Advertisement

- United Kingdom

- /

- Insurance

- /

- LSE:SBRE

Sabre Insurance Group plc (LON:SBRE) Full-Year Results: Here's What Analysts Are Forecasting For This Year

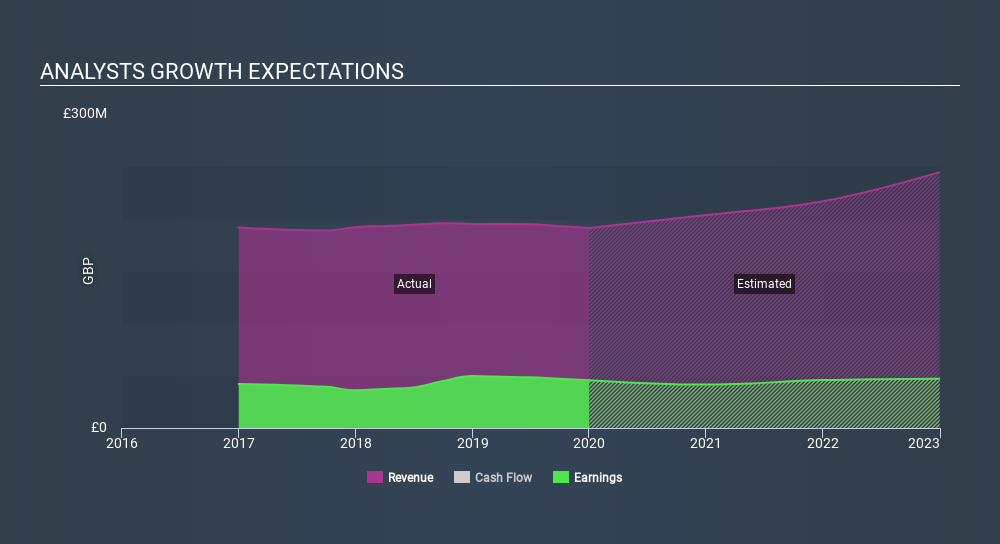

Sabre Insurance Group plc (LON:SBRE) missed earnings with its latest yearly results, disappointing overly-optimistic forecasters. Sabre Insurance Group missed analyst forecasts, with revenues of UK£191m and statutory earnings per share (EPS) of UK£0.18, falling short by 3.9% and 4.3% respectively. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. We thought readers would find it interesting to see the analysts latest (statutory) post-earnings forecasts for next year.

Check out our latest analysis for Sabre Insurance Group

Taking into account the latest results, the current consensus from Sabre Insurance Group's four analysts is for revenues of UK£203.5m in 2020, which would reflect an okay 6.5% increase on its sales over the past 12 months. Statutory earnings per share are forecast to decline 10% to UK£0.17 in the same period. In the lead-up to this report, the analysts had been modelling revenues of UK£208.1m and earnings per share (EPS) of UK£0.18 in 2020. It's pretty clear that pessimism has reared its head after the latest results, leading to a weaker revenue outlook and a minor downgrade to earnings per share estimates.

The analysts made no major changes to their price target of UK£2.77, suggesting the downgrades are not expected to have a long-term impact on Sabre Insurance Group'svaluation. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. The most optimistic Sabre Insurance Group analyst has a price target of UK£3.10 per share, while the most pessimistic values it at UK£2.20. These price targets show that analysts do have some differing views on the business, but the estimates do not vary enough to suggest to us that some are betting on wild success or utter failure.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. It's clear from the latest estimates that Sabre Insurance Group's rate of growth is expected to accelerate meaningfully, with the forecast 6.5% revenue growth noticeably faster than its historical growth of 5.4%p.a. over the past five years. Compare this with other companies in the same industry, which are forecast to see a revenue decline of 17% next year. It seems obvious that as part of the brighter growth outlook, Sabre Insurance Group is expected to grow faster than the wider industry.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for Sabre Insurance Group. Unfortunately, they also downgraded their revenue estimates, and our data indicates sales are expected to perform better than the wider industry. Even so, earnings per share are more important to the intrinsic value of the business. The consensus price target held steady at UK£2.77, with the latest estimates not enough to have an impact on their price targets.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. At Simply Wall St, we have a full range of analyst estimates for Sabre Insurance Group going out to 2022, and you can see them free on our platform here..

Before you take the next step you should know about the 1 warning sign for Sabre Insurance Group that we have uncovered.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About LSE:SBRE

Sabre Insurance Group

Through its subsidiaries, engages in writing of general insurance for motor vehicles in the United Kingdom.

Excellent balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|32.0% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|21.7% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|0.5% overvalued

DA

Community Contributor