Advertisement

- Canada

- /

- Energy Services

- /

- TSX:AKT.A

Should You Be Pleased About The CEO Pay At AKITA Drilling Ltd.'s (TSE:AKT.A)

Karl Ruud became the CEO of AKITA Drilling Ltd. (TSE:AKT.A) in 2009. This report will, first, examine the CEO compensation levels in comparison to CEO compensation at companies of similar size. Next, we'll consider growth that the business demonstrates. And finally we will reflect on how common stockholders have fared in the last few years, as a secondary measure of performance. This process should give us an idea about how appropriately the CEO is paid.

View our latest analysis for AKITA Drilling

How Does Karl Ruud's Compensation Compare With Similar Sized Companies?

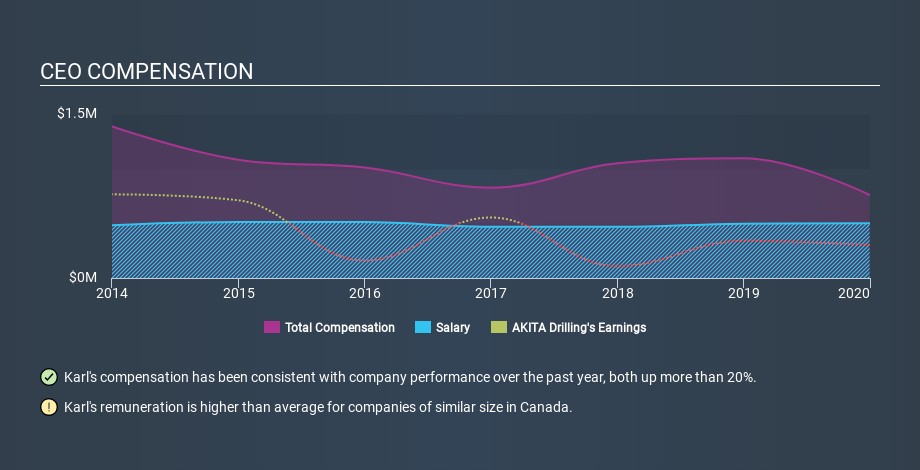

According to our data, AKITA Drilling Ltd. has a market capitalization of CA$19m, and paid its CEO total annual compensation worth CA$759k over the year to December 2019. That's below the compensation, last year. We think total compensation is more important but we note that the CEO salary is lower, at CA$500k. We looked at a group of companies with market capitalizations under CA$281m, and the median CEO total compensation was CA$220k.

Now let's take a look at the pay mix on an industry and company level to gain a better understanding of where AKITA Drilling stands. Speaking on an industry level, we can see that nearly 42% of total compensation represents salary, while the remainder of 58% is other remuneration. According to our research, AKITA Drilling has allocated a higher percentage of pay to salary in comparison to the broader sector.

Thus we can conclude that Karl Ruud receives more in total compensation than the median of a group of companies in the same market, and of similar size to AKITA Drilling Ltd.. However, this doesn't necessarily mean the pay is too high. We can better assess whether the pay is overly generous by looking into the underlying business performance. The graphic below shows how CEO compensation at AKITA Drilling has changed from year to year.

Is AKITA Drilling Ltd. Growing?

AKITA Drilling Ltd. has seen earnings per share (EPS) move positively by an average of 9.4% a year, over the last three years (using a line of best fit). Its revenue is up 49% over last year.

It's great to see that revenue growth is strong. Combined with modest EPS growth, we get a good impression of the company. I wouldn't say this is necessarily top notch growth, but it is certainly promising. Shareholders might be interested in this free visualization of analyst forecasts.

Has AKITA Drilling Ltd. Been A Good Investment?

Since shareholders would have lost about 94% over three years, some AKITA Drilling Ltd. shareholders would surely be feeling negative emotions. It therefore might be upsetting for shareholders if the CEO were paid generously.

In Summary...

We compared the total CEO remuneration paid by AKITA Drilling Ltd., and compared it to remuneration at a group of similar sized companies. As discussed above, we discovered that the company pays more than the median of that group.

The growth in the business has been uninspiring, but the shareholder returns have arguably been worse, over the last three years. Considering this, we have the opinion that the CEO pay is more on the generous side, than the modest side. Taking a breather from CEO compensation, we've spotted 4 warning signs for AKITA Drilling (of which 2 are significant!) you should know about in order to have a holistic understanding of the stock.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies, that have HIGH return on equity and low debt.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About TSX:AKT.A

AKITA Drilling

Operates as an oil and gas drilling contractor in Canada and the United States.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor