Qantas Airways Limited Just Missed Earnings And Its EPS Looked Sad - But Analysts Have Updated Their Models

Qantas Airways Limited (ASX:QAN) last week reported its latest half-year results, which makes it a good time for investors to dive in and see if the business is performing in line with expectations. Revenues were in line with forecasts, at AU$9.5b, although statutory earnings per share came in 17% below what analysts expected, at AU$0.29 per share. Analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. So we gathered the latest post-earnings forecasts to see what analysts' statutory forecasts suggest is in store for next year.

View our latest analysis for Qantas Airways

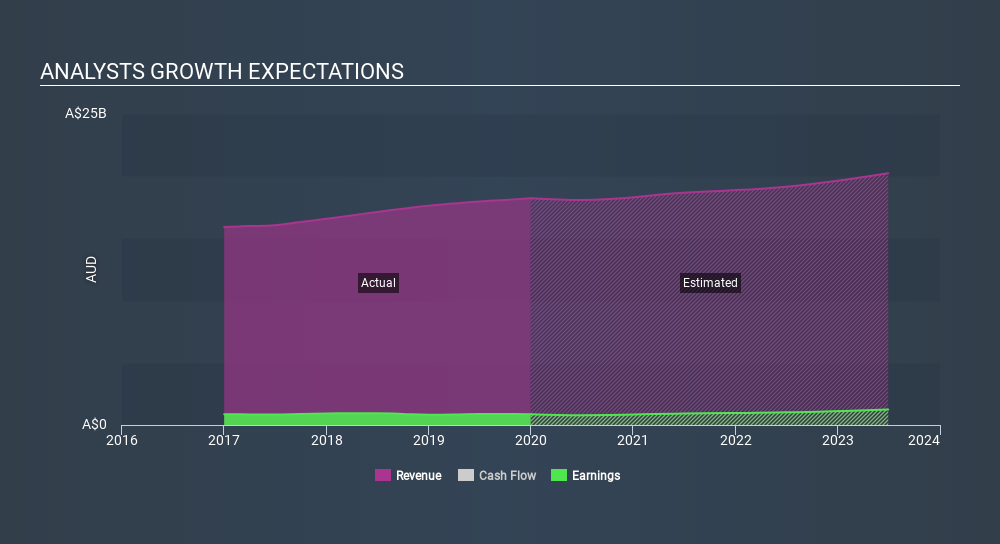

Following last week's earnings report, Qantas Airways's ten analysts are forecasting 2020 revenues to be AU$18.1b, approximately in line with the last 12 months. Statutory earnings per share are expected to dip 8.9% to AU$0.51 in the same period. Before this earnings report, analysts had been forecasting revenues of AU$18.4b and earnings per share (EPS) of AU$0.56 in 2020. Analysts seem to have become a little more negative on the business after the latest results, given the small dip in their earnings per share forecasts for next year.

The consensus price target held steady at AU$7.02, with analysts seemingly voting that their lower forecast earnings are not expected to lead to a lower stock price in the foreseeable future. The consensus price target just an average of individual analyst targets, so - considering that the price target changed, it would be handy to see how wide the range of underlying estimates is. The most optimistic Qantas Airways analyst has a price target of AU$8.00 per share, while the most pessimistic values it at AU$5.00. These price targets show that analysts do have some differing views on the business, but the estimates do not vary enough to suggest to us that some are betting on wild success or utter failure.

Further, we can compare these estimates to past performance, and see how Qantas Airways forecasts compare to the wider market's forecast performance. We would highlight that sales are expected to reverse, with the forecast 0.8% revenue decline a notable change from historical growth of 3.1% over the last five years. Compare this with our data, which suggests that other companies in the same market are, in aggregate, expected to see their revenue grow 6.1% next year. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - analysts also expect Qantas Airways to grow slower than the wider market.

The Bottom Line

The most important thing to take away is that analysts downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. On the plus side, there were no major changes to revenue estimates; although analyst forecasts imply revenues will perform worse than the wider market. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

Still, the long-term prospects of the business are much more relevant than next year's earnings. At Simply Wall St, we have a full range of analyst estimates for Qantas Airways going out to 2023, and you can see them free on our platform here..

You can also see whether Qantas Airways is carrying too much debt, and whether its balance sheet is healthy, for free on our platform here.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About ASX:QAN

Qantas Airways

Provides air transportation services in Australia and internationally.

Good value with acceptable track record.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)