Advertisement

- Australia

- /

- Medical Equipment

- /

- ASX:SOM

Shorn Like A Sheep: Analysts Just Shaved Their SomnoMed Limited (ASX:SOM) Forecasts Dramatically

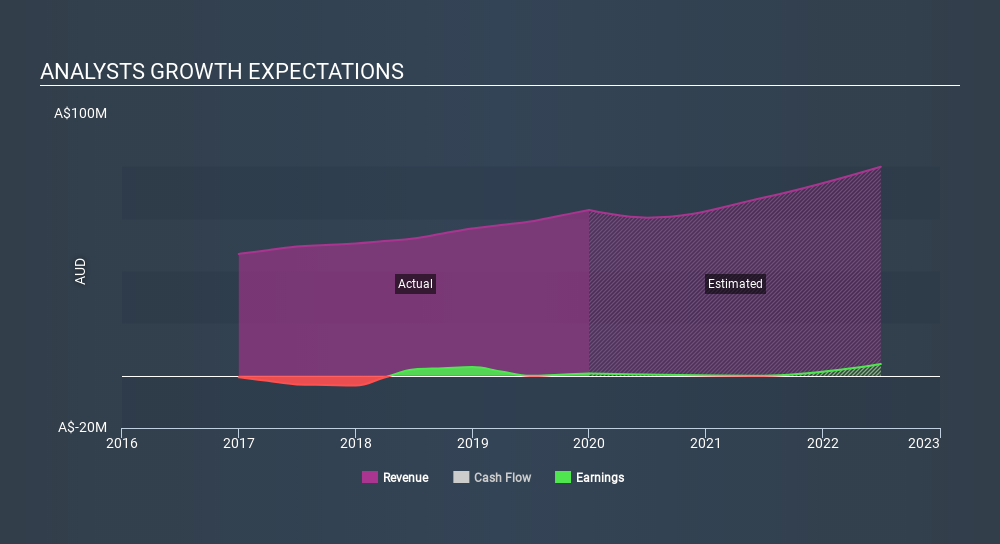

The analysts covering SomnoMed Limited (ASX:SOM) delivered a dose of negativity to shareholders today, by making a substantial revision to their statutory forecasts for this year. Revenue and earnings per share (EPS) forecasts were both revised downwards, with the analysts seeing grey clouds on the horizon.

Following the latest downgrade, the current consensus, from the three analysts covering SomnoMed, is for revenues of AU$60m in 2020, which would reflect a perceptible 4.6% reduction in SomnoMed's sales over the past 12 months. Statutory earnings per share are supposed to reduce 8.8% to AU$0.013 in the same period. Prior to this update, the analysts had been forecasting revenues of AU$68m and earnings per share (EPS) of AU$0.059 in 2020. Indeed, we can see that the analysts are a lot more bearish about SomnoMed's prospects, administering a substantial drop in revenue estimates and slashing their EPS estimates to boot.

See our latest analysis for SomnoMed

It'll come as no surprise then, to learn that the analysts have cut their price target 32% to AU$2.54. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. There are some variant perceptions on SomnoMed, with the most bullish analyst valuing it at AU$3.76 and the most bearish at AU$1.33 per share. Note the wide gap in analyst price targets? This implies to us that there is a fairly broad range of possible scenarios for the underlying business.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. These estimates imply that sales are expected to slow, with a forecast revenue decline of 4.6%, a significant reduction from annual growth of 12% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 15% next year. It's pretty clear that SomnoMed's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The biggest issue in the new estimates is that analysts have reduced their earnings per share estimates, suggesting business headwinds lay ahead for SomnoMed. Unfortunately analysts also downgraded their revenue estimates, and industry data suggests that SomnoMed's revenues are expected to grow slower than the wider market. Given the scope of the downgrades, it would not be a surprise to see the market become more wary of the business.

So things certainly aren't looking great, and you should also know that we've spotted some potential warning signs with SomnoMed, including concerns around earnings quality. For more information, you can click here to discover this and the 3 other risks we've identified.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About ASX:SOM

SomnoMed

SomnoMed Limited, together with its subsidiaries, produce and sells devices for the oral treatment of sleep related disorders in the Asia Pacific region, North America, and Europe.

Flawless balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor