Advertisement

- United States

- /

- Electronic Equipment and Components

- /

- NasdaqGS:PLXS

Plexus Corp. Just Beat Analyst Forecasts, And Analysts Have Been Updating Their Predictions

As you might know, Plexus Corp. (NASDAQ:PLXS) just kicked off its latest quarterly results with some very strong numbers. Plexus beat earnings, with revenues hitting US$852m, ahead of expectations, and statutory earnings per share outperforming analyst reckonings by a solid 10%. This is an important time for investors, as they can track a company's performance in its report, look at what top analysts are forecasting for next year, and see if there has been any change to expectations for the business. We've gathered the most recent statutory forecasts to see whether analysts have changed their earnings models, following these results.

View our latest analysis for Plexus

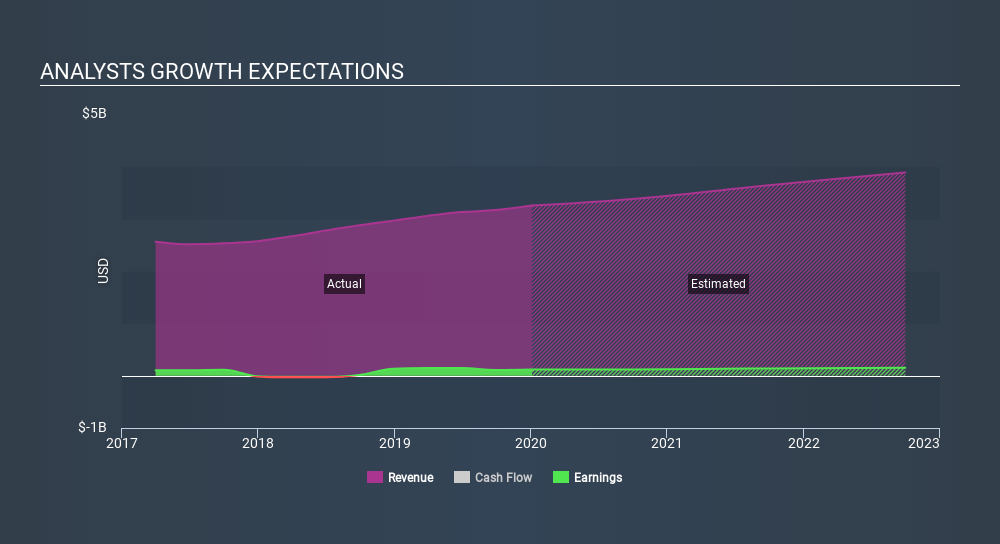

After the latest results, the five analysts covering Plexus are now predicting revenues of US$3.37b in 2020. If met, this would reflect a credible 3.8% improvement in sales compared to the last 12 months. Statutory per share are forecast to be US$3.98, approximately in line with the last 12 months. In the lead-up to this report, analysts had been modelling revenues of US$3.34b and earnings per share (EPS) of US$4.09 in 2020. Analysts seem to have become a little more negative on the business after the latest results, given the minor downgrade to their earnings per share forecasts for next year.

Although analysts have revised their earnings forecasts for next year, they've also lifted the consensus price target 10% to US$84.17, suggesting the revised estimates are not indicative of a weaker long-term future for the business. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. Currently, the most bullish analyst values Plexus at US$93.00 per share, while the most bearish prices it at US$75.00. The narrow spread of estimates could suggest that the business' future is relatively easy to value, or that analysts have a clear view on its prospects.

Another way to assess these estimates is by comparing them to past performance, and seeing whether analysts are more or less bullish relative to other companies in the market. We can infer from the latest estimates that analysts are expecting a continuation of Plexus's historical trends, as next year's forecast 3.8% revenue growth is roughly in line with 4.5% annual revenue growth over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenues grow 5.1% per year. So it's pretty clear that Plexus is expected to grow slower than similar companies in the same market.

The Bottom Line

The most important thing to take away is that analysts downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. Fortunately, analysts also reconfirmed their revenue estimates, suggesting sales are tracking in line with expectations - although our data does suggest that Plexus's revenues are expected to perform worse than the wider market. Analysts also upgraded their price target, suggesting that analysts believe the intrinsic value of the business is likely to improve over time.

With that in mind, we wouldn't be too quick to come to a conclusion on Plexus. Long-term earnings power is much more important than next year's profits. We have forecasts for Plexus going out to 2022, and you can see them free on our platform here.

You can also see whether Plexus is carrying too much debt, and whether its balance sheet is healthy, for free on our platform here.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NasdaqGS:PLXS

Plexus

Provides electronic manufacturing services in the United States, the Asia-Pacific, Europe, the Middle East, and Africa.

Flawless balance sheet with acceptable track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Optimi Health ·

OPTH: A licensed manufacturer already selling MDMA while peers still wait on trials

Fair Value:US$1259.6% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

FU

FundamentalFlow on Vertiv Holdings Co ·

The Short and Long Term Compounder of Liquid Cooling industry.

Fair Value:US$45040.0% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

JO

John_Eric on SPX Technologies ·

I Fell in Love With a Data-Center Cooling Stock. Then I Opened the Filings.

Fair Value:US$2034.6% overvalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

TR

tripledub on GQG Partners ·

The Cheap Genius Problem

Fair Value:AU$2.4541.2% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

Recently Updated Narratives

KL

Klim on PetroTal ·

PetroTal: Betting On a Production Recovery

Fair Value:CA$0.8542.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

david_1211213 on Robo.ai ·

Robo.ai (AIIO): A Long-Term Bullish Technical Setup

Fair Value:US$5.6443.6% undervalued

1 followerusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ES

Ester on Lagenda Properties Berhad ·

Lagenda Properties 录得创纪录销售额与收入,推动盈利能见度提升

Fair Value:RM 2.543.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28022.3% undervalued

293 followersusers have followed this narrative

9 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.9120.5% overvalued

156 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

KI

KiwiInvest on Amazon.com ·

Amazon's high growth, high tech segments propel its profits, while traditional segments plod along

Fair Value:US$475.0941.5% undervalued

176 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

Trending Discussion

IA

ian_oii7z on Woodside Energy Group ·

Hey James! Thank you but I am not sure if I am reading this correctly as your analysis opens with "At A$36.602 per share, Woodside Energy Group (ASX: WDS) appears reasonably valued based on its existing operations and near-term production growth." I would like to say that the last time that WDS was above $36.00 per share was in October 2023, so I am a little confused by your statement w.r.t. current prices etc . Can you please explain?

1

|0

GE

george_b177x on Bloom Energy ·

Brilliant analysis. Great company with proven product and service!

0

|0