Advertisement

- United Kingdom

- /

- Airlines

- /

- LSE:EZJ

Some easyJet plc (LON:EZJ) Analysts Just Made A Major Cut To Next Year's Estimates

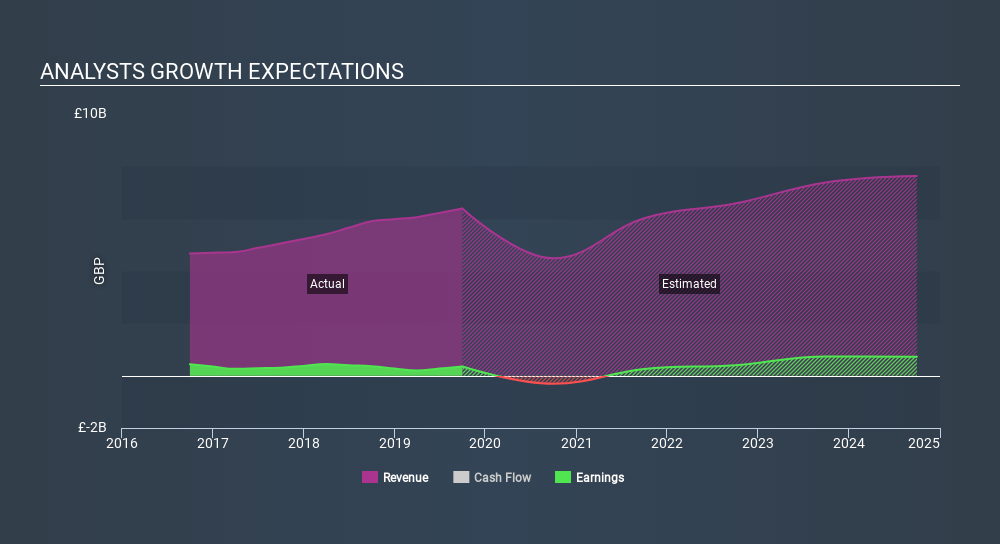

One thing we could say about the analysts on easyJet plc (LON:EZJ) - they aren't optimistic, having just made a major negative revision to their near-term (statutory) forecasts for the organization. Revenue and earnings per share (EPS) forecasts were both revised downwards, with analysts seeing grey clouds on the horizon.

Following the latest downgrade, the 21 analysts covering easyJet provided consensus estimates of UK£4.5b revenue in 2020, which would reflect a sizeable 30% decline on its sales over the past 12 months. Following this this downgrade, earnings are now expected to tip over into loss-making territory, with the analysts forecasting losses of UK£0.76 per share in 2020. Yet prior to the latest estimates, the analysts had been forecasting revenues of UK£5.0b and losses of UK£0.46 per share in 2020. So there's been quite a change-up of views after the recent consensus updates, with the analysts making a serious cut to their revenue forecasts while also expecting losses per share to increase.

View our latest analysis for easyJet

There was no major change to the consensus price target of UK£10.04, signalling that the business is performing roughly in line with expectations, despite lower earnings per share forecasts. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. Currently, the most bullish analyst values easyJet at UK£18.00 per share, while the most bearish prices it at UK£4.50. We would probably assign less value to the forecasts in this situation, because such a wide range of estimates could imply that the future of this business is difficult to value accurately. With this in mind, we wouldn't rely too heavily on the consensus price target, as it is just an average and analysts clearly have some deeply divergent views on the business.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. These estimates imply that sales are expected to slow, with a forecast revenue decline of 30%, a significant reduction from annual growth of 7.3% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 5.5% annually for the foreseeable future. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - easyJet is expected to lag the wider industry.

The Bottom Line

The most important thing to note from this downgrade is that the consensus increased its forecast losses this year, suggesting all may not be well at easyJet. Unfortunately analysts also downgraded their revenue estimates, and industry data suggests that easyJet's revenues are expected to grow slower than the wider market. The lack of change in the price target is puzzling in light of the downgrade but, with a serious decline expected this year, we wouldn't be surprised if investors were a bit wary of easyJet.

A high debt burden combined with a downgrade of this magnitude always gives us some reason for concern, especially if these forecasts are just the first sign of a business downturn. To see more of our financial analysis, you can click through to our free platform to learn more about its balance sheet and specific concerns we've identified.

Another thing to consider is whether management and directors have been buying or selling stock recently. We provide an overview of all open market stock trades for the last twelve months on our platform, here.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About LSE:EZJ

Proven track record with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor