- India

- /

- Real Estate

- /

- NSEI:PRESTIGE

Revenue Beat: Prestige Estates Projects Limited Beat Analyst Estimates By 31%

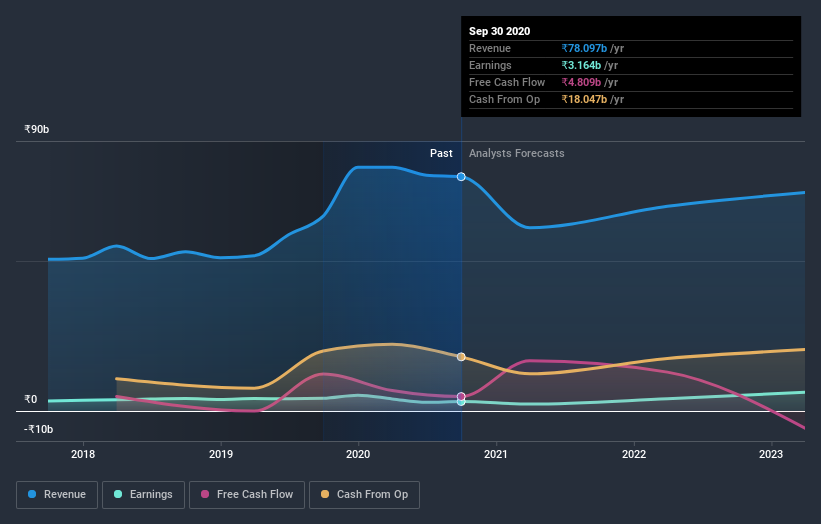

Investors in Prestige Estates Projects Limited (NSE:PRESTIGE) had a good week, as its shares rose 3.1% to close at ₹263 following the release of its second-quarter results. Sales of ₹19b came in a notable 31% ahead of expectations, while statutory earnings of ₹1.49 were in line with what the analysts had been forecasting. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

See our latest analysis for Prestige Estates Projects

After the latest results, the consensus from Prestige Estates Projects' 13 analysts is for revenues of ₹61.1b in 2021, which would reflect a painful 22% decline in sales compared to the last year of performance. Statutory earnings per share are forecast to crater 57% to ₹5.20 in the same period. In the lead-up to this report, the analysts had been modelling revenues of ₹59.6b and earnings per share (EPS) of ₹4.47 in 2021. There's been a pretty noticeable increase in sentiment, with the analysts upgrading revenues and making a decent improvement in earnings per share in particular.

Althoughthe analysts have upgraded their earnings estimates, there was no change to the consensus price target of ₹290, suggesting that the forecast performance does not have a long term impact on the company's valuation. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. There are some variant perceptions on Prestige Estates Projects, with the most bullish analyst valuing it at ₹376 and the most bearish at ₹161 per share. Note the wide gap in analyst price targets? This implies to us that there is a fairly broad range of possible scenarios for the underlying business.

Of course, another way to look at these forecasts is to place them into context against the industry itself. These estimates imply that sales are expected to slow, with a forecast revenue decline of 22%, a significant reduction from annual growth of 19% over the last three years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 14% next year. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - Prestige Estates Projects is expected to lag the wider industry.

The Bottom Line

The most important thing here is that the analysts upgraded their earnings per share estimates, suggesting that there has been a clear increase in optimism towards Prestige Estates Projects following these results. Fortunately, they also upgraded their revenue estimates, although our data indicates sales are expected to perform worse than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

With that in mind, we wouldn't be too quick to come to a conclusion on Prestige Estates Projects. Long-term earnings power is much more important than next year's profits. We have estimates - from multiple Prestige Estates Projects analysts - going out to 2023, and you can see them free on our platform here.

And what about risks? Every company has them, and we've spotted 4 warning signs for Prestige Estates Projects (of which 1 makes us a bit uncomfortable!) you should know about.

If you decide to trade Prestige Estates Projects, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NSEI:PRESTIGE

Prestige Estates Projects

Engages in the development and leasing of real estate properties in India.

High growth potential with adequate balance sheet.

Similar Companies

Market Insights

Community Narratives