Advertisement

- United States

- /

- Semiconductors

- /

- NasdaqCM:PXLW

Pixelworks, Inc. Just Reported And Analysts Have Been Lifting Their Price Targets

It's been a pretty great week for Pixelworks, Inc. (NASDAQ:PXLW) shareholders, with its shares surging 11% to US$4.43 in the week since its latest full-year results. Revenues came in at US$69m, in line with forecasts and the company reported a statutory loss of US$0.24 per share, roughly in line with expectations. Analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. So we gathered the latest post-earnings forecasts to see what analysts' statutory forecasts suggest is in store for next year.

View our latest analysis for Pixelworks

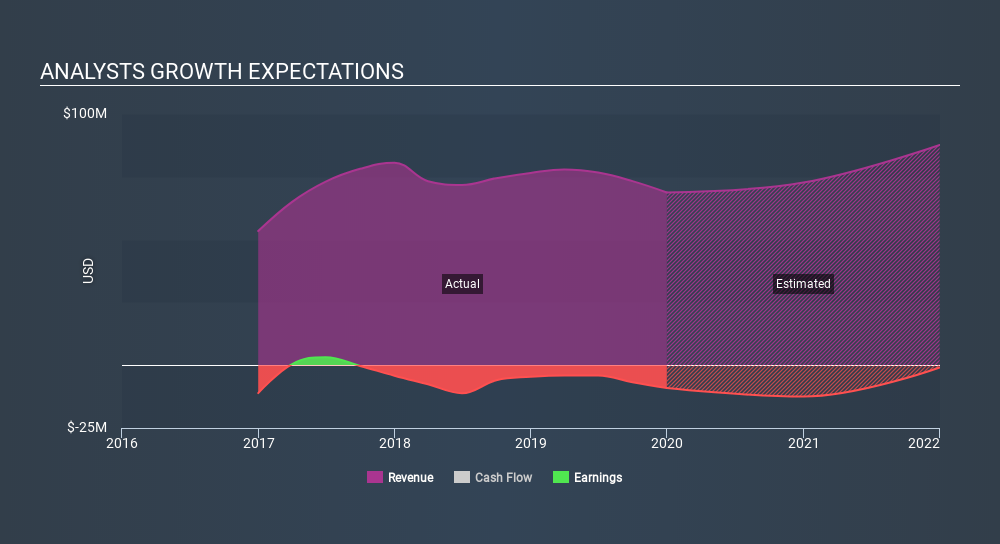

After the latest results, the four analysts covering Pixelworks are now predicting revenues of US$72.7m in 2020. If met, this would reflect a reasonable 5.8% improvement in sales compared to the last 12 months. The statutory loss per share is expected to greatly reduce in the near future, narrowing 33% to US$0.32. Before this latest report, the consensus had been expecting revenues of US$72.7m and US$0.23 per share in losses. Analysts seem to have become more bearish following the latest results. While there were no changes to revenue forecasts, there was a pretty serious reduction to EPS estimates.

Although analysts are now forecasting higher losses, the average analyst price target rose 7.3% to 5.125, which could indicate that these losses are expected to be "one-off", or analysts think they won't have a longer-term impact on the business. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. The most optimistic Pixelworks analyst has a price target of US$6.00 per share, while the most pessimistic values it at US$5.00. The narrow spread of estimates could suggest that the business' future is relatively easy to value, or that analysts have a clear view on its prospects.

It can be useful to take a broader overview by seeing how analyst forecasts compare, both to the Pixelworks's past performance and to peers in the same market. We can infer from the latest estimates that analysts are expecting a continuation of Pixelworks's historical trends, as next year's forecast 5.8% revenue growth is roughly in line with 6.3% annual revenue growth over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenues grow 8.8% per year. So it's pretty clear that Pixelworks is expected to grow slower than similar companies in the same market.

The Bottom Line

The most obvious conclusion is that analysts made no changes to their forecasts for a loss next year. On the plus side, there were no major changes to revenue estimates; although analyst forecasts imply revenues will perform worse than the wider market. Analysts also upgraded their price target, suggesting that analysts believe the intrinsic value of the business is likely to improve over time.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have forecasts for Pixelworks going out to 2021, and you can see them free on our platform here.

We also provide an overview of the Pixelworks Board and CEO remuneration and length of tenure at the company, and whether insiders have been buying the stock, here.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NasdaqCM:PXLW

Pixelworks

Develops and markets semiconductor and software solutions for mobile, home and enterprise, over-the-air, and cinema markets in the United States, Japan, China, and Taiwan.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor