Advertisement

- United States

- /

- Metals and Mining

- /

- NasdaqGS:RDUS

Schnitzer Steel Industries (NASDAQ:SCHN) Has A Somewhat Strained Balance Sheet

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Schnitzer Steel Industries, Inc. (NASDAQ:SCHN) makes use of debt. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Schnitzer Steel Industries

How Much Debt Does Schnitzer Steel Industries Carry?

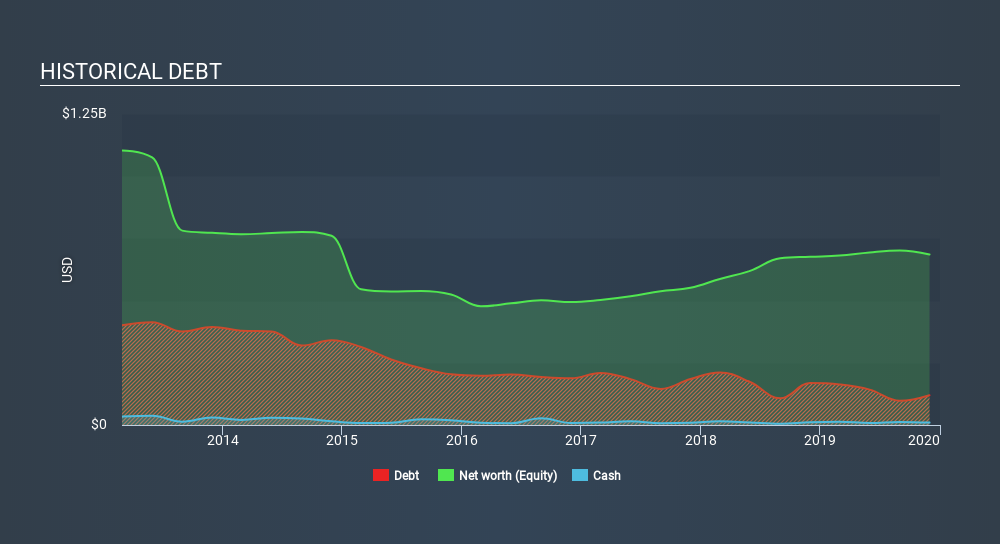

The image below, which you can click on for greater detail, shows that Schnitzer Steel Industries had debt of US$119.8m at the end of November 2019, a reduction from US$168.6m over a year. However, because it has a cash reserve of US$9.62m, its net debt is less, at about US$110.2m.

How Healthy Is Schnitzer Steel Industries's Balance Sheet?

We can see from the most recent balance sheet that Schnitzer Steel Industries had liabilities of US$157.4m falling due within a year, and liabilities of US$316.1m due beyond that. Offsetting these obligations, it had cash of US$9.62m as well as receivables valued at US$120.8m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$343.1m.

This deficit is considerable relative to its market capitalization of US$446.6m, so it does suggest shareholders should keep an eye on Schnitzer Steel Industries's use of debt. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Schnitzer Steel Industries has net debt of just 0.99 times EBITDA, indicating that it is certainly not a reckless borrower. And it boasts interest cover of 7.3 times, which is more than adequate. The modesty of its debt load may become crucial for Schnitzer Steel Industries if management cannot prevent a repeat of the 60% cut to EBIT over the last year. When it comes to paying off debt, falling earnings are no more useful than sugary sodas are for your health. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Schnitzer Steel Industries's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. During the last three years, Schnitzer Steel Industries produced sturdy free cash flow equating to 66% of its EBIT, about what we'd expect. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

Schnitzer Steel Industries's struggle to grow its EBIT had us second guessing its balance sheet strength, but the other data-points we considered were relatively redeeming. For example, its conversion of EBIT to free cash flow is relatively strong. Taking the abovementioned factors together we do think Schnitzer Steel Industries's debt poses some risks to the business. While that debt can boost returns, we think the company has enough leverage now. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. Take risks, for example - Schnitzer Steel Industries has 2 warning signs we think you should be aware of.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NasdaqGS:RDUS

Radius Recycling

Radius Recycling, Inc. recycles ferrous and nonferrous metal, and manufactures finished steel products worldwide.

Fair value low.

Similar Companies

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|9.5% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|7.2% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|56.5% overvalued

UN

Community Contributor