Advertisement

- Saudi Arabia

- /

- Oil and Gas

- /

- SASE:2222

Some Saudi Arabian Oil Company (TADAWUL:2222) Analysts Just Made A Major Cut To Next Year's Estimates

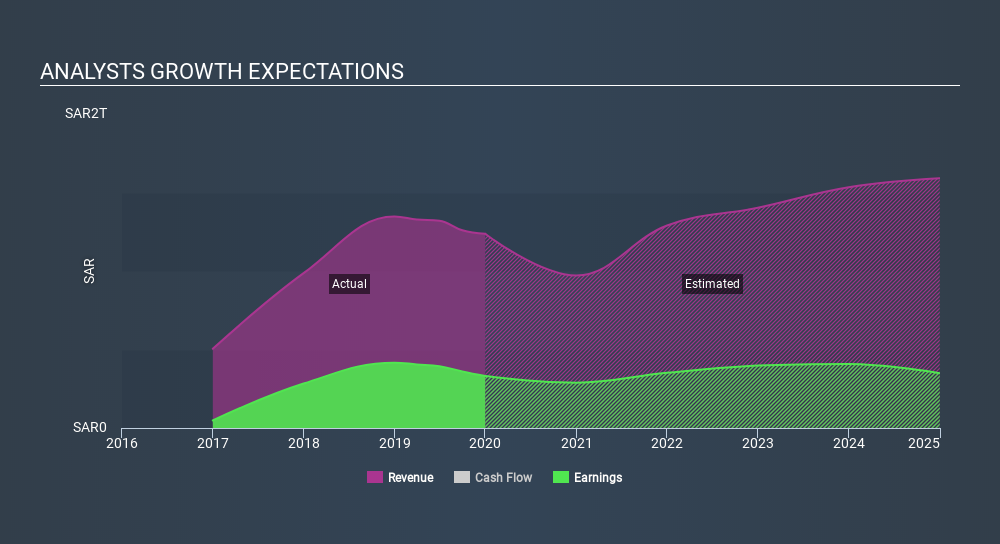

Market forces rained on the parade of Saudi Arabian Oil Company (TADAWUL:2222) shareholders today, when the analysts downgraded their forecasts for this year. Both revenue and earnings per share (EPS) estimates were cut sharply as analysts factored in the latest outlook for the business, concluding that they were too optimistic previously.

Following the latest downgrade, the current consensus, from the 14 analysts covering Saudi Arabian Oil, is for revenues of ر.س971b in 2020, which would reflect a disturbing 21% reduction in Saudi Arabian Oil's sales over the past 12 months. Statutory earnings per share are anticipated to sink 15% to ر.س1.41 in the same period. Prior to this update, the analysts had been forecasting revenues of ر.س1.3t and earnings per share (EPS) of ر.س1.84 in 2020. Indeed, we can see that the analysts are a lot more bearish about Saudi Arabian Oil's prospects, administering a pretty serious reduction to revenue estimates and slashing their EPS estimates to boot.

Check out our latest analysis for Saudi Arabian Oil

The consensus price target fell 6.0% to ر.س30.89, with the weaker earnings outlook clearly leading analyst valuation estimates. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. There are some variant perceptions on Saudi Arabian Oil, with the most bullish analyst valuing it at ر.س43.00 and the most bearish at ر.س24.00 per share. This is a fairly broad spread of estimates, suggesting that the analysts are forecasting a wide range of possible outcomes for the business.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Saudi Arabian Oil's past performance and to peers in the same industry. We would highlight that sales are expected to reverse, with the forecast 21% revenue decline a notable change from historical growth of 22% over the last three years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 5.8% next year. It's pretty clear that Saudi Arabian Oil's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The biggest issue in the new estimates is that analysts have reduced their earnings per share estimates, suggesting business headwinds lay ahead for Saudi Arabian Oil. Regrettably, they also downgraded their revenue estimates, and the latest forecasts imply the business will grow sales slower than the wider market. Given the scope of the downgrades, it would not be a surprise to see the market become more wary of the business.

Unfortunately, by using these new estimates as a starting point, we've run a discounted cash flow calculation (DCF) on Saudi Arabian Oil that suggests the company could be somewhat overvalued. Find out why, and see how we estimate the valuation for free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About SASE:2222

Saudi Arabian Oil

Operates as an integrated energy and chemical company in the Kingdom of Saudi Arabia and internationally.

Excellent balance sheet with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor