Accenture ·

High-quality global services company facing an AI-driven valuation reset.

Fair Value:US$30152.3% undervalued

17 followersusers have followed this narrative

1 commentusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

RO

Robbo on Microsoft ·

Is Microsoft on sale? and Its Case in the AI Race

Fair Value:US$4042.5% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

AnimalDoctorKwon on Ultragenyx Pharmaceutical ·

burns cash despite four approved drugs, trapped by structural inefficiencies and gene-therapy scaling hurdles that thin safety margins.

Fair Value:US$2612.6% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

AnimalDoctorKwon on BridgeBio Pharma ·

Faces a brutal commercial dogfight against Pfizer’s entrenched monopoly and Alnylam’s silencers, compressing its safety margins

Fair Value:US$25225.5% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75027.5% undervalued

96 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5458.4% undervalued

64 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6513.0% undervalued

62 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Trending Discussion

BE

benjamin_lvieq on PayPal Holdings ·

An investment case is not about loving the product. Its about price vs reality.

2

|0

ST

StoxEurope on Koninklijke Ahold Delhaize ·

I ran Ahold Delhaize through a three-model triangulation — DCF, dividend discount, and residual inco...

1

|0